How to Make Your Money Work for You During a Downturn

It’s never fun to watch the value of your portfolio drop during a market downturn. In fact, it’s often during downturns that investors panic and sell at the bottom, locking in their losses and demonstrating why pessimism does not serve investors well. Instead of selling at a loss, look for ways to position your portfolio to take advantage of the market’s eventual recovery. There are many opportunities during bear markets, as detailed below.

First, it’s important to understand that significant market downturns occur typically and are a normal part of the markets. On average, a 10 percent downturn occurs every 11 months. Typically, a bear market is defined as a period during which securities prices fall 20 percent or more from recent highs amid widespread pessimism and negative investor sentiment.

While a drop of 20 percent may sound scary, bear markets also offer opportunities. Following are three tips to help you capitalize on volatile market conditions.

Tip #1 When the market is down, avoid fear-driven selling

Fear-driven selling is the single biggest mistake investors make during market volatility. The COVID-19 bear market lasted a mere 33 days from February 19, 2020, to its trough on March 23, 2020, yet a lot of fear-driven selling occurred during this short timeframe.

By selling out and moving to cash, you can miss out on the three main opportunities of investing during a bear market.

- Rebalancing – selling high/buying low – Rebalancing is the process of realigning the blend of assets back to a target allocation when they drift out of balance due to market movements.

For example, let’s say you own stocks and bonds. In a bear market, when stock prices drop, your portfolio will own a smaller percentage of stocks compared to bonds. To rebalance your account, you sell a portion of your bonds to purchase stock, which boosts your stock percentage back to your desired target. The opposite would occur during a market upturn; your portfolio would end up with a larger percentage of stock, so rebalancing would lead you to sell stocks and buy bonds within the portfolio.

Periodically rebalancing your portfolio in this way is designed to allow you to sell high and buy low.

- Dividend reinvestment – Stocks and bonds often pay dividends and interest, which are an important part of an investment’s total return. Reinvesting your dividends allows you to:

- Grow your portfolio through the purchase of additional shares – When shares cost less during a market downturn, you’re able to buy more shares with the same amount of money.

- Take advantage of compounding interest within the portfolio.

These are two major benefits you sacrifice when you take your money out of the market.

- Tax-loss harvesting – Tax-loss harvesting is the process of realizing investment losses in order to lower your tax liability and limit the taxation on future gains. Many investors ride the ups and downs of the stock market by following a buy-and-hold strategy. While this strategy typically makes sense within an IRA, it’s often wise to consider tax-loss harvesting within your after-tax accounts.

