Key Takeaways

- A concentrated stock position can expose your portfolio and long‑term goals to outsized single‑stock risk.

- The tax cost of selling and the risk of holding are always in tension, so you need a plan that weighs both.

- Direct indexing, exchange funds, options and charitable strategies can all help manage concentrated stock exposure.

- The right mix depends on your net worth, tax picture, time horizon and comfort with volatility.

- A planning‑led advisor can help you evaluate trade‑offs and build a practical path forward.

Introduction to Managing Concentrated Stock Positions

If a single stock makes up a significant share of your investable assets, you may have a concentrated stock position. This situation often occurs when employer stock grows over time, you inherit a large position, you receive shares in a business sale or you simply hold on to a long‑term winner.

A concentrated position can feel like a success story, but it also introduces meaningful risk. If that one stock falls sharply, your wealth, liquidity and long‑term plans may all be affected at once. The challenge is finding a way to reduce risk without creating unnecessary tax drag.

That’s why managing concentrated stock positions usually isn’t about one dramatic move. It’s about understanding the trade‑offs, then building a plan that gradually improves diversification, manages taxes and keeps your broader goals in focus.

What Qualifies as a Concentrated Stock Position?

There’s no single threshold, but many investors start to view a holding as concentrated when one stock represents more than 10%-20% of investable assets or when a sharp decline would materially change their long‑term financial goals. It’s also important to look beyond a single brokerage account and include employer stock plans, options, retirement accounts and overlapping exposure through funds.

If both your income and your portfolio depend on the same company, your concentration risk may be even greater. When one company influences both your paycheck and your net worth, the downside risk isn’t isolated to your investment account — it can affect your day‑to‑day financial life as well.

Most concentrated positions build gradually, not intentionally. Common paths include long‑tenured employment with stock compensation, business sales paid in public company shares, inherited stock, and outsized growth from a single investment.

That’s one reason these positions can be easy to overlook. What starts as a valuable part of a portfolio can slowly become the dominant driver of risk and return. No matter how the position developed, the planning question is the same: how do you respect the role that stock played in building wealth while reducing the downside risk it creates going forward?

Understanding the Risks of Concentrated Stock Positions

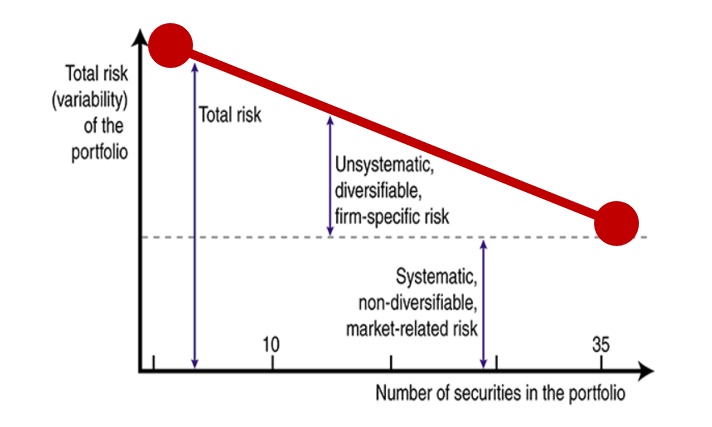

One of the biggest risks is company‑specific risk, also known as unsystematic risk or idiosyncratic risk. A single stock is vulnerable to business setbacks, regulatory issues, leadership changes, product failures and competitive pressure in ways that a broad market index isn’t.

A concentrated position can also create asset class risk if too much of your wealth is tied to one segment of the market. When the stock is tied to your employer, you may face career risk as well, meaning a downturn could affect both your paycheck and your portfolio.

Caption: As the number of securities in a portfolio increases, unsystematic (company-specific) risk decreases, while systematic (market-wide) risk remains. Diversification can help eliminate the former but not the latter.

There’s also tax exposure to consider. A large low‑basis holding may come with significant unrealized gains, which means selling to diversify can trigger a meaningful capital gains tax bill. This tension between reducing risk and managing taxes is what makes concentrated stock planning so complex.

These risks don’t always show up all at once. The position may feel manageable while markets are rising then suddenly feel much riskier during volatility or a company‑specific setback.

For additional perspective on the emotional side of concentration risk, Creative Planning’s The Double‑Edged Sword of Concentrated Holdings adds helpful context.

The Tax Trade‑Off: Capital Gains and Concentration Risk

One of the main reasons investors hold concentrated positions is the desire to defer taxes. Selling appreciated stock can trigger capital gains tax on realized gains, but continuing to hold it leaves you exposed to ongoing concentration risk.

