6 Tips to Help Minimize Fees and Maximize Your Retirement Savings

When it comes to saving for retirement, every dollar counts. However, many individuals underestimate the impact excessive fees can have on their retirement savings over time. If not properly managed, high investment fees have the potential to significantly erode the value of your retirement accounts.

The danger of high fees

Investment fees come in various forms, such as expense ratios, sales loads, transaction fees and advisor fees. While some fees are necessary to cover the costs of managing your investments, excessive fees can be a significant drain on your long-term returns.

One of the most significant risks of excess fees is their impact on your ability to accumulate compound interest. Compounding interest has the potential to generate substantial growth in your investment portfolio over time. However, excess fees reduce your overall investment return and the resulting benefit of compound interest over time.

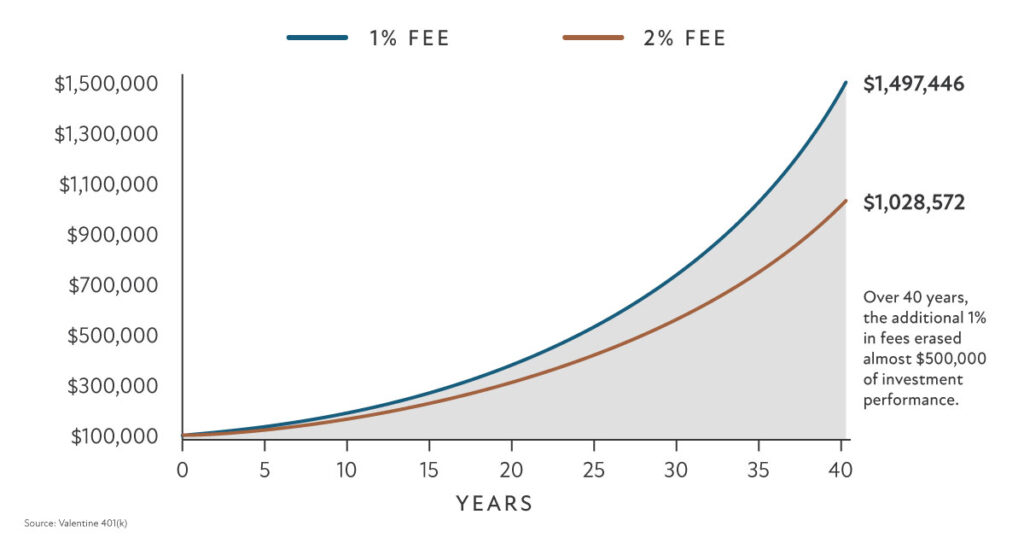

Consider the following example.

As you can see in the chart above, excessive fees have the potential to drastically reduce your retirement savings over time.

Tips to help mitigate the risk of excess fees

The following tips can help mitigate the risk of excessive fees and optimize your investment returns over time.

#1 – Understand and compare fees

Take time to understand exactly what fees you’re paying and what you’re receiving in return. Review investment prospectuses and fee disclosure documents, and compare the fees of various low-cost investment vehicles, such as index funds and exchange-traded funds (ETFs). Make sure the fees you’re paying for a given investment are justified by the returns you’re making.

#2 – Consider expense ratios

Expense ratios refer to the annual cost of owning a mutual fund or ETF. Different funds/ETFs can vary widely in the expense ratios they charge. Look for funds with lower expense ratios. Even a seemingly small reduction in expense ratios can lead to significant savings over time.

#3 – Be aware of sales loads

Sales loads are fees charged when you buy or sell certain mutual funds. Front-end loads are deducted from your initial investment. Back-end loads are assessed when you sell your holdings. Look for no-load or low-load funds to avoid excessive sales charges that can reduce your returns.

#4 – Watch out for transaction fees

Transaction fees refer to charges imposed when buying or selling investments, such as individual stocks and bonds. If you make frequent trades, these fees can add up quickly. Consider implementing a long-term investment allocation that doesn’t require constant trading.

#5 – Regularly review and rebalance

While it’s smart to take a long-term approach when developing your asset allocation, it’s important to periodically review and rebalance your portfolio to help ensure it continues to align with your financial goals and risk tolerance. The rebalancing process can also help you identify and eliminate underperforming funds with high fees to help optimize your returns.

#6 – Work with a fee-based advisor

Fee-based wealth advisors are compensated based on the assets they manage on your behalf. They don’t make commissions on investment product sales, nor do they charge transaction fees. Not only can working with a fee-based advisor help reduce your expenses but it also eliminates potential conflicts of interest. Because the advisor’s fee grows in proportion with your portfolio, he or she is incentivized to maximize your investment returns, which aligns the advisor’s goals with yours.