It’s 2025! (The time travel movies from my childhood didn’t even go as far into the future as 2025!) As the clock strikes midnight on another year, New Year’s revelers can toast the positive returns the markets mostly provided in 2024. The clear winner was U.S. large cap stocks, which achieved another year of more than 20% growth — a rare occurrence, as the S&P 500 has only seen this happen four times since 1900. Smaller U.S. companies saw double-digit growth as well, while international market returns were more muted as the U.S. dollar continued to strengthen. (This is a great time to make international travel plans to stretch your dollar further.)

At first glance, it almost seems difficult to fathom these types of returns with the headlines that were facing the markets this past year. While today feels different, when we look at things through an objective long-term lens, we realize times like these occur more often than initially perceived. Even some of the seemingly “unprecedented” events of the prior year with the extra attention bestowed on the presidential election have a precedent. Politics serves no purpose in prudent portfolio management. If you cashed out when Obama became president, that was a terrible investment decision. If you cashed out when Trump first won the election, that too was a terrible idea. (In Trump’s first four years, the markets went up 56%, while in Obama’s tenure, the markets increased by 148%. However, the latter had two full terms, thus reinforcing it’s time in the market that matters … not the president’s political party.) Once upon a time, someone was surely screaming “I can’t have my money invested with the Whig party in control of the White House!” (There were four presidents that were part of the Whig Party in the mid-19th century: William Henry Harrison, John Tyler, Zachary Taylor and Millard Fillmore. According to historical records, none of them wore toupees, so I may be misinterpreting the Whig party’s platform.) Historically speaking, taking your money out of the market is the wrong call 100% of the time over the long term.

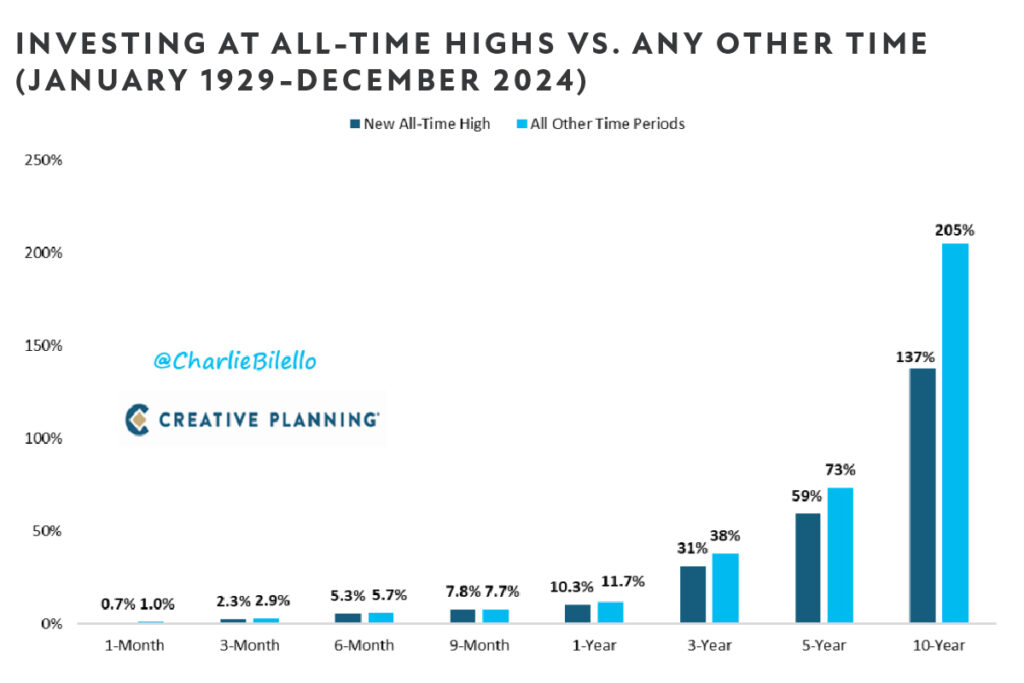

Another, this time apolitical, false narrative would be the argument that you shouldn’t be putting money to work at all-time highs after the recent gains we’ve seen in the markets. As our own graph wizard, Charlie Bilello, noted, all-time highs happen a lot:

(If you’re into graphs, Charlie puts out great stuff weekly. You can check out his videos on Creative Planning’s YouTube channel.)

