Tips for Prioritizing Your Spending

If you, like me, take time to meditate, you may agree that it is a tedious journey. However, if you can string together enough days of mindfulness, the effects are real. Every day, I make an effort to start with the meditation mantra, “clear away and bring forward.” This mantra reminds me to start my day with intention, and it can be infused into every aspect of daily life. Think intentionally, speak with intent and use time with intention. Taking this one step further, spend with intention. Or, more specifically, build a framework on the meaning behind how you spend money and, through that process, identify your personal spending values.

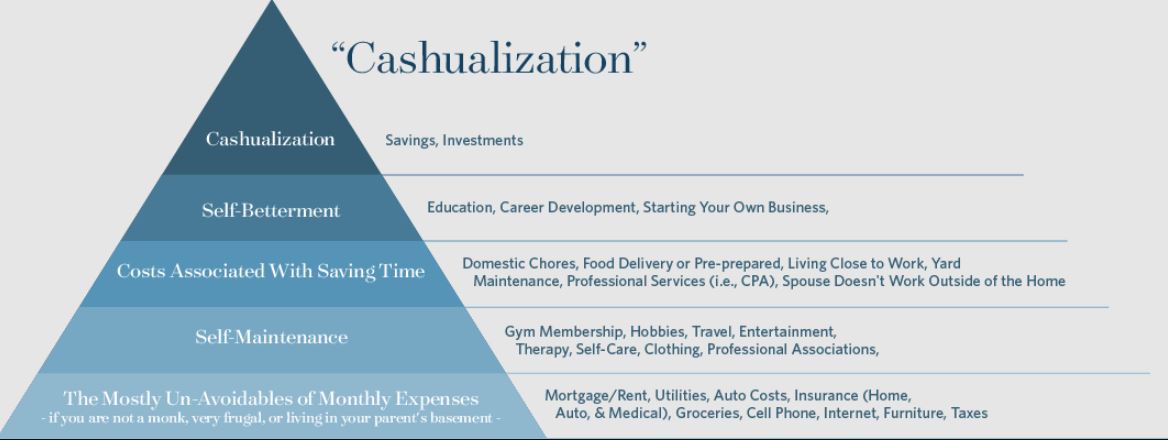

In building this framework, it can be helpful to identify your spending priorities. Much like Maslow’s Pyramid,1 you can build your spending framework by starting with basic needs and moving through various stages as you progress toward your financial goals. The idea is that the higher up the hierarchy you go, the more you create a better version of your life.

The (mostly) unavoidable expenses

The base of the pyramid consists of mostly unavoidable expenses, including:

• Mortgage/rent

• Utilities

• Auto costs

• Insurance (home, auto and medical)

• Groceries

• Cell phone

• Internet

• Furniture

• Taxes

These expenses are the tedious and mundane spending required to maintain a basic lifestyle. In correlation to Maslow’s Pyramid, they are the basic needs. You need a roof over your head, a car to drive, food to eat and a cell phone to stay connected (or to waste time). These not-so-fun expenses often take up the majority of an individual’s monthly budget.

As you work and earn money, you have your first chance to begin assigning value to some of these items. For example, do you value a certain zip code for better schools? If so, your housing and property taxes may increase. Do you want to drive an expensive car? Plan on spending more on auto costs and insurance. Most importantly, ask yourself if spending more in this category will stunt your ability to move up the pyramid. If so, this is another value you choose to accept.

If you are just starting out, it can be helpful to delay these expenses for as long as possible. Limiting your unavoidable expenses early on allows for more career path options. If you are already deep into the responsibilities of a mortgage/rent, a car and all the rest, it is important to keep these expenses within your monthly budget so you can more easily move up the hierarchy.