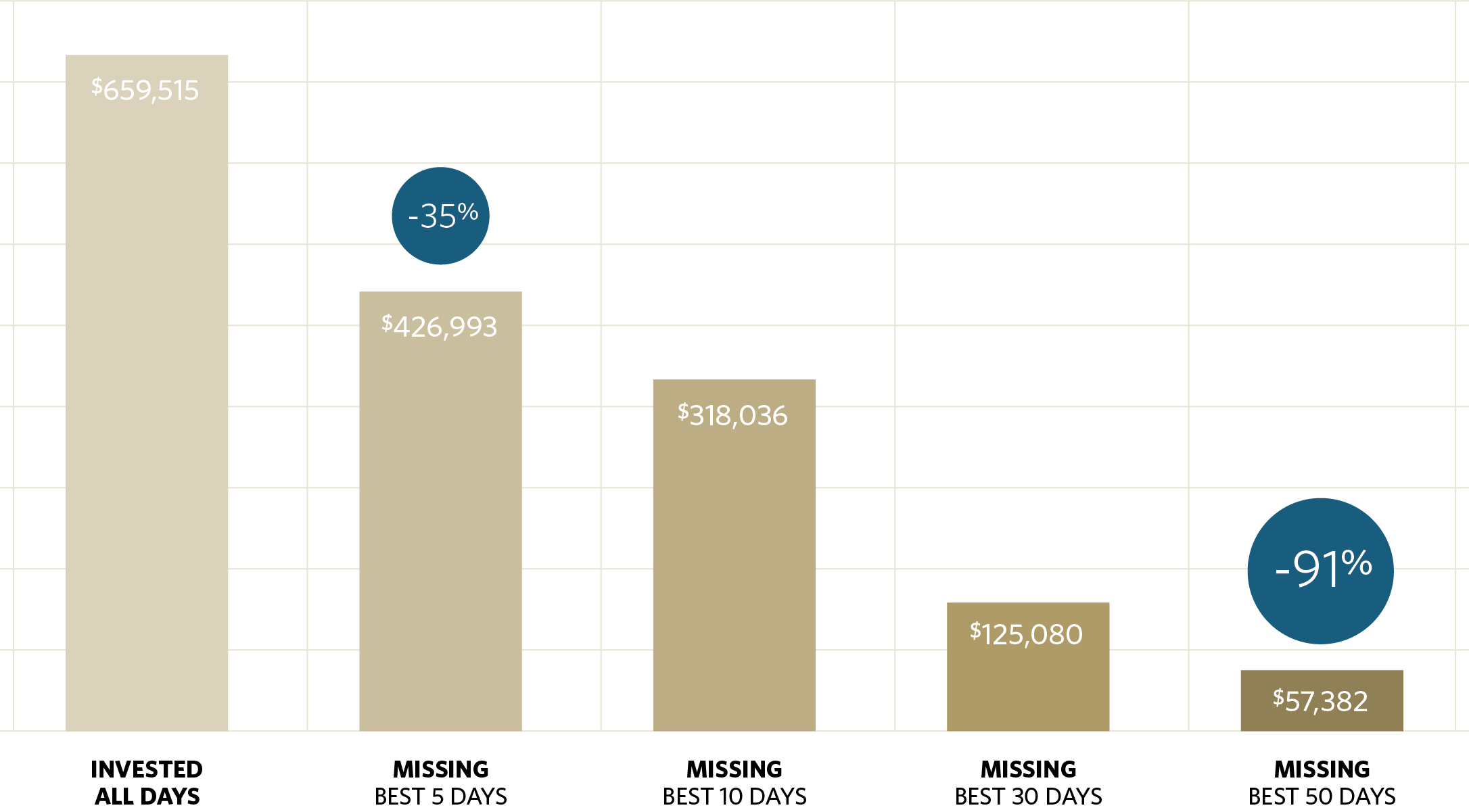

Investors are forward-looking. Market lows typically occur about four months before the beginning of an economic recovery. Warren Buffett offers wise words in his famous quote, “We simply attempt to be fearful when others are greedy and to be greedy when others are fearful.” It’s all about time in the market, as great opportunities can be missed when you take your money out. The following chart illustrates how missing just a few days in the market can greatly impact a portfolio’s performance.

Missing Out On the Best Days Can Be Costly1

Hypothetical growth of $10,000 invested in S&P 500 Index (January 1, 1980 – December 31, 2018)

Tip #2 The five-year rule

According to the five-year rule, any assets you plan to use within the next five years should be conservatively allocated. When structuring your investment portfolio, it’s wise to have enough conservative assets to cover your monthly expenses and any large purchases you plan to make during this timeframe (examples – college costs, weddings, new car, etc.) Your goal should be to have enough assets invested conservatively to avoid selling during a market downturn.

