Key Takeaways

- Diversification isn’t just “own some bonds with your stocks” — it’s a portfolio construction process designed to manage risk across different market conditions and economic regimes.

- A diversified portfolio blends different asset classes, sectors, regions and market caps so that no single bad decade in one area sinks your entire investment portfolio.

- Stocks, bonds, real estate, international markets, private markets and alternative investments all behave differently in disinflationary booms, deflationary busts, stagflation and inflationary booms.

- Building your asset allocation around your goals, risk tolerance and time horizon comes first; adjusting around current market volatility and interest rate moves comes second.

- Working with a fiduciary advisor can help align your diversification strategy and risk management approach with your long-term financial goals.

I’d like to discuss a topic that seems boring but is actually pretty nuanced and dynamic — diversification.

You’ve probably heard some of the greatest hits: “Diversification is the only free lunch,” “Don’t put all your eggs in one basket,” and “You concentrate to get rich but diversify to stay rich.” These one-liners are catchy, but they don’t explain what’s going on under the hood of an investment portfolio.

Many investors don’t truly understand diversification beyond “don’t put all your money in one or two stocks.” Nor do they understand how each holding plays into a diversified portfolio and their long-term financial goals.

In this piece, we’ll dig into what diversification really is, how different asset classes behave in various economic environments and how thoughtful portfolio diversification for different economic environments can help you manage risk while still pursuing growth potential.

Construction First, Adjusting Next

Some investment management clients believe an advisor starts by predicting the future and investing accordingly. That couldn’t be further from how a disciplined diversification strategy works.

Most advisors, including those at Creative Planning, start by constructing a diversified portfolio based on your financial plan, other income streams, cash flow distributions, risk tolerance and time horizon. Only after that core portfolio construction work is done do we form an opinion on current market conditions and make adjustments around the edges.

We don’t build an investment portfolio around a single prediction about interest rates, inflation or the next recession. Instead, we recognize that different asset classes and different types of investments behave differently as the economy and inflation move through various regimes, and we want your portfolio prepared for multiple possible paths instead of just one.

Diversification 101

In textbooks, diversification usually shows up in the context of modern portfolio theory and the idea of reducing unsystematic risk (the risk specific to a company or sector) by owning many different investments. At a practical level, diversification helps protect your portfolio from a bad short-term or long-term experience.

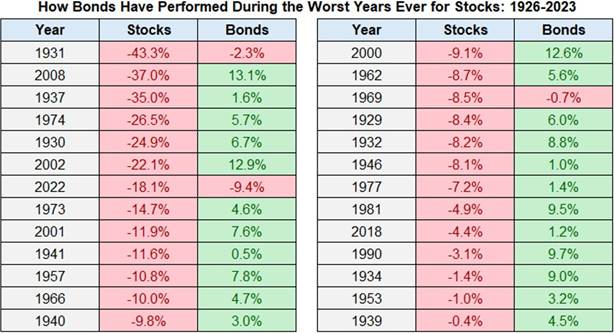

The simplest, most familiar example is the relationship between stocks and bonds. Historically, in most (but not all) periods, when stocks go down, high-quality fixed income has held up relatively well or even risen, softening the blow to a diversified portfolio. Holding bonds can help reduce overall portfolio risk and may provide diversification benefits during periods of equity market downturns.

Source: https://awealthofcommonsense.com/2024/01/the-holy-grail-of-portfolio-management/

That’s Diversification 101: holding different asset classes that don’t all move in the same direction at the same time.

Short-Term Pain vs. Long-Term “Bad Experiences”

What’s less well known is the risk of a long-term bad experience in a single asset class or style. History offers multiple examples of long periods where even the mighty U.S. large cap stock market went essentially nowhere for a decade or more in real (inflation-adjusted) terms.

Bonds can go through their own rough patches too. As investors have seen in recent years, even usually steady, high-quality U.S. bond indexes can suffer extended downturns when interest rates rise sharply and market volatility spikes.

The reality is that every asset class, style and sector — U.S. vs. international, large vs. small, growth vs. value, public vs. private, real estate, alternative investments and more — will go through good and bad periods. There’s no silver bullet you can hold that will always work in every market condition.