Self-maintenance

The next level of the pyramid is self-maintenance. This can include:

• Gym membership

• Hobbies

• Travel

• Entertainment

• Therapy

• Self-care

• Clothing

• Professional associations

Self-maintenance is about experiences that help you feel whole and provide a sense of community. These expenses allow you to spend time doing things you enjoy with friends and family. These are optional costs, but they can play an important role in helping you become a happier, healthier version of yourself. Self-maintenance expenses are budgetary items that require extra planning, as they can fluctuate greatly from month to month. Your value question at this level is, “How can I spend to ensure an adequate level of self-maintenance without hampering my ability to move up the pyramid?”

Time saving

The next level of the pyramid brings us to costs associated with saving time, such as:

• Domestic chores

• Food delivery or pre-prepared meals

• Living close to work

• Yard maintenance

• Professional services (i.e., CPA)

• A spouse who doesn’t work outside the home

I often listen to podcasts when I am driving. The Tim Ferris Show2 is one of my favorites. Tim interviews elite people across various industries, including CEOs, top athletes, scientists and more. He often talks about the importance of delegating the to-dos you least enjoy. If you are able to delegate these things, you give yourself the freedom to spend more time doing what you love. As a wife and mom of two teenage boys with a full-time career, I understand that time is a finite commodity. Can you live without someone doing your housework, taking care of your yard or preparing your taxes? Absolutely. However, based on your values and priorities, you may determine that your time is more important to you than the cost of delegating these tasks. As an example, the following table breaks out a hypothetical week for someone who works full-time. There are 168 hours in a week, and I have assumed here that this individual sleeps 56 hours and works 40 hours.

In this example, 168 hours minus 126 hours leaves 42 hours a week in discretionary time. Add in other miscellaneous chores, such as doctors’ appointments, home maintenance projects, meetings and teacher conferences, children’s sporting events and volunteer obligations, and this individual likely has very little time to his/herself each week. What’s the easiest way to add more time? Delegate the domestic tasks.

At this level of the pyramid, ask yourself, “If I allocate more of my financial resources toward reducing my time obligations, how will I take advantage of this extra time?” and, “Will the extra time help me and my family move up the pyramid and improve our lives?” These are important questions that can give you great insight into your values.

Self-betterment

The next level of the pyramid is self-betterment. This includes:

• Education

• Career development

• Starting your own business

Self-betterment is the equivalent of Maslow’s self-fulfillment stage. As you formulate your values at this level, ask yourself, “What do I want my life to be like in the future?” Spending your financial resources on education and career development does not guarantee success, but it can increase your odds of achieving your goals. A financial commitment to your education and/or career development can have a larger impact the earlier in your career you make the investment.

There are many different ways to approach post-high school education. If you are fortunate, the unavoidable expenses will be delayed through scholarships, deferred student loans, the military or parental support. It becomes increasingly more difficult to invest in self-betterment as you grow older and get deeper into paying for the bottom of the pyramid. However, it is important to keep in mind that this level has the potential to catapult you more quickly into being able to invest in all levels of the pyramid. Sometimes, you must go slow to go fast.

“Cashualization”

“Cashualization” is my play on self-actualization as it relates to:

• Savings

• Investments

Once your invested cash begins to grow, you will be able to allocate your budget in a more enjoyable way. If self-actualization means achieving your full potential, then cashualization is achieving your full money potential. Arguably, in all other levels of the pyramid, you consume resources. Once you achieve cashualization, you truly begin to build wealth and grow your financial resources. This building of wealth is a tedious process that is essential to achieving financial freedom. Important rules for investing include:

• Establish a spending value system. Understand that when you spend on x, you reduce what you can spend on y, and so on

• Save at least six months of expenses

• Max out your 401(k) contributions

• Contribute to a Roth IRA if eligible

• Be mindful of discretionary income and

spend or save it with intention

In summary, how you spend your money is largely based on your values. The higher up the hierarchy you climb, the more you are able to improve your life, both today and in the future. It is easier to spend with intention once you have a clear understanding of your values.

At Creative Planning, our advisors work with clients every day to help them articulate their priorities and values when it comes to budgeting, saving, spending and investing. We then integrate these values into a customized financial plan that helps each client achieve his or her long-term financial goals. If you’re ready to start planning for your financial future, please contact us.