What’s Going On and What to Expect From Here

It doesn’t just seem like there’s a lot going on — there is. Fasten your seat belt. Here we go.

Let’s start by taking a look at the current landscape. So far this year the S&P 500, an index of large U.S. stocks, is down about 14%. How often does this happen? About once a year. Basically, all the time.

But if you watch the news, it sounds much worse. The reason is that the typical investor is getting absolutely crushed. Let’s take a quick look at some of the hottest investments over the last few years and how far they’ve fallen from their recent highs:

- Chinese stocks: -47%

- Tech stocks: -21%

- FAANG stocks: -38%

- Meme stocks (AMC, GameStop, Bed Bath & Beyond): -77%

- Crypto index: -59%

- Bitcoin: -50%

- SPACs: -43%

- Tiger Global (the hedge fund that has garnered the most attention): – 45%

- ARKK Funds (the money manager that has garnered the most attention): -67%

- NFTs: -95%

If you would like a recap on some of these investments, and my warning as to how this would likely play out, you can read my previous newsletter on the topic.

Huge amounts of money had flooded into these speculative investments coming out of the pandemic, and things changed quickly for investors who had placed concentrated bets in these sectors. When rates go up, speculative assets tend to get hit the hardest. This time is no different, but many investors are learning this for the first time — the very hard (and expensive) way.

So, things seem scary out there. How did we get here? It seems we never have to go too far back to take a look at our last crisis, and that’s certainly the case here. So let’s hop in the wayback machine and go way, way, way back to…2020. You may even recall where you were in March 2020 when you heard you were supposed to head home and stay there until further notice. A pandemic was sweeping the world, and we really had no sense of what we were dealing with. Businesses completely shut down, and the president, Congress and the Federal Reserve (Fed) all — in real time — came up with a plan to keep the financial system going.

At the top of the list was dealing with unemployed, and soon to be unemployed, Americans. What followed was a messy, three-part “plan” that involved corporate and Wall Street bailouts, forgivable loans to small (and not-so-small) businesses, and stimulus checks to just about everyone else. Free money, it seemed, was everywhere, and everyone was stuck inside with few ways to spend it.

On top of all the “free” money1, the Fed also dramatically lowered interest rates, making it easier for people to buy houses, cars, boats, equipment, appliances, businesses and just about everything else people regularly borrow money to buy.

As it turns out, vaccines were developed faster than expected, the COVID mortality rate was far better than anticipated and Americans went back outside. But this time, they had more money in their pockets than ever before, and they were ready to do some serious revenge spending. And just to add some juice to the free money, they could now borrow for close to free as well.

With more money chasing the same amount of stuff, prices started to rise. While it was and is clear some of that was due to transitory issues, the Fed stated they believed all the inflation was transitory. “Transitory inflation” just means the causes of inflation were temporary and would soon pass.

In fact, some of the elements are transitory:

- Several million Americans decided to retire early. With expected retirement dates in 2022 or 2023, some simply decided they weren’t going to bother going back to work at all.2

- We typically welcome a few million immigrants into the U.S. each year. Under both President Biden and President Trump, this slowed dramatically (for various reasons, including COVID).

- When stimulus checks began, millions of Americans could make more money staying home than working, and an additional round of stimulus checks made it easier for workers to delay reentry into the market.

- Finally, the supply chain had been turned off during the pandemic, and with workers slow in coming back to work, many workers retiring early, and COVID not under control in many parts of the world, it would take some time for supply systems to get back on track.

While the U.S. economy is making progress in overcoming these four transitory issues, there is now no doubt that part of this inflation comes down to a principle learned in the first hour of the first day of an Economics 101 course: supply and demand. If you have a larger supply of money chasing the same amount of goods, prices will go up. If you have a huge supply of money chasing even less goods, prices will go way up.

And here we are with record home prices, car prices, boat prices and Chipotle burrito bowl prices.