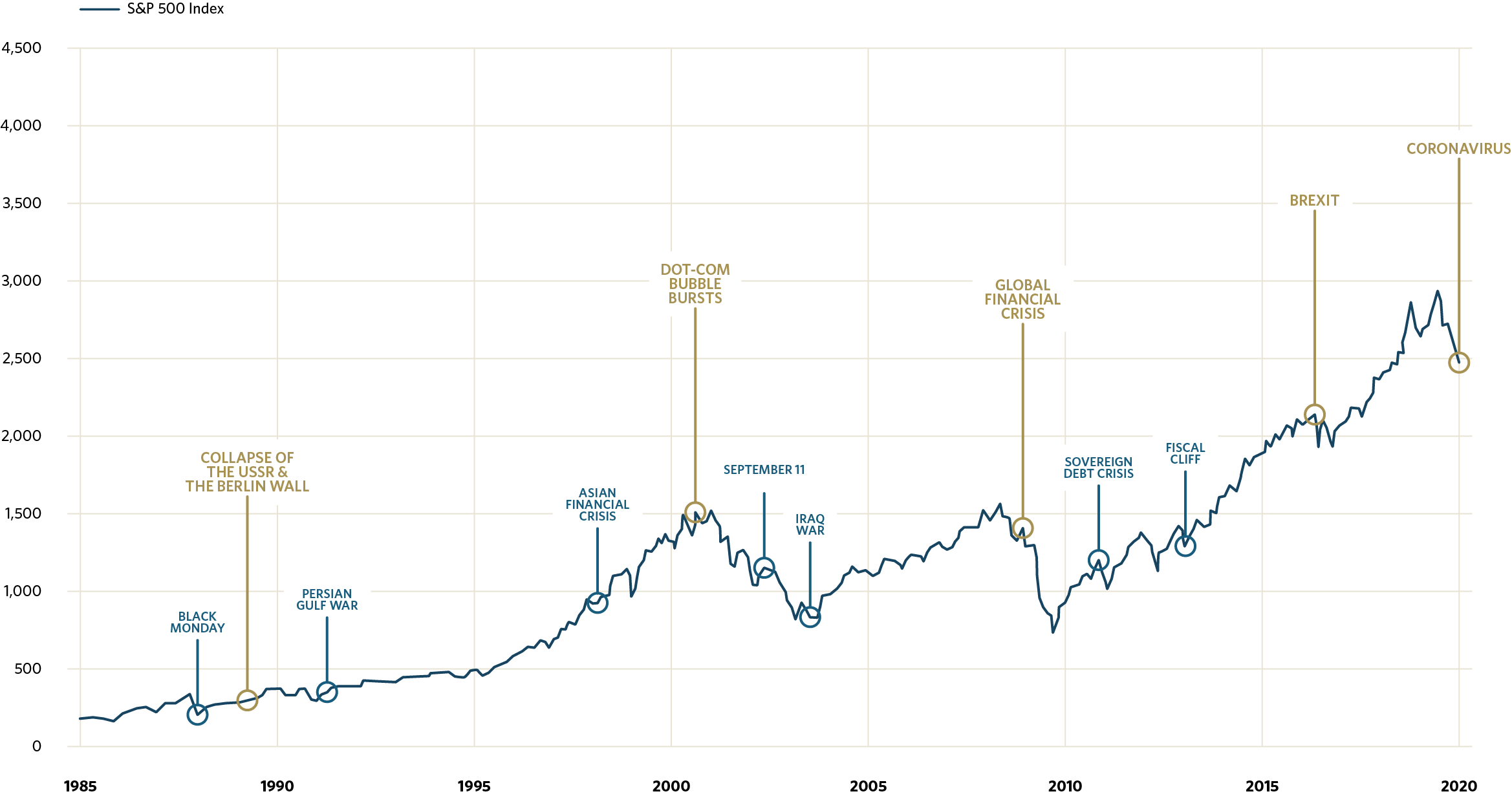

The following chart illustrates the duration of several historic recessions. Excluding the COVID-19 downturn, a typical downturn lasts approximately 18 months and the typical rebound takes approximately 36 months. If you are aggressively invested and need to withdraw funds during one of these market pullbacks, you may be forced to sell at an inopportune time.

