It’s 84 days to Election Day and we have our match-up: Trump/Pence v. Biden/Harris

Because it’s 2020, we are on the brink of one of the most contentious elections of our lifetime and given that every race from Bush v. Gore on has been particularly hostile, that is saying something. I have vivid memories of encouraging clients to stick with their portfolios, and in some cases why they should remain U.S. citizens, after the election of President Obama, and again after the election of President Trump. The reality is elections have always been contentious. Those of us who long for the good old days when things were civil really don’t remember the old days or know their history. During the John Adams v. Thomas Jefferson campaign, each had headline ads. Here was John Adam’s key advertisement:

IF YOU ELECT THOMAS JEFFERSON

MURDER, ROBBERY, RAPE, INCEST, and ADULTRY will be practiced throughout the land.

Are you prepared to see your dwellings in flames… FEMALE CHASTITY VIOLATED, or children writhing on the pike?

Thomas Jefferson, let’s just acknowledge, didn’t take the high road:

JOHN ADAMS IS……

busy IMPORTING MISTRESSES from Europe or trying to marry one of his sons to the daughter of King George.

He is a HIDEOUS, HERMAPHRODITICAL CHARACTER with neither the force or firmness of man, nor the gentleness and sensibility of a woman.

Dear goodness, what a mess. So much for the good old days. But something is different now. We no longer only see an ad in a paper or on a flyer. We get the news we want, when we want it, and have the luxury (or curse) of only seeing the sort of news we want to see. We also now have social media, allowing for real time, round the world political commentary, with often the worst of the worst on both sides amplified by those with other agendas. So, here we are, on the brink of yet another historic election, emotions raw for so many reasons, around the clock news, social media and – oh by the way – a pandemic. It’s no wonder I have already spoken with both liberal and conservative clients regarding their Plan B – meaning which country they should move to – if their candidate doesn’t win. I haven’t had my inbox blow up with hate mail in a while, usually accusing me of being too liberal or too conservative, so let’s dive in!1

Looking at modern history, the markets have gone up under most presidents. Why? Because that’s what the market generally does over time. Part of the market’s return is simply inflation, some is dividends, and some is attributable to the growth of companies. Step away from the hysteria for a moment and think about how you and everyone you know has lived over the last dozen years. After President Obama won, did you still go out to eat and buy stuff? After President Trump won, did you still go out to eat and buy stuff? For nearly all of us, the answer is ‘yes’. We used Amazon more, our iPhones more, kept going to Chipotle.2 And that’s why the markets went up.

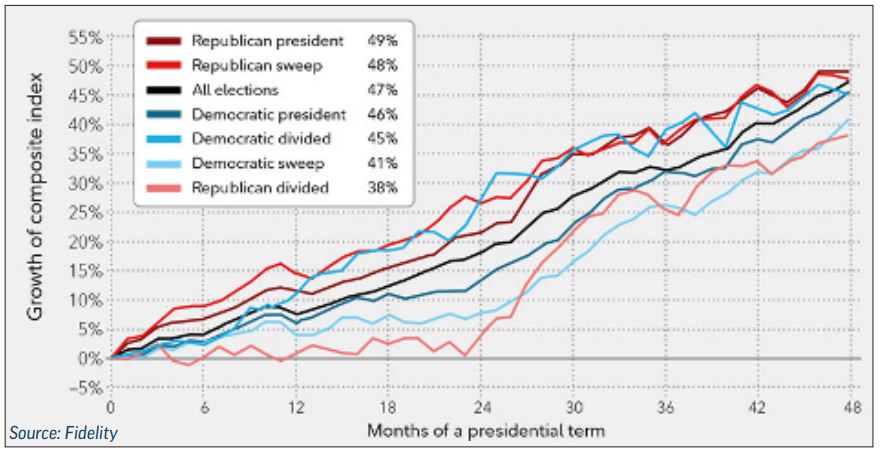

Now, I know what you are thinking. You’re thinking that simple performance summary doesn’t tell the full story because it doesn’t address situations where there is complete power by one party. So, let’s address what happens under the scenario where either party sweeps, or for that matter, any scenario. This chart gives us one broad message: the market tends to go up about the same amount, regardless of the scenario. Shocking, I know, but true.