Now, the magic of the Fed is that it can use the same tool — in reverse — to try to contain inflation. And that’s exactly what the Fed is doing by raising interest rates. So far this year, the Fed has raised interest rates twice, first by .25% and then by .50%. The Fed has also indicated it will raise interest rates, in small increments, another 1% or more in total by year end. This makes things more expensive for people to buy. The home that looked affordable with a 2% mortgage doesn’t look as appealing at 5% to 6%. That boat that looked within reach at a 4% interest rate suddenly looks like a money pit at 7%.

The goal of the Fed is to engineer what it loves to refer to as a soft landing. In this ideal outcome, the Fed’s plan results in bringing inflation under control and back to its target of 2% to 3% while still leaving the unemployment rate strong and the economy robust, thus avoiding a recession.

While everyone agrees it’s time to stop spiking the office party punch bowl, the market is not necessarily convinced the Fed can pull this off with such precise elegance, and there is concern the Fed may accidentally tip us into a recession.3

Now, let’s go through a real-world example of how this generally happens. Some of our clients build houses for a living. A year ago, many of them were buying as many lots as they could handle, building as fast as they could, then selling into a super strong housing market. Rinse. Repeat.

Today, many of these developers are still buying lots, but not buying as many. Why? They’re concerned by the time the new houses are complete, the market will have softened due to higher interest rates. They aren’t quite as confident the buyers will still be there in droves with mortgage rates potentially considerably higher. And this has a cascading effect. The homebuilders then need less plumbers, electricians, construction workers, landscape architects and so on. These businesses in turn then order less from their suppliers. This can happen across multiple industries at the same time, and, voila, unemployment goes up, demand drops, businesses make less money, and you have an official recession. A quick look at housing stocks, seen by some as a leading indicator of what’s to come, shows quite a bit of pessimism, with the housing index down about 30%.

The yield curve has inverted as well, which is seen by many as another indicator of a pending recession. Every now and then, the market will pay a lender more interest on a short-term bond than on a long-term bond. For example, if you can loan money to the federal government for two years and get more interest than if you loan it money for 10 years, that tells market observers that something is wrong. There is only one reason why a short-term treasury bond would pay more than a long-term treasury bond, and that would be if investors expected long-term rates to decline, which would only happen if the economy was weak. So, how good of a recession predictor is the inverted yield curve? Well, the majority of the time there’s a recession that follows approximately 18-24 months later. That doesn’t mean much, as the economy is cyclical (meaning it expands and contracts regularly whether the yield curve is inverted or not). Sometimes a recession doesn’t happen at all, sometimes it comes much, much later and, sometimes, the recessions are mild. The bottom line is that the inverted yield curve is not actionable. If you have interest in learning more about the inverted yield curve4, you can check out my previous letter on this, which was done the last time the yield curve inverted. A recession did not follow.

Now, the markets do know, generally, what happens when the Fed pulls money out of the system and raises interest rates. But we now have two unique factors in play that have not presented themselves before.

First, some of the transitory issues are going to take much longer than expected. For example, while in the U.S. we are all going about our business, that’s not the case in other parts of the world, like China. With factories — and sometimes entire cities — in China still going through lockdowns, expect high prices to persist for many of your favorite things, like electronics, toys, machinery and pretty much everything made with plastic.

Second, and this is a doozy, we have now entered into the first period of deglobalization since World War II. Globalization — a word that has somehow become politicized5 — simply means the world is coming together by trading with each other because of advancements with technology. One way to think about it is that globalization is the reason Germany buys its oil from Russia, Europe buys natural gas from Russia, the U.S. buys computer chips from Taiwan and China, and when you call your credit card company, the person who helps you is in a call center in India. Simply put, governments and businesses fill their needs the lowest-cost way possible, going anywhere in the world they need to go to get their products made or their services handled. The Russian invasion of Ukraine may resolve itself, one can hope soon, but the negative impact on globalization is very real and will be sustained. What we are witnessing now, for the first time, is deglobalization. The Germans have pledged to get oil elsewhere, Europe is looking to move away from Russia’s natural gas, the U.S. is now building facilities to make computer chips at home, and so on. We have several clients whose small businesses are building parallel plants in the U.S. so that they can have better control over their products.