Despite Market Pullbacks, Stocks Have Risen Over The Long Term2

Tip #3 Diversification

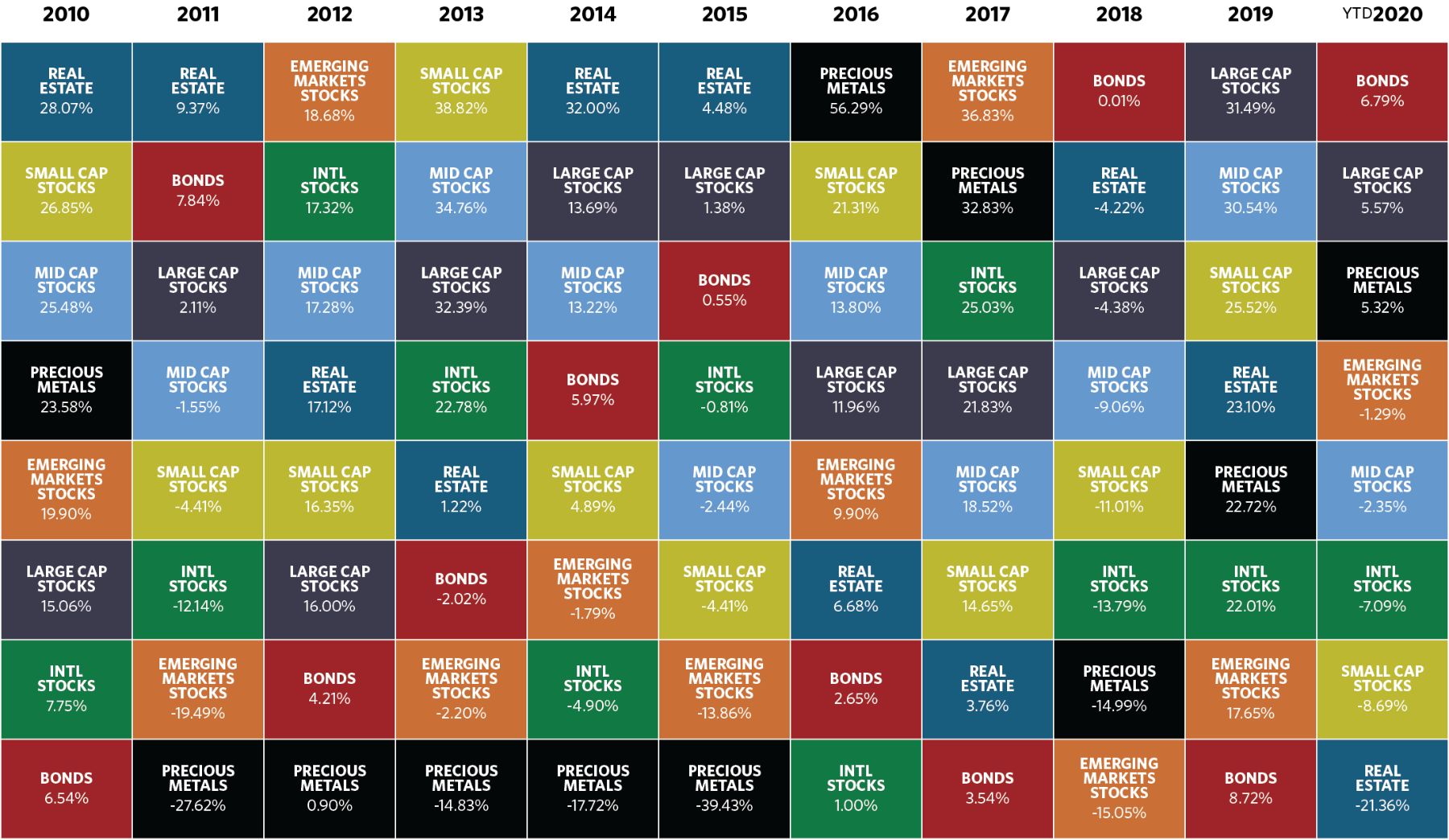

The chart below illustrates the importance of diversification across asset class types. As you can see, the various asset classes fluctuate greatly when it comes to performance. It’s important to maintain a diversified portfolio in order to allow this fluctuation to work to your advantage. History has taught us the best way to achieve higher returns and limit risk is to diversify across asset classes, sectors and geography.

Annual Returns for Selected Asset Classes3

Having a financial plan in place that is customized based on your specific financial situation, goals for the future, challenges and risk tolerance will help keep your emotions from getting the best of you during a bear market. When you have a solid plan in place, it can provide peace of mind of knowing that your investment portfolio is positioned to help you achieve your vision for the future, regardless of market volatility.

At Creative Planning, we work with clients to develop customized and comprehensive financial plans specifically designed to help them achieve their long-term financial goals. If you’re ready to start planning for your financial future, please contact us.