That’s why a thoughtful diversification strategy is really about:

- Identifying the possible environments that may occur over your investing lifetime

- Understanding how different asset classes and investments tend to behave in those environments

- Allocating enough to various investments so that the risk of your entire portfolio experiencing a truly awful decade is reduced

If you want a visual of how different asset classes take turns leading and lagging, Creative Planning’s annual returns by asset class “periodic table” is a great illustration of why different asset classes and different types of investments belong in a diversified portfolio.

4 Key Environments to Plan For

One environment that’s more market-driven than economic is a bubble — when an asset or a sector gets so overpriced that it may disappoint over the long run. Think U.S. large cap growth stocks after the tech bubble in 2000 or Japanese equities after 1989. After a huge run-up in valuations, those markets experienced long stretches of weak or flat returns.

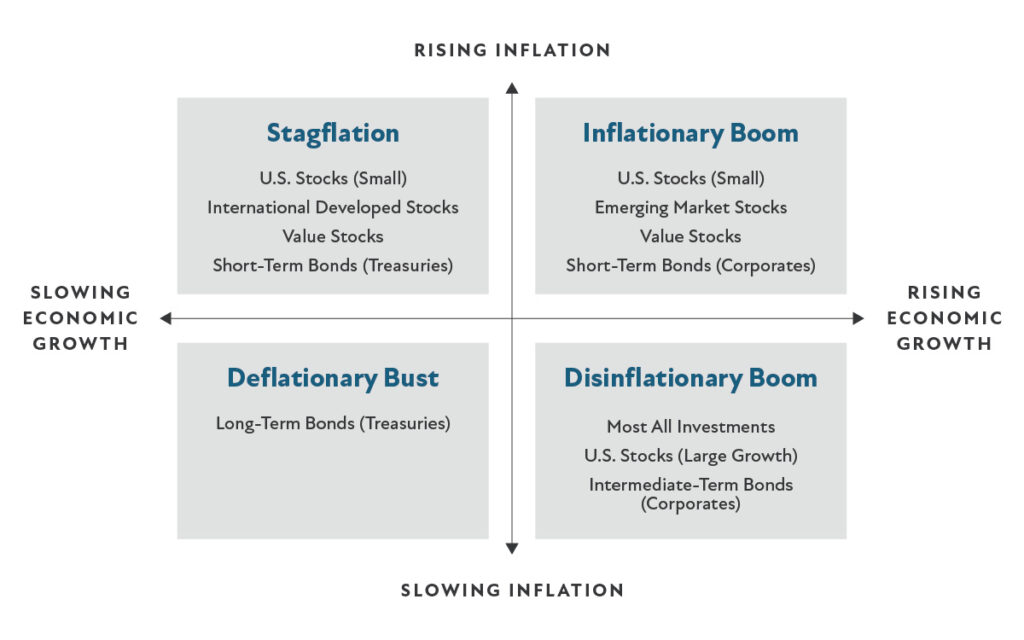

Beyond bubbles, most of the major environments investors live through can be described by what’s happening with inflation and economic growth. A simple framework many portfolio managers use divides the world into four broad quadrants:

- Disinflationary boom – Growth is solid, and inflation is falling or under control.

- Deflationary bust – Both growth and inflation are falling, often in a recession.

- Stagflation – Growth is slowing while inflation is rising.

- Inflationary boom – Growth is strong, and inflation is also rising.

Over time, the economy and markets move between these four environments, and each has very different implications for asset allocation, portfolio risk and which parts of your diversified portfolio are likely to do the heavy lifting.