In 100% of these instances, the end product or service will cost more. Any time a government or business moves away from the lower-cost global options and moves the service back home, they are by definition paying more, and 100% of these costs will pass through to the consumer, becoming another force for inflation.

In short, the Fed can try to lower demand by raising rates, but they have zero control over supply chain issues and deglobalization, both of which impact the supply and the cost of the supply.

Are you still with me?6

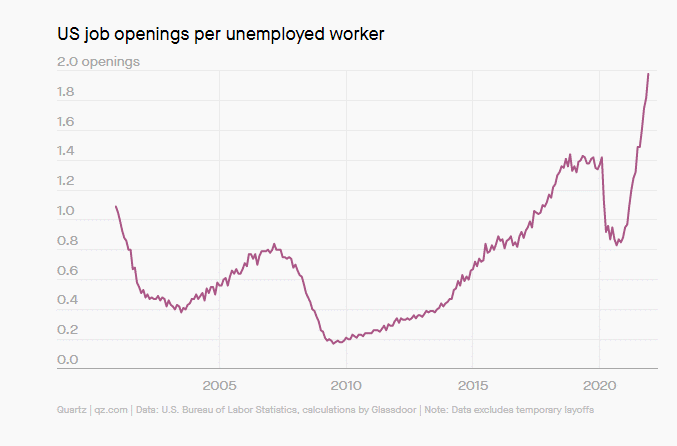

So, to recap, so far we have a normal stock market correction, but more of a blood bath in speculative parts of the market. The markets are concerned the Fed may overdo it with rate hikes and tip us over into a recession. Some indicators, like housing stocks and the inverted yield curve, seem to suggest that may happen. But — and this is big but7 — it’s important to note there is a reason the Fed is raising rates aggressively. The unemployment rate is the lowest it’s ever been. There are now two job openings for every unemployed person (you read that right), there is a shortage of 3.8 million homes needed to meet current demand, people and businesses are still drowning in excess cash, and corporate earnings are very strong. How often has a recession happened with a mix of factors similar to these? Well, never.

What are the various scenarios that can unfold?

- The Fed succeeds with its soft landing. Inflation slows, corporations continue to make money, unemployment stays well under 5% and we all live happily ever after.8 Under this scenario, stocks, real estate and private investments tend to perform best.

- The Fed doesn’t do enough and inflation stays strong for several years. Under this scenario, again, stocks, real estate and private investments are expected to perform best.

- The Fed overdoes it and we fall into a recession. Well, recessions do often lead to bear markets (a drop of 20% or more), but they also tend to be short lived, lasting for less than a year. You, and your portfolio, will survive. Under this scenario, we would expect bonds to come roaring back, as the Fed would have to slow their rate increases or even drop rates.

- Something else happens. The world is dynamic. Literally anything can happen.9 Bad things can happen, like a new virus, a cyberattack, or expansion of war in Europe or elsewhere. Good things can happen, like COVID subsiding in Asia and China coming out of various lockdowns, a peace agreement could be reached with Russia and Ukraine, we could have a technological breakthrough that changes everything, and on and on and on. Under this scenario, the smart investor has short-term needs covered with bonds and similar investments and longer-term needs covered by investments in stocks, real estate and private investments.

The bottom line is there is a lot at play, the economy and markets are dynamic, and any intelligent investor is going to cover their bases with an “anything can happen” bet.