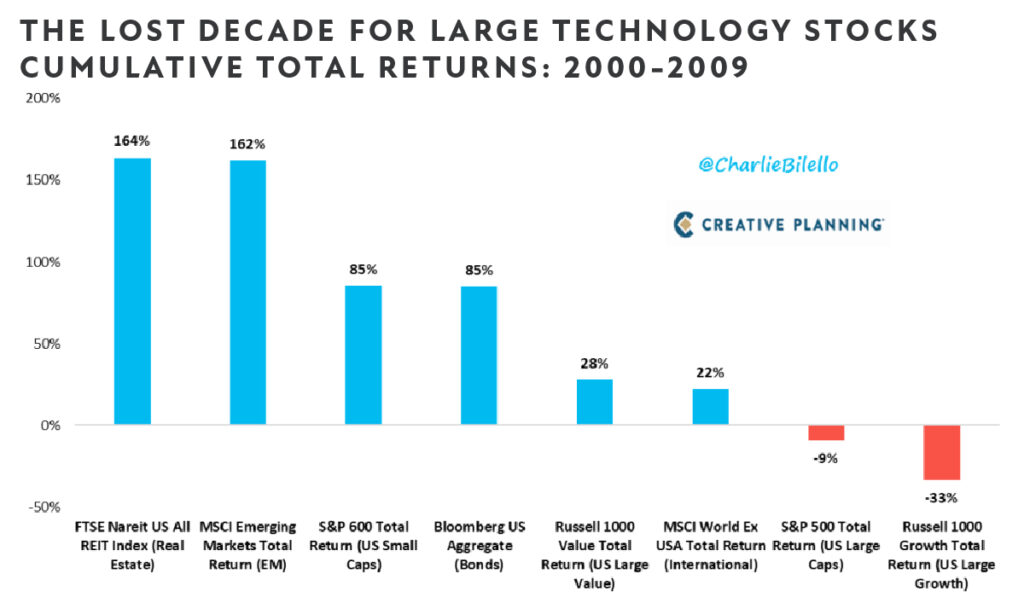

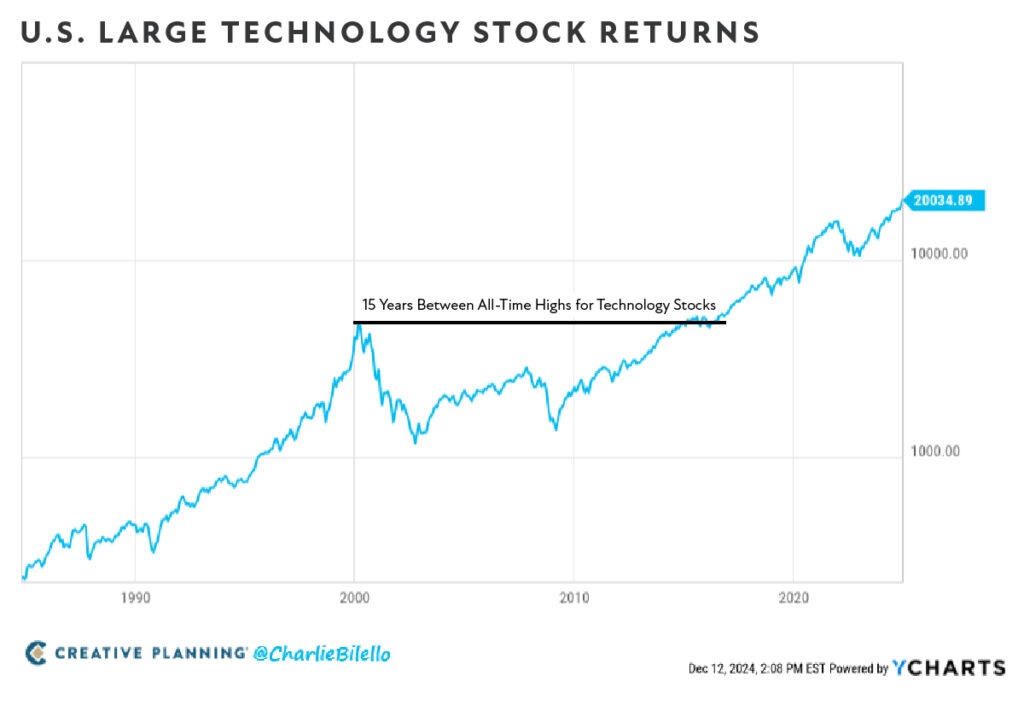

What also happens often (although not nearly as frequently — and that’s very important) are long bouts of no new all-time highs. This is sometimes a hard lesson to follow, especially when the strongest gains are bunched into only a handful of asset classes, like with large domestic technology stocks at present. Zoom out just a little, and for an entire decade, Big Tech names lost a whopping 33% of their value while other investments helped weather the storm. Avoiding these prolonged periods of market stagnation mandates putting more of your eggs in different baskets. As graphed, all those current “drags” on total returns have shown their merit when the tide goes out for hot investments of the moment. Each basket has its own moment in the sun, but this is the key to sustained portfolio positive trendlines. (It was only the turn of the new century when high-flying technology stocks last dominated returns and headlines. At the vanguard of that parade was Cisco, a tech darling and briefly the no. 1 stock in the S&P 500. Well, since then, the S&P 500 is up 800% while Cisco is still nearly 50% below its 2000 high. The point is that by properly indexing public markets, you can benefit from Cisco’s, Exxon’s, Walmart’s, Apple’s, Amazon’s or Nvidia’s moment in the sun without being beholden to them individually.)

It took large tech company stocks 15 years to return to all-time highs, as graphed. A lot changes in 15 years, but you have to keep moving forward. Your portfolio needs to move forward too, and that’s what proper diversification provides.

A reversion to the mean may commence immediately, or it may go on for much longer. We don’t know, and no one else does either. The bull market, in general, may continue — or it may not — but using history as our guide, this bull market has been historically small in both duration and overall returns thus far. (This terminology came from the idea that the bull strikes upward with its horns, while the bear strikes downward with its paws — but we’ve never really liked it, as it denotes that you should jump into bull markets and avoid bear markets. That really just doesn’t work. Be a bison instead. During intense weather, bison turn and face the storm. They’re the only known animals to do so, because heading into the storm shortens its duration.)