Now, you might say, that’s all in the past and this is different. Yes, every election is different – there is no question about that. But let’s examine our two options here. First, President Trump has promised to leave all tax cuts in place and has made some public comments regarding potential further cuts, though he has not settled on a firm policy. Biden has started to clarify his economic positions and we do know quite a bit about his plans. Biden proposes a return of the highest income tax rate from 37% to where it stood under President Obama, at 39.6%. In a more substantive move, Biden’s payroll tax plan would increase payroll taxes. Every employer and employee each presently contribute 6.2% of the employee’s earned income towards social security via payroll taxes. This payroll tax only applies to the first $137,700 of income. Biden proposes having the tax applied on the first $137,700 and on all income over $400,000. Biden’s plan proposes changing the capital gains rates to match ordinary income tax rates for those making over $1 million per year, thus changing the highest capital gains rate from 20% in many cases to 39.6%. Under current law, when someone dies, their heirs can sell their assets with no capital gains taxes due. For example, if someone has a property or stock they bought for $100,000, and on their death it’s valued at $150,000, today the heirs can sell it for $150,000 with no income taxes due. Under Biden’s plan, there is no ‘step up’ in basis and taxes would be due on the $50,000 gain. When it comes to the corporate tax, Biden proposes eliminating half the Trump tax cut, increasing the rate from 21% to 28%.

Now, consider that for all these tax increases to happen, Biden needs to stick with these objectives through the election and likely needs a sweep to get them all through. Even with a sweep, compromises tend to be the norm for a variety of reasons. Finally, the timing of the cuts would depend largely on the strength of the economy. It is highly unlikely, for example, that all these tax increases would be passed if the pandemic continues, or we are in or near a recession for other reasons. If there is a blue sweep, and all the proposals stick, and all pass, the market would likely make a one-time, modest downward adjustment to account for the corporate tax increase, just as it made a modest, one-time upward move to account for the tax cut. It is estimated the one-time market adjustment, pricing in only the tax consequences of the proposed legislation, could range from 6% to 8%. Of course, there are a lot of ‘ifs’ in there, and it’s important to note the market is dynamic and impacted by many factors beyond corporate and other tax rates.

What is clear is that if these tax proposals pass, they will have significant implications for high income earners, those with capital assets like real estate, businesses and stocks – and for those who will face a tax burden, that may change their behavior. For those who live in high income tax states, it may be the ‘final straw’ that results in moving to another state. Take a high income California resident, for example, who already pays a 13.3% state tax rate. Their highest income tax bracket moves to 39.6%, and if they are a business owner, they now pay 12.4% in payroll taxes as well, bringing their incremental tax rate to 65.3%. On top of this, some cities in California also have a tax and the state is considering a state tax hike. People, as we all know, are different, and will make different decisions. Some may decide it’s not worth it to continue to work, some may move, and many will just continue on with no changes.

The ultimate takeaways? First, most Americans will see a minimal change to their tax situation should Biden win, even if there is a sweep. Second, high income Americans, and those who make over $1 million per year and plan to sell capital assets like stocks, real estate or a business, could see a dramatic change to their tax picture and will adjust the timing of their purchases and sales to mitigate some of the increase. Those who make a few hundred thousand a year or more in high income tax states may make changes that impact state revenues.

