Are Bonds Still Worth Owning?

Some of you may have seen the movie What About Bob? starring the always entertaining Bill Murray and Richard Dreyfuss. Murray plays Bob Wiley, a troubled patient with multiple phobias who follows his self-centered, Type A psychotherapist, Dr. Leo Marvin (Dreyfuss), on vacation. Most of the movie is about Bill Murray’s character driving Dr. Leo crazy with his wild antics to the point that Dr. Leo is rendered catatonic and institutionalized — which brings me to bonds. No, I’m not saying that bond investors will meet a similar fate, but the latest decline in bond prices (caused by rising interest rates) may be driving investors a little crazy.

Background

To put things into context, let me summarize where we’ve been. The COVID-19 outbreak in 2020 brought the global economy to a standstill, requiring the Federal Reserve (Fed) and central banks all over the world to force short-term interest rates to zero and conduct further stimulative policies to sustain economic growth. The combination of those policies and the Ukraine/Russia war have translated into inflation throughout many areas of the economy, which central banks must now fight by raising rates and potentially selling bonds back into the market to drain liquidity from the system.

The ultimate goal is to slow down economic activity just enough to reduce inflation but not so much as to cause the economy to go into a recession. This shift in policy is causing market participants to brace for higher interest rates and thus sell bonds (and push rates up) to appropriate levels that compensate investors for this risk and the risk that inflation will not be able to be tamed. This caused the Bloomberg U.S. Aggregate Bond Index to decline 1.54% in 2021 and 6.89% as of March 25, 2022.

With this type of environment, it would be logical for clients to ask the following questions:

Why should we own bonds at all if they are losing value?

Let’s start with the basics. Like in sports where each position has a specific role within the team framework, so too should each investment play a unique role in your portfolio. The purpose of some is to achieve high, long-term returns, while others endeavor to outperform in inflationary environments, etc. Historically, one of the main purposes of holding bonds is to add ballast in your portfolio when stocks have significant declines.

In the chart below, you can see how bonds have performed in all negative calendar years for stocks. There are only a few years where bonds lost value at the same time as stocks, and there has never been a year where they have been negative when stocks finished the year down more than 20%. The reason for this is that major, sustainable market downturns often occur around recessions, and recessions are almost always disinflationary or deflationary events that make bonds more attractive to investors.

Weren’t interest rates higher in previous years than they are today?

Yes, but remember that the 10-year Treasury bond yield was 2% heading into 2020 just prior to the COVID-19 downturn. This is lower than it stands today at approximately 2.5%. Yet, when stocks declined in 2020, 10-year Treasury bonds went up 8%.1 In addition, the federal funds rate was 1.75% prior to the COVID-19 downturn. Compare that to today, where the market has already “priced in” a federal funds rate of approximately 2.25%. More on this below.

With inflation running at approximately 8%, aren’t we losing purchasing power? Won’t interest rates continue to go up?

Certainly, with bond yields so low the “real” (after inflation) return potential for the foreseeable future is diminished, which makes other assets more attractive. With that said, while inflation is running at very high year-over-year levels at this time and could sporadically plague markets for years into the future, that doesn’t mean inflation can’t come back down as we progress throughout the year. There’s a reasonable case to be made that the economy could hit a slow patch in the months/quarters ahead due to multiple forces, including the reduction of fiscal stimulus, an expensive U.S. dollar (which makes U.S. exports less competitive), high oil prices and, now, higher interest rates. Slowing economic growth could cause inflation to pull back, allow the Fed to slow down its interest rate increases and send bond prices back up. It’s important to remember that even in the inflationary 1970s, there were multiple times when interest rates moved lower for periods of time.

In addition, rising interest rates, while painful at first, are a good thing for long-term bond holders, as the total returns generated from bonds come mostly from the interest rate you receive. As interest rates move up, shorter-term bonds or bonds that mature can purchase new bonds at higher interest rates, thus leading to higher future returns.

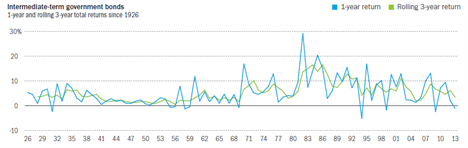

The chart below shows how Intermediate-term government bonds have performed throughout history over rolling one- and three-year year periods. You will see that some of the highest returns came during the late 1960s to early 1980s, when inflation was surging and the 10-year Treasury rate quadrupled from 4% to 16%.