There’s no one “right” answer for how quickly to diversify. Instead, the goal is to weigh:

- How much of your net worth is tied up in the stock

- How much unrealized gain you have and the projected tax cost of realizing it

- Your time horizon for using the funds

- Your comfort with volatility and drawdowns

In some cases, it may make sense to accept more tax in the near term to significantly reduce risk. In others, you might prefer to diversify more slowly, using tools that help manage taxes along the way.

The rest of this article walks through several strategies investors use to address concentrated stock positions. These aren’t mutually exclusive, and many effective plans use a combination rather than a single tactic.

Strategy 1: Build a Staged Selling Plan

The most straightforward way to address a concentrated position is to sell shares over time and reinvest the proceeds in a more diversified portfolio. A staged selling plan might involve:

- Setting a target for how much of your net worth you want in the stock

- Developing a divestment timeline (for example, three to five years)

- Pre‑committing to sell a set number of shares or a set dollar amount at regular intervals

This type of plan can reduce the emotional burden of deciding “when” to sell, as you’re following a playbook rather than reacting to each market move. It can also help spread realized gains across multiple tax years, which may keep you in a more favorable bracket.

You and your advisor can also coordinate sales with other parts of your tax picture, such as harvesting losses elsewhere in the portfolio, making charitable gifts or the timing of other income events.

Strategy 2: Use Direct Indexing to Diversify Tax‑Efficiently

Direct indexing involves owning the individual stocks in an index directly rather than through a mutual fund or exchange‑traded fund. This structure makes it possible to customize the portfolio around your concentrated position while still targeting index‑like exposure.

For example, if you hold a large position in a technology company that’s part of a major index, a direct indexing strategy might:

- Underweight or exclude that stock in the index sleeve

- Add positions in other sectors or companies to offset some of the concentration

- Use tax‑loss harvesting opportunities across the rest of the portfolio to help offset realized gains over time

The goal isn’t to eliminate the concentrated position overnight but rather to gradually reduce its impact by building a more diversified, tax‑aware structure around it.

For a deeper look at how direct indexing and enhanced direct indexing are implemented, see Direct Indexing: Tax‑Efficient Diversification for Concentrated Stock and Enhanced Direct Indexing.

Strategy 3: Explore Exchange Funds for Diversification Without Immediate Tax Consequences

Exchange funds are private investment vehicles that allow investors to contribute shares of appreciated stock in exchange for an interest in a diversified portfolio, usually without triggering immediate capital gains tax.

In a typical structure, you contribute your stock to the fund and receive units of the fund in return. The fund holds a diversified pool of contributed stocks from many investors, and you remain invested in the pooled portfolio rather than in your original shares.

Exchange funds aren’t right for everyone. They require a significant minimum investment, are generally available only to accredited investors and qualified purchasers, and have lockup periods and limited liquidity. Fees and tax treatment can also be complex.

Still, for some investors, they can be a way to diversify without triggering an immediate capital gains event, especially when combined with other strategies.

Strategy 4: Consider Options‑Based Strategies

Certain options strategies can help manage risk around a concentrated position, though they add complexity and aren’t appropriate for all investors. Common approaches include:

- Covered calls, where you sell call options against your stock, potentially creating a disciplined way to reduce your position if the stock is called away

- Protective puts, where you buy put options to place a floor under the value of your position for a period of time

These strategies come with trade‑offs in terms of cost, complexity and the range of potential outcomes. Options can also have tax consequences that differ from simply buying and selling stock. They’re most often used as part of a broader plan rather than as a stand‑alone fix.

Before implementing any options strategy, work with an advisor who understands the investment and tax implications and can help you decide whether derivatives belong in your tool kit.

Strategy 5: Incorporate Charitable Planning

Charitable strategies can help you reduce concentrated positions while supporting causes you care about. Common structures include:

- Donor‑advised funds, where you contribute appreciated shares, potentially receive an immediate charitable deduction (subject to limits) and then recommend grants over time

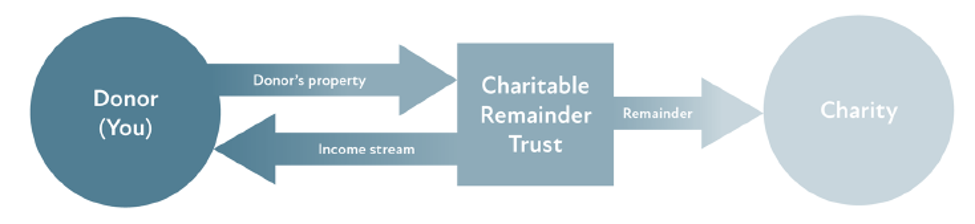

- Charitable remainder trusts, where appreciated stock is contributed to a trust that can sell the shares without immediate capital gains, then pay income to you or other beneficiaries for a period of time with the remainder going to charity

By donating appreciated shares instead of cash, you may be able to avoid capital gains tax on the contributed shares while still achieving your giving goals. You can then use cash that would have gone to charity to repurchase a more diversified mix of investments, helping to reshape your overall portfolio.