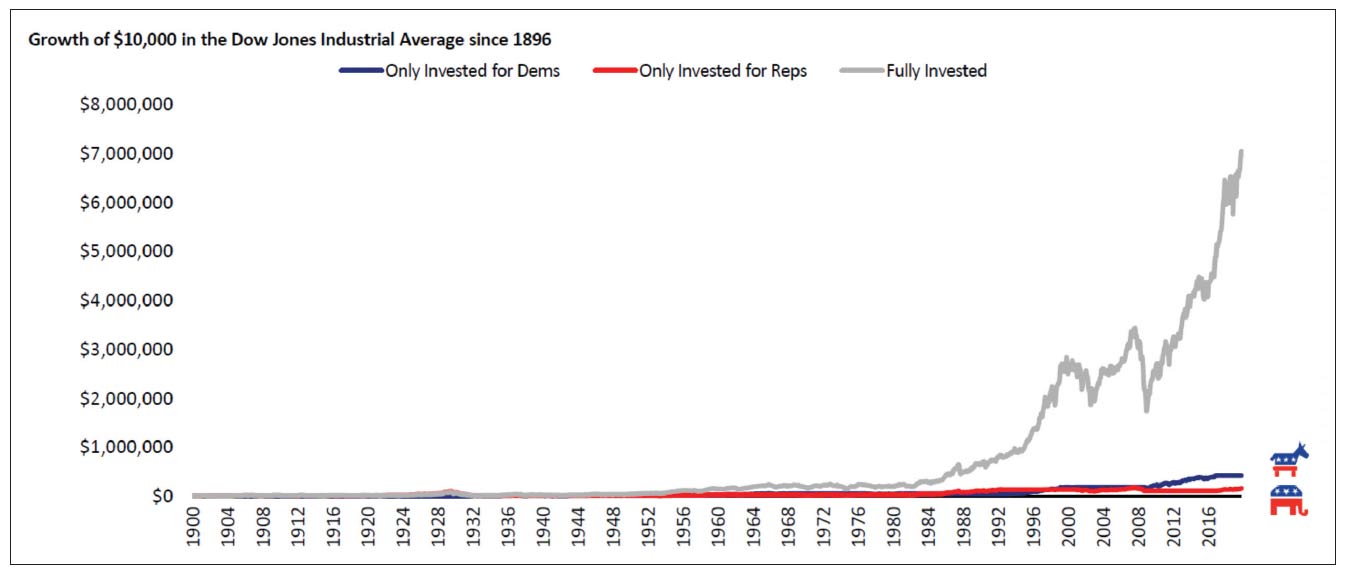

And finally, and to reinforce the main message of this letter, there is a big difference between what tax hikes mean to individuals compared to markets. Markets tend to find a way to perform, regardless of who is in office, and despite any changes in tax policy. This chart tells the story quite nicely.

Sources: Haver, Invesco, 12/31/19

As always, we will be prepared to advise you regarding your personal situation as soon as any new tax plan comes into focus, just as we did with the CARES Act, and in years prior, with Fiscal Cliff planning. For individuals, tax planning may move front and center in 2021. As for the markets, the smart money is betting that four years later, American companies, and companies all over the world, will most likely do just fine. And that means the markets will most likely do what they tend to do – continue onward and upward. We are humans and we will always have our strong opinions and our beliefs about what is best for the country, our thoughts about what is right and what is wrong, what is fair and what is not, and what policies create the best outcomes.3 But the markets? The markets are laser focused on one thing – and only one thing – all the time: future corporate earnings. The markets, you see, don’t bleed blue or red, only green. So go ahead and be passionate about your candidates, and by all means exercise your right to vote. But know the market doesn’t care who you think is wonderful, or who you think is crazy, and as it did after Presidents Obama and Trump each respectively won, it tends to punish those who tried to outsmart it.

Footnotes

- Writing newsletters in 2020 is not as fun as it usually is.

- Somehow Chipotle has worked its way into three of my newsletters. I need to stop writing these at midnight. Also, Chipotle is a horrible thing to crave at midnight, because it isn’t even open; but thankfully I don’t crave Taco Bell, which is open and could actually be fulfilled, and would greatly reduce my life expectancy.

- And each of us is, of course, 100% correct about every single major issue.