Another thing you will notice from the chart is that high returns often follow poor one- and three-year returns. For lack of a better, more sophisticated term, we’ll call this the “double whammy” effect. It’s when bond holders are receiving higher income due to higher interest rates and then receive capital appreciation when bond prices eventually increase in value (yields going back down) due to a slowdown in the economy. Prices can also go up as investors start rotating away from stocks and toward bonds to lock in higher rates.

A wonderful example of this was in 1994 when the Fed raised rates by 300 basis points within 12 months, resulting in negative returns from bonds that year. However, that was followed by excellent annual returns in the following years as the economy slowed and the Fed had to cut rates again.

Isn’t the Fed just starting to raise rates? Won’t that further hurt bond returns?

You’ve likely read articles, such as this one, preaching how the stock market is a forward-looking indicator that moves ahead of the economy. This explains why stocks bottomed in March 2020 well before the economy rebounded from the effects of the COVID-19 shutdowns. The same can be said for the bond market. With each passing day, the market is trying to price in all various inflation scenarios ahead and the resulting actions of the Fed in the year (and years) ahead.

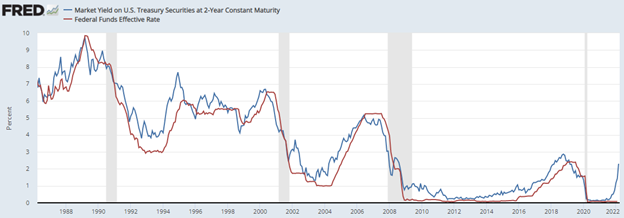

This can be seen in the chart below that compares the two-year Treasury bond rate (in red) to the federal funds rate (in blue). You will see that the two have a very tight correlation and that the federal funds rate usually follows the two-year Treasury. With the two-year Treasury rate at approximately 2.3%, the market has already “priced in” the Fed raising rates to that level. Thus, should the Fed raise rates to that level, it should have minimal, if any, impact on bond prices going forward.

What should I do?

As mentioned above, the low interest rate environment will likely be a headwind for bond investors for quite some time, especially when adjusting for inflation. Thus, every investor has a few choices with respect to how they want to deal with the current environment.

- Do nothing – Yes, this is an option. If your financial plan works even if bonds have lower returns in the coming five to ten years and your risk tolerance doesn’t allow you to increase risk in your portfolio, keeping your existing bond allocation may make sense. Hopefully this article shows you that eventually bond returns tend to work out. After all, unless your bonds default (which is extremely rare if you hold high-quality bonds), you will get your principal back with interest. In addition, higher interest rates lead to higher longer-term returns.

- Increase stock exposure– It is widely known that stocks have a high probability of outperforming bonds over long periods of time. If you have enough cash and bonds to satisfy your short-term cash flow needs (approximately five years is a good rule of thumb), you may want to invest in stocks with the remaining portfolio. Having this five-year buffer reduces the risk of having to sell stocks at poor prices, even in a severe downturn.

- Add or increase private investments – I certainly know many clients who would rather not increase the risk of their portfolio by adding to stock exposure. There is never a one-size-fits-all solution in any investment environment. For these clients and others, investing in private investments such as private real estate, private debt and private equity may be appropriate. While these options aren’t lower risk and don’t have the unique characteristics of bonds that make them a good ballast in the portfolio, they are priced in a way that tends to reduce volatility, which helps investors stay with the strategy to reap the long-term rewards. Private investments are often priced monthly or quarterly, thus avoiding the emotional day-to-day experience of the public markets. In addition, they’re valued in similar ways to your house (third-party appraisals, “comps” or long-term fundamentals), and my guess is that you don’t check the price of your house on a daily basis. While private investments aren’t for everyone, they may be of use in today’s world.

Most importantly, your Creative Planning advisor is here to help you both evaluate your choices and make the best decisions based on your specific goals, financial plan and unique personality. We look forward to guiding you in the years ahead.

Footnotes:

- Datastream, GMO, https://www.gmo.com/americas/research-library/2q-2020-gmo-quarterly-letter/. Note: Short rates are levels as of 1/31/2020 and bond returns are the returns from 2/19/2020 to 3/23/2020.