6 Strategies to Help You Achieve Financial Freedom

For many people, achieving financial independence can seem like an unreachable goal. Financial independence refers to a point of controlling your own finances (rather than being controlled by your finances). It typically means you’re not tied to income from a job or the uncertainty of not knowing how to cover unexpected expenses.

Individuals who have achieved financial independence typically share the following characteristics.

#1 – They have a plan.

A key step to achieving financial independence is having a financial plan in place. A comprehensive financial plan helps put you in control of all aspects of your financial life, allows you to set specific financial goals and helps you implement actionable strategies to achieve your objectives. More than anything, a financial plan clearly highlights your progress toward achieving financial independence and can help you make adjustments to improve your future outcomes.

Financial planning can also help increase your level of confidence, result in more beneficial financial behavior and help ensure your family will be provided for in unexpected circumstances. Ultimately, a financial plan can help you establish a path toward achieving financial freedom.

#2 – They find a way to generate passive income.

For many people, achieving financial independence means no longer needing to exchange their time for money (aka working for employment income). Doing so typically means finding a way to generate passive income. As opposed to employment income, passive income is money earned with little to no ongoing effort. It typically requires an upfront investment in an asset with the potential to generate income over time.

Examples of income-generating investments include:

- Dividend stocks

- CDs

- Bonds and bond funds

- Real estate investment trusts (REITs)

- Private equity investments

- High-yield savings accounts

- Peer-to-peer lending

- Money market funds

- Managed real estate/rental properties

Your wealth manager can help you identify passive income opportunities that may make sense for you based on your personal financial situation and goals for the future.

#3 – They don’t carry high-interest debt.

High-interest debt is a killer of financial independence. By its very definition, debt means your financial priorities are to someone else rather than to yourself. Regardless of whether you carry student loan debt, credit card debt or any other type of debt, the sooner you pay it off, the sooner you’ll be able to achieve financial independence. It’s especially important to pay off high-interest debt as soon as possible, as interest and fees on outstanding debt can quickly spiral out of control if not properly managed.

Two effective strategies for paying off debt include:

- The snowball method – This method involves paying off your smallest debt balance as quickly as possible, then moving on to the next-smallest debt. The benefit of this approach is it can help you gain a sense of accomplishment as you knock out one loan after another. It can also help with your cash flow, as you will have fewer monthly payments each time a debt is paid off.

- The avalanche method – Using this method, you begin paying on whatever loan has the highest interest rate. Once that’s paid off, you move on to the loan with the next-highest interest rate until all loans are paid off. This approach allows you to pick up speed as you go, because each payment saves you more money than the one before.

However, low-interest or 0% interest debt can be a valuable financial tool to help you achieve financial independence. If low-interest or 0% interest debt allows you to leave more funds invested for your future and you’re not utilizing this debt to meet your short-term needs, it can be advantageous to leave your investment funds to grow if they’re likely to outpace the interest on the debt.

#4 – They budget.

The ability to achieve financial freedom requires that you spend less than you earn. A great way to make sure your expenditures don’t exceed your income is by creating (and sticking to!) a budget. A budget allows you to identify exactly where your money is going each month, which, in turn, allows you to be more intentional with your spending and saving.

Start by determining how much money you spend each month. Next, divide your expenditures into discretionary and non-discretionary expenses. Discretionary expenses are costs you choose to take on that aren’t essential for living your life. In other words, they’re wants, not needs. Examples of discretionary expenses include:

- Eating out

- Movie and concert tickets

- Streaming TV subscriptions

- Gifts

- Vacations

Non-discretionary expenses are those you must pay each month in order to live or work, including:

- Rent/mortgage

- Minimum credit card payments

- Car payments

- Insurance

- Utility bills

- Cell phone

It’s also important to factor in discretionary or non-discretionary expenses that aren’t monthly. These may be things you set aside money for each month to fund, or that you may use a bonus or extra income to fund. These expenses can include:

- Property taxes

- Income taxes

- Annual or semi-annual insurance payments

- Annual car registration

- New furniture or electronics

- Vacations

- Christmas gifts

Once you have an idea of your total expenses, compare that amount to the income you bring in each month. Are you spending less than you earn? If not, you may need to find ways to reduce your discretionary spending. Maybe you can cut back from eating out four times a week to one or two times a week. Perhaps you don’t need all your streaming services. Or maybe you choose to take your next vacation closer to home rather than paying for a plane ticket.