Most importantly, whether the bull market continues really shouldn’t matter for long-term investors putting their money to work. The data is overwhelmingly supportive to just get as much of your money working on your behalf as you possibly can. (Albert Einstein called compounding interest the eighth wonder of the world. Like my six-year-old, he wasn’t great at combing his hair but still had many wonderful attributes and nailed this observation perfectly.) Graphed below are future returns if you only invested money immediately following an all-time high versus a day when the markets didn’t eclipse an all-time high. The future returns are very compelling regardless of when dollars go in. Keep contributing to corporate retirement plans, use the account type that’s optimized for your particular needs and circumstances (e.g., Roth vs. traditional) and continue funding the kids’ (or grandkids’) education savings accounts. (Tax-optimized investing is like eating a healthy diet and exercising. On a daily basis, the results are almost immeasurable, but they make all the difference over the long term. Tax-optimized investing can add an additional 60% in after-tax returns over a 20-year period. I’m unfortunately much better at tax optimization than the veggies and working out part, so consider that my New Year’s resolution.)

Whatever makes up your particular circumstances should be the planning-led and active component of decision-making, and, broadly, getting your money invested should be on autopilot as much as possible. (Many tax-optimized decisions need to be made before the end of the calendar year, but others only have to be made before filing taxes. Visit our Insights page to read articles discussing tax-smart decisions. My 13-year-old daughter worked after-care at her school and received W-2 earnings, meaning that we can fund a Roth IRA for her now. If you’re fortunate enough to be in a position to help loved ones, it doesn’t have to end when they leave the nest. That same daughter wants to be a teacher like her grandmas. At her initial wages, she may not be able to contribute enough to receive 100% of the match from her employer’s retirement plan. If instead of giving her money we allow her to adjust her payroll to contribute more to her retirement plan, if the match is 100% then we just doubled the gift we gave her, which is about as close to free money as you can get.)