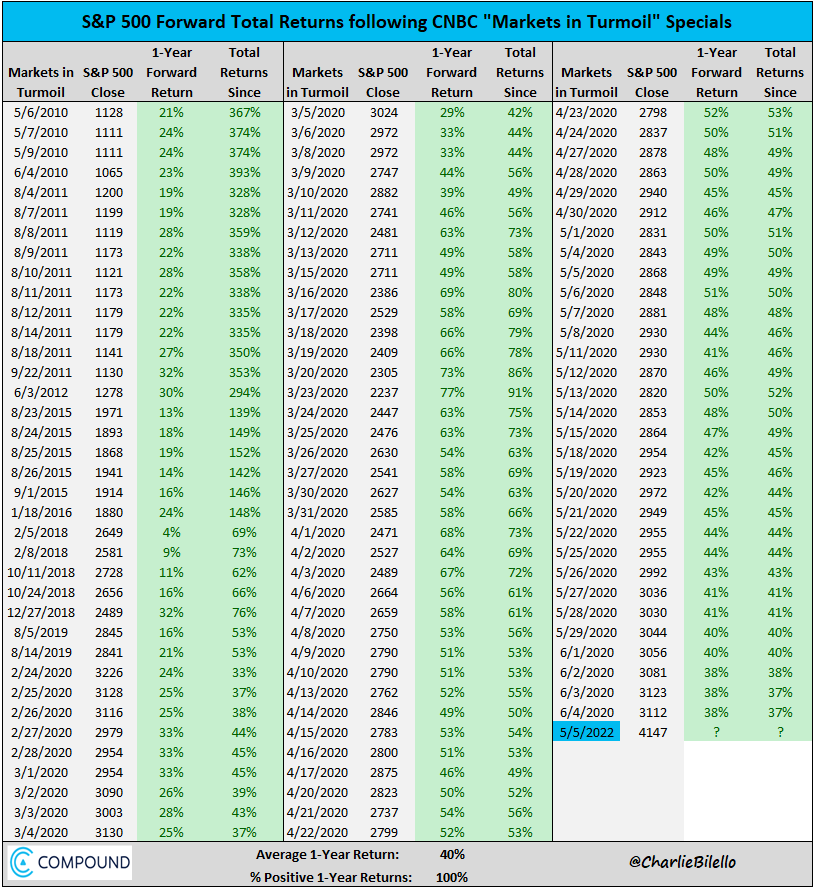

Interestingly, the stock market tends to work itself out quite well in the year following a Fed rate hike, finishing positive 100% of the time over the next 12 months:

What should you do? Stick with your plan, steel yourself for more volatility and know that things may or may not get much worse before they get better, but also know the economy is resilient and always finds a way forward. If we do have a recession, know they tend to be short lived; if the Fed gets it remotely right, there is big upside from here. Regardless, the saying “don’t fight the Fed” exists for a reason. If they do get things wrong, guess what, they get to try again and again and again until they get it right. Low unemployment, supply chain problems and deglobalization suggest the smart investor should maintain a posture to protect against inflation (stocks, real estate and private investments), but the potential for a recession suggests bonds should still be held to cover the shorter term.

Finally, if you were looking for the ultimate contrarian indicator, CNBC ran a special last week titled “Markets in Turmoil” — something they have done now more than 100 times in the last dozen years.10 100% of the time, the stock market finished positive (usually very substantially positive) over the next 12 months.

Footnotes:

- Every economist knows there is no such thing as a free lunch; someone has to pay for it, someday and in some way.

- Hi, Dad! To be fair, my dad had planned to retire from internal medicine at age 88, but being a total slacker he decided age 86 was good enough.

- This is an uncharacteristically long newsletter for me, so feel free to walk the dog, take a nap or grab a drink. I’ll be here when you get back.

- If you click this link, you are a glutton for punishment, as there are few things more boring than the yield curve.

- I am waiting for the word sofa to become politicized somehow.

- God bless you.

- Insert Sir Mix-A-Lot joke here.

- Or until the next crisis, that is.

- Anyone that has been alive over the last five to 10 years is doing their face slap emoji impersonation at least once a week.

- It turns out the markets are in turmoil quite a bit.