It’s important to establish a budget that allows you to pay your fixed expenses and certain valued discretionary expenses while living within your means and making progress toward achieving financial independence.

#5 – They save for emergencies.

If not properly planned for, unexpected expenses can quickly derail your financial security. That’s why an important part of achieving financial independence is knowing you’re in a position to handle unexpected emergencies, such as medical bills, lawsuits, natural disasters, car accidents, etc.

Having adequate emergency savings can help ensure you aren’t forced to sell your investments at inopportune times, thereby locking in losses that can be difficult to recover from. It’s wise to establish a liquid emergency fund to cover at least three to six months of living expenses. For your own peace of mind, you may decide to save even more.

You should work with your wealth manager to help ensure you have appropriate insurance in place. In addition to standard policies, such as medical, homeowners and auto insurance, consider whether the following policies are necessary, based on your personal financial situation:

- Liability insurance

- Umbrella insurance

- Permanent life insurance

#6 – They start saving early in life.

Another common trait among those who have achieved financial independence is that they started saving at a young age. Saving when you’re young allows you to maximize the benefits of compound interest over time, because, as investment gains accumulate, they increase your account balance and begin earning their own interest. Over time, this cycle can create significant savings.

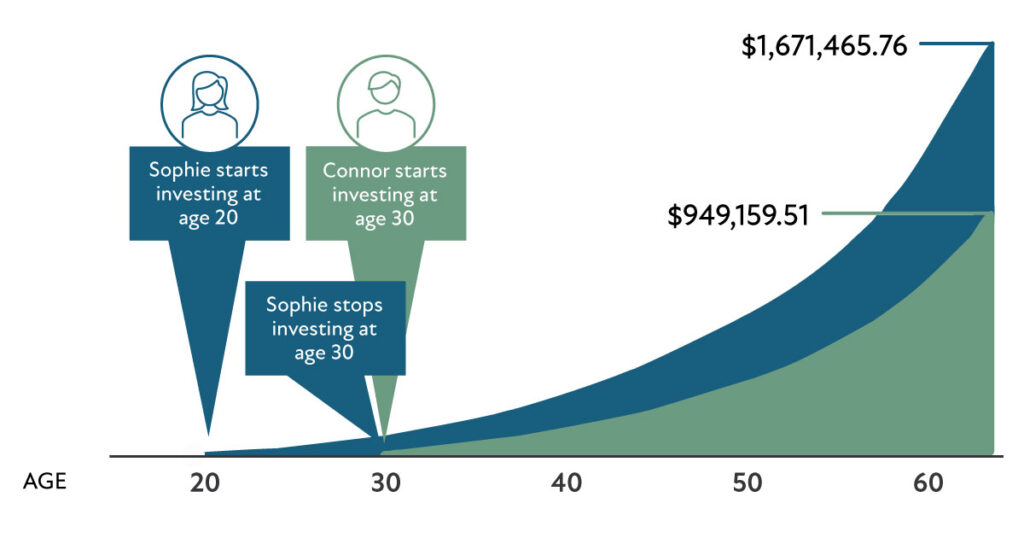

Consider the following chart, which illustrates an example of the impact of compound interest. Notice that both Sophie and Connor contribute $250 per month to their 401ks. However, Sophie begins investing at age 20 and completely stops making contributions at age 30. Connor, on the other hand, waits until age 30 to begin contributing to his 401k but continues saving $250 each month until he reaches age 65.

Assuming a 10% annual return, look at the difference between Sophie and Connor’s account balances at age 65!

The above chart is an example for illustrative purposes only and shows the growth of Sophie and Connor’s retirement contributions over time, as described.

The $30,000 Sophie contributed over 10 years while she was in her 20s has grown to more than $1.6 million, while the $105,000 Connor contributed over 35 years starting in his 30s has only grown to just over $949,000.

Imagine if Sophie had continued contributing from age 30 to 65. She would be well on her way to financial independence!

However, it’s important to remember that it’s never too late to start saving. Any amount you put away today has the opportunity to grow over time.

Could you use some help planning for financial independence? Creative Planning is here for you. Our experienced professionals help clients take charge of their financial lives and make progress toward achieving financial freedom. To learn more, schedule a call with a member of our team. We look forward to getting to know you.