Asset allocation by economic quadrant

Disinflationary boom: the “easy” environment

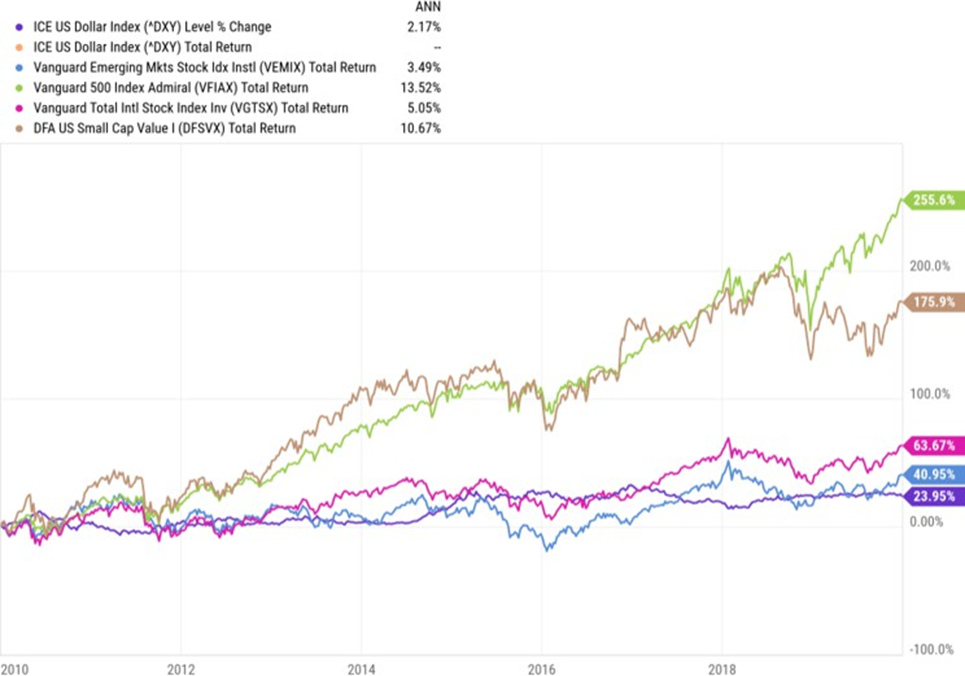

A disinflationary boom is the best of both worlds: the economy is growing, but inflation isn’t a problem. Corporate profits often rise, interest rates are stable or falling, and many kinds of investments can do well.

The decade leading up to 2020 — which was not quite a “boom” but still had solid growth with mostly contained inflation — is a familiar example. During this stretch, U.S. large cap growth stocks led the way while international stocks generally lagged in part because the U.S. dollar strengthened.

In this kind of environment:

- Broad equities, especially large cap growth and quality companies, tend to do well.

- Long-term bonds can benefit if interest rates are drifting lower, though yields may be modest.

- Risk assets across the board often enjoy tailwinds, even if some areas still face headwinds from currency moves or local market risk.

If you build your portfolio only for this environment — heavy in U.S. growth stocks, longer-term bonds and maybe some real estate — it might feel great while it lasts, but that approach can fall short when markets shift. That’s why we emphasize broader diversification across sectors, regions and asset classes in our piece on diversification strategies for various markets.

Disinflationary Boom Performance Chart (2010–2019)