These strategies involve legal, tax and administrative considerations. They’re usually most effective for investors who already have philanthropic goals and can benefit from both the tax and planning aspects of structured giving.

| Sell stock and donate proceeds | Donate in-kind shares | |

|---|---|---|

| Current market value | $1,000,000 | $1,000,000 |

| Cost basis | $200,000 | $200,000 |

| Embedded capital gain | $800,000 | $800,000 |

| Capital gains tax owed (23.8% total rate) | $190,400 | $0 |

| Total charitable contribution | $809,600 | $1,000,000 |

| Charitable deduction amount | $809,600 | $1,000,000 |

Strategy 6: Coordinate With Your Broader Financial Plan

You shouldn’t manage a concentrated stock position in isolation. Your concentrated position affects — and is affected by — many other parts of your financial life, such as:

- Retirement planning, including your target retirement age

- Cash flow needs, including upcoming purchases, education funding or business investments

- Estate planning, including charitable bequests and your goals for heirs

- Risk management, including how much volatility you can tolerate and still stay on track

For example, if you plan to retire in the next few years and rely heavily on portfolio withdrawals, you might prioritize reducing concentration risk even if it means realizing more gains today.

If you’re earlier in your career and have a longer time horizon, you might have more flexibility to stage diversification and coordinate with other events.

Consider a hypothetical investor in their early 60s with 45% of their investable assets in a single technology stock and plans to retire within five years. Working with an advisor, they build a plan to gradually reduce the position to 15% by combining a three‑year staged selling schedule, direct indexing around the remaining shares and annual charitable gifts of appreciated stock. Along the way, tax‑loss harvesting in the rest of the portfolio helps offset some realized gains, and the overall allocation becomes more diversified and better aligned with their retirement income needs.

| Primary Goal | Tax Impact | Complexity | Best Fit | |

|---|---|---|---|---|

| Structured Selling | Orderly liquidation and diversification | Potential immediate recognition | Medium-High | Concentrated stock with near-term liquidity needs |

| Direct Indexing | Customization and tax optimization | Enhanced tax-loss harvesting | High | Tax-sensitive investors wanting precise control and tracking |

| Exchange Fund | Immediate diversification without tax event | Deferred capital gains | Medium | Large concentrated positions with long horizons |

| Options Hedging | Downside protection and income | Complex, options-specific rules | High | Managing risk in core holdings or generating yield |

| Charitable Planning | Tax efficiency and philanthropy | Large potential deductions; bypass gains | Low-Medium | Charitably-inclined investors with appreciated assets |

Managing concentrated stock positions is ultimately about aligning risk, taxes and long‑term goals. The best plans acknowledge both the upside that helped build your wealth and the danger of letting one stock carry too much weight in your future.

Creative Planning Advisor Insight

“When a single stock has created a meaningful portion of your net worth, the goal usually isn’t to fix everything at once. It’s to build a plan that respects the tax realities, reduces risk over time and gives your future more than one company to depend on.” — Troy Kuhn, Wealth Manager, CFP®, MBA, CAIA®

Frequently Asked Questions

What’s considered a concentrated stock position?

Many investors and advisors start to treat a position as concentrated when one stock represents more than 10%-20% of investable assets or when a large decline would meaningfully affect long‑term plans.

Why is a concentrated position so risky if the company is strong?

Even strong companies face risks that are hard to predict, including regulatory changes, competitive threats and leadership shifts. A diversified portfolio can absorb setbacks better than a portfolio dominated by a single holding.

Why not simply hold and avoid capital gains tax?

Deferring tax by holding the stock may feel attractive, but it leaves you exposed to the risk that the stock declines before you diversify. In many cases, the potential downside of a sharp loss can outweigh the tax savings from continued deferral.

Which strategy should I use to address my concentrated position?

There’s no single best approach. Most effective plans use a combination of selling, direct indexing, charitable strategies and, in some cases, tools like exchange funds or options, all tailored to your goals, tax picture and risk tolerance.

Talk With a Planning‑Led Advisor

A concentrated stock position can be both a sign of past success and a source of future risk. A planning‑led advisor can help you quantify that risk, understand your tax options and design a step‑by‑step strategy to move toward a more durable, diversified portfolio.