The trajectory of interest rates, and subsequent weak returns for bonds, reinforces two of the key tenets at the core of Creative Planning’s philosophy. The first, and most important, lesson it reinforces is, “over the long run you’re rewarded more for being an owner than for being a lender,” which systematically tilts our investment recommendations toward owning more stocks versus bonds. Your conservative bucket should be based on your near-term withdrawal needs, not some arbitrary percentage based on age.

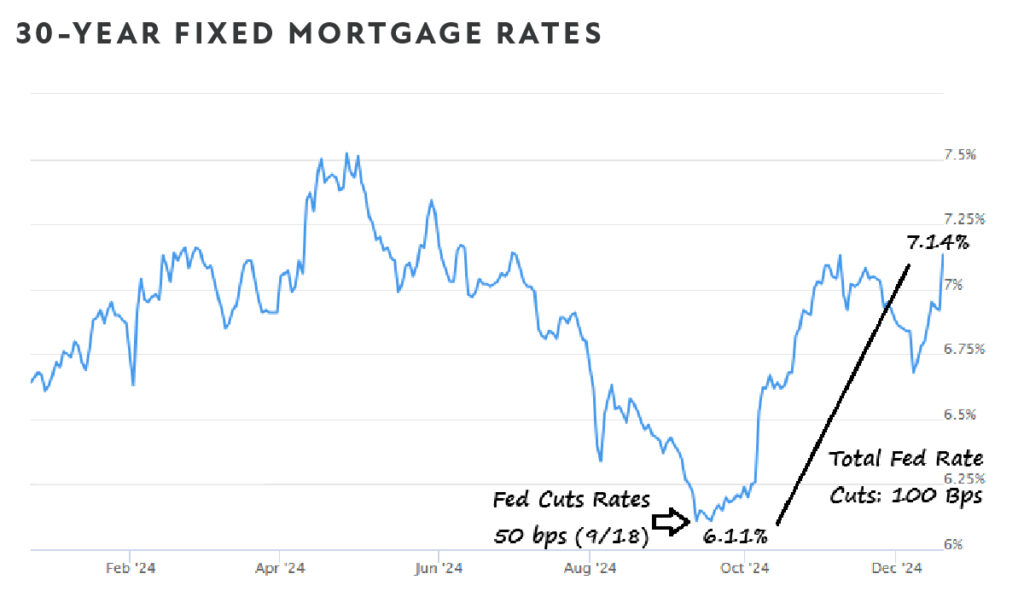

The second lesson reinforced is to avoid short-term market prognostications. In the short run, it’s a pure guess; in the long run, it’s math. Overpaid and overdressed tarot card readers anticipated interest rates dropping precipitously in 2024. (No offense is meant to tarot card readers. Pick up a Barron’s Magazine from January 2008. The “top Wall Street strategist” surveyed said, on average, the market would be up 11% in 2008. It ended up being down 39%, so they only missed by 50%. The same occurred in 2020, when markets were down 35% and the average call was for another 15% decline — over the next 100 days that was only off by 100%. We’re not for a nanosecond saying we foresaw any of these market calamities coming, but that’s the entire point. Nobody could have truly seen them coming.) As graphed, interest rates actually ended the year higher, and mortgage rates spiked after the Federal Reserve began to officially lower interest rates. Don’t be lured into higher rates being offered by fixed income investments, such as CDs or other so-called “low-risk investments.” The highest risk to these strategies is lower long-term returns for a portfolio. They always fail to mention that in the disclaimers of the proprietary products they peddle.

Just as important is avoiding the temptation of believing these good times are here to stay. The price of admission for successful long-term investing is inevitable periods of market downturns and volatility. Yes, we’ve had two strong years in a row, but 2022 was terrible and about one out of every four years (in no sequential order) is terrible too. We can (and should) celebrate the markets cooperating in 2024, but the sound investor celebrates doing the right thing regardless of prevailing market conditions over and over and over again.

Best wishes for a safe and prosperous 2025.