4 Tips to Help Mitigate Sequence of Returns Risk

When people plan for retirement, they often consider savings rates and investments, but there’s another important aspect of retirement planning — timing. Deciding when to retire and how that timing impacts your investments can make a big difference in your long-term financial well-being.

One common risk many soon-to-be retirees fail to consider is sequence of returns risk. This term refers to the risk of being forced to withdraw from your portfolio early in your retirement during a market downturn (i.e., as your investments are losing value).

When you’re forced to sell out of equities at a decreased value, you must sell more shares in order to receive a certain amount of assets, which can cause you to drain your retirement savings more quickly. In addition to selling at a loss, you’re also removing assets from the market that could otherwise have been poised to generate growth as the market recovers. This move can be devastating to those in their early years of retirement, as it may not be possible to recover from such a loss.

On the other hand, if a market downturn occurs later in your retirement, it may not have as big of an impact on your overall savings, as you likely won’t need your assets to last as long.

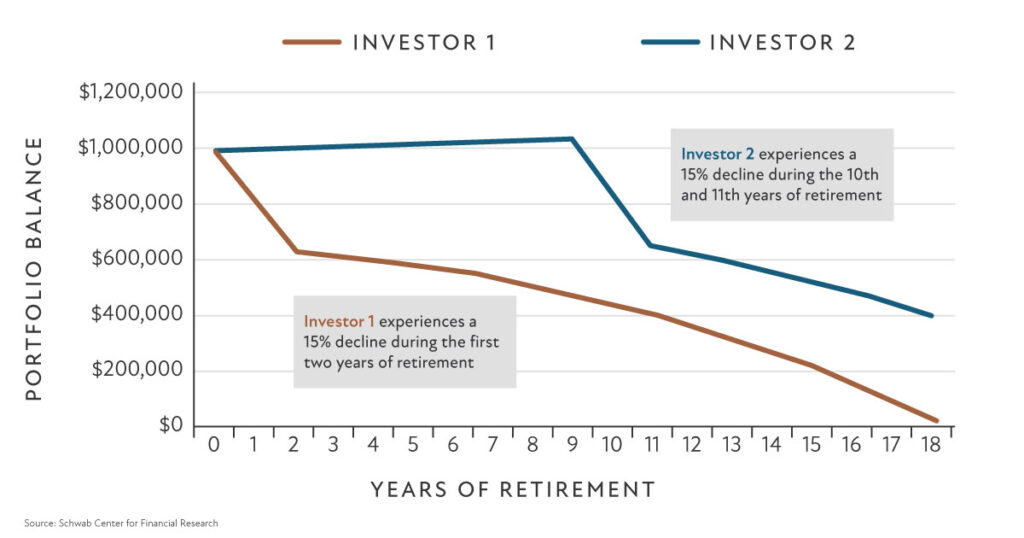

An Example of Sequence of Returns Risk

Consider the following chart, which shows two investors who both enter retirement with $1 million in savings. Both investors take initial withdrawals of $50,000 and increase the withdrawal amount by 2% each year to account for inflation. Both investors also experience a 15% market drop; however, the market drop occurs during the first two years of Investor 1’s retirement and in the 10th and 11th years of Investor 2’s retirement.

As you can see, the market decline has a much more drastic impact on Investor 1’s portfolio, making it virtually impossible for Investor 1 to recover the lost assets during their lifetime.

Strategies for Managing Sequence of Returns Risk

The following strategies can help mitigate sequence of returns risk.

- Maintain a short-term investment account –One of the best ways to manage the risk of a market downturn early in retirement is by maintaining three to five years of living expenses in a short-term, semiliquid investment account. A mix of bond funds typically works well, as it provides capital for opportunistic rebalancing as well as monthly income. Having a short-term allocation to bonds can prevent you from being forced to sell equities at a loss when markets are low.

- Use bond laddering –Taking an allocation to bonds one step further, you may want to consider a bond laddering strategy. This approach involves purchasing a variety of bonds with different, evenly spaced maturity dates that span a specific timeframe. This strategy can help minimize sequence of returns risk by allowing you to generate consistent retirement income (based on the various maturity-date payouts) without the need to sell out of equities at an inopportune time.

For example, you may want to implement a five-year bond laddering strategy by purchasing a bond that matures in one year, one that matures in two years, one that matures in three years, one that matures in four years and one that matures in five years. By doing so, you receive income each year for the next five years that can be used to fund your daily living expenses without the need to worry about stock market volatility. - Diversify –Regardless of the current market environment, it’s always wise to maintain a diversified portfolio. Investing in different types of assets can help spread out your risk, because when one sector or investment type is performing poorly, another investment type that’s performing better can help smooth out volatility within your portfolio. Diversification won’t prevent losses, but it can reduce the risk of being too heavily invested in the worst-performing part of the market.

You can diversify by combining stocks with bonds, large company stocks with small company stocks, U.S. stocks with international stocks, and stocks from different sectors, like technology, financial, energy, healthcare, etc. - Establish (and stick to) a withdrawal strategy –Another way to help mitigate sequence of returns risk is by following a disciplined spend-down strategy. Your wealth manager can help you establish an appropriate strategy that takes into consideration your current financial situation and retirement goals. This strategy should incorporate all potential sources of retirement income, including Social Security.

There are a variety of ways to mitigate sequences of returns risk depending on your particular set of circumstances. At the core of all of these is building a portfolio that is based on your goals and having a process to revisit those goals on a regular basis within the context of the current market environment.

Could you use some help implementing strategies to help mitigate sequence of returns risk? Creative Planning is here for you. Our wealth managers are available to help manage all aspects of your retirement and investment planning with custom strategies specifically designed to help achieve your retirement lifestyle goals. To learn more, schedule a call with a member of our team.