Source: Ycharts. 12/31/2009-12/31/2019

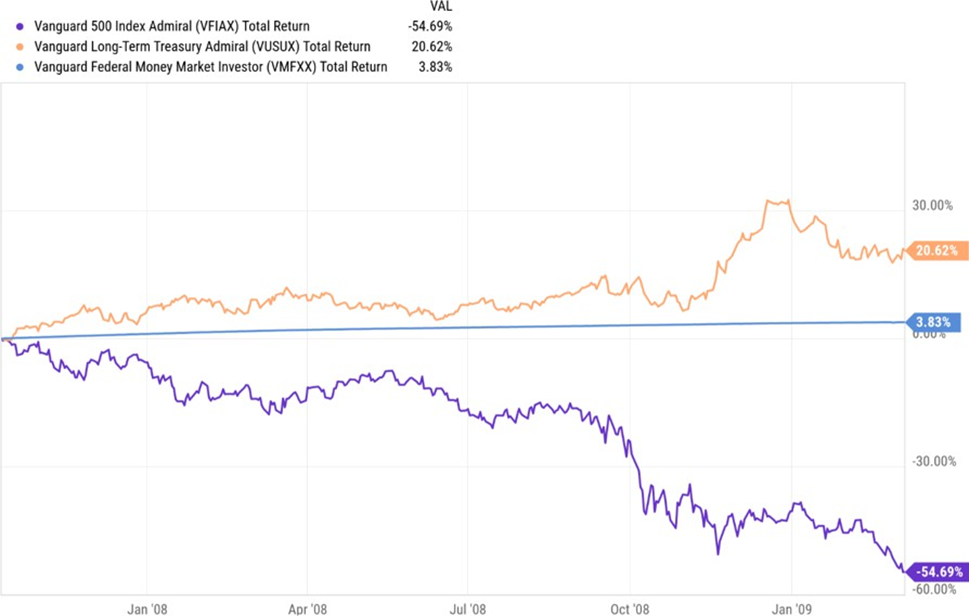

Deflationary bust: when safety shines

A deflationary bust often happens during a deep recession, when the economy contracts enough to also drag inflation down. The global financial crisis of 2007-2009 is the classic modern example.

In this environment:

- Long-term U.S. Treasury bonds and other high-quality fixed income often fare well as investors seek safety and benefit from falling interest rates.

- Many risk assets — such as stocks, high-yield bonds and certain types of real estate — can struggle as earnings expectations are cut and credit stress rises.

- Cash and short-term fixed income help dampen portfolio volatility and provide liquidity.

This is where the most basic form of diversification — owning both stocks and high-quality bonds — really shows its value. Even if your equities are going through a painful decline, your fixed income allocation may be rising or at least holding up, helping manage overall risk and giving you dry powder to rebalance when markets eventually recover. For more on how to think about downturns in context, see Creative Planning’s guidance on bear markets and how you can prepare for the next one.

Deflationary Bust Performance Chart (2007–2009)

Source: Ycharts. 10/10/2007-03/06/2009

Stagflation: the worst of both worlds

Stagflation — slowing growth and rising inflation—is one of the hardest environments. The 1970s are the poster child: U.S. stocks and high-quality bonds both struggled in real terms, inflation eroded purchasing power, and the U.S. dollar often weakened as capital moved to stronger currencies.

In stagflation:

- Traditional “core” stocks and bonds can both be challenged at the same time.

- International stocks can benefit, particularly if capital flows toward regions with stronger currencies or better inflation dynamics.

- Small cap value stocks, especially in sectors tied to hard assets like energy, materials, industrials, real estate and financials, may hold up relatively well because their fundamentals can benefit from rising prices.

- Within fixed income, shorter-term bonds usually fare better than long-term bonds because their prices are less sensitive to rising interest rates.

This is a powerful case for combining style diversification (growth vs. value, large vs. small), geographic diversification (U.S. vs. international vs. emerging markets) and exposure to real asset-oriented sectors in your overall diversification strategy. If you’d like to dig further into why your wealth shouldn’t be concentrated solely in U.S. markets, Creative Planning’s article on why your wealth should be diversified globally walks through the case for global diversification.

Inflationary boom: growth with a catch

An inflationary boom is characterized by strong economic growth and rising inflation. Investors cheer the economic strength but also worry about preserving purchasing power as prices climb.

In this environment:

- Global growth tends to be strong, and the U.S. dollar often weakens as capital flows to faster growing or higher yielding markets abroad.

- Historically, small-cap and value stocks have tended to perform relatively well in such periods, especially in sectors tied to real assets or financials; future results may differ

- International stocks, particularly those in emerging markets, have sometimes outperformed in similar environments as their earnings benefited from stronger local growth and a weaker dollar, though such outcomes are not guaranteed

- Corporate bonds, especially high-yield bonds with shorter maturities have, in some historical periods, delivered higher returns than traditional Treasuries when the economy was strong and perceived default risk was lower; however, future performance remains uncertain

If your strategy is built only around U.S. large cap growth stocks and core U.S. bonds, you may miss some of these opportunities and carry more overall risk than you realize. Deliberate diversification across different asset classes, sectors and geographies can position you to participate more fully in global growth while managing inflation risk. For more detail on how different asset classes behave when inflation is high, Creative Planning’s piece on how to counteract inflation in your portfolio is a good reference.

2022: Back to the ’70s … sort of

Recent history shows how messy real-world environments can be. In 2022, markets grappled with a sharp inflation spike that felt reminiscent of the 1970s but with a stronger starting economy and a very aggressive Federal Reserve response.

Like the 1970s:

- Inflation hurt both broad bond markets and many stocks at the same time.

- Value stocks (both large and small) tended to outperform growth stocks as “hard asset” sectors like energy and materials held up better.

- Short-term bonds did better than long term bonds because rapidly rising interest rates hit long durations hardest.

But unlike earlier inflationary episodes, the U.S. dollar strengthened meaningfully as the Fed raised interest rates faster than many other central banks, attracting foreign capital seeking higher yields. That dollar surge held back international and emerging-market stocks from playing their usual diversification role in an inflationary period.

2022 Inflationary Period Performance Chart

Source: Ycharts. 12/31/2021-12/31/2022.

It’s a good reminder that no diversification strategy is perfect. Sometimes investments that usually move separately all get hit at once. The goal of diversification isn’t to eliminate short-term losses; it’s to manage risk over full cycles and reduce the odds of a catastrophic long-term outcome.

How About Private Investments and Alternative Investments?

So far, we’ve mostly talked about broad public stocks and bonds, but diversification can also extend to real estate, private markets and alternative investments.

- Real estate – Direct real estate and publicly traded real estate securities can offer income, potential inflation protection and diversification away from traditional stock and bond drivers.

- Private markets and alternative investments – Private credit, private real estate and private infrastructure often have return streams tied to cash flows that can adjust with inflation, which may help in inflationary environments. Private equity has historically performed well in disinflationary booms characterized by solid growth and lower interest rates.

- Commodities and commodity-related stocks – Commodities themselves don’t produce cash flow, but they can hedge inflation and supply shocks, while commodity-oriented value stocks can sometimes offer similar benefits with the added upside of earnings and dividends.

These types of alternative investments — accessed through private markets and other nontraditional asset categories — can complement traditional portfolios by adding differentiated sources of return and diversification, especially for investors with higher risk tolerance and longer time horizons. If you’re wondering whether alternatives are a fit for you, Creative Planning’s article on whether alternative investments could complement your portfolio and its overview of alternative investments outline key considerations and due diligence questions.

Diversification in Practice

In practice, a diversified portfolio designed to manage market volatility and different economic regimes often includes a mix of both traditional and alternative investments:

- Multiple asset classes – A blend of equities, fixed income and, where appropriate, real estate and alternative investments — not just a single mutual fund or index fund.

- Variety within equities – U.S. and international stocks, large cap and small cap stocks, and growth and value stocks, across sectors like technology, healthcare, finance and industrials, often accessed via broadly diversified index funds and ETFs.

- Different types of bonds – High-quality Treasuries and investment-grade bonds, plus short-term and (when appropriate) longer-term fixed income and possibly some high-yield or credit exposure to balance risk and return.

- Geographic diversification – Exposure beyond the United States to developed international and emerging markets to help manage country-specific and currency risk over the long term.

- Private markets and real assets (when appropriate) – For investors with the right time horizon, liquidity profile and risk tolerance, private investments and real assets can help reduce reliance on a single public market environment.

The exact mix depends on your financial goals, risk tolerance, time horizon and liquidity needs. That’s why we start with your plan and risk profile, then use diversification and asset allocation to build around them — not the other way around. If you’d like help determining the right strategy and asset mix for your situation, Creative Planning’s fiduciary investment management services are built around client-specific, diversified portfolios.

Why Diversification Still Matters

There will be years when it feels like diversification is letting you down. Maybe everything in your portfolio seems to be down at once, or a single hot sector your neighbor talks about is crushing your more balanced allocation.

Concentrated bets can feel great for a while, but they can also leave you exposed to severe drawdowns you may not be willing or able to endure. A portfolio diversified across different asset classes and different types of investments is designed to spread out that risk, even though it means you’ll rarely be the very top performer in any single calendar year.

Over a full investing lifetime, diversification can help:

- Can help reduce the impact of any single market fluctuation or downturn

- May provide more consistent progress toward your financial goals

- Can make it easier to stay invested through rough markets, which is critical for long-term success