Tips for Maximizing Your Employer-Sponsored Retirement Plan

If you’re making regular contributions to an employer-sponsored retirement plan, such as a 401k or 403b, congratulations! You’re taking steps toward a more secure financial future. However, even those who participate in a 401k plan may worry they’re not contributing enough to achieve their retirement goals.

Unfortunately, as with so many financial planning challenges, there’s no single guideline to ensure you’re putting enough aside for retirement. Even if you have an idea of the dollar amount you’ll need to comfortably retire, the amount you need to save varies based on a wide range of factors, including when you start investing, your portfolio allocation, market events, lifestyle goals, spending habits, inflation, etc.

A general rule of thumb is to invest 15% of your income in a retirement account, but your exact savings requirements may differ widely from that number. Rather than focusing on a specific contribution percentage, consider implementing the following tips to help maximize your employer-sponsored retirement plan benefits.

#1 – Start contributing as early as possible.

Thanks to the power of compound interest, it’s typically more advantageous to start contributing to a 401k as early as possible, even if you’re only able to commit to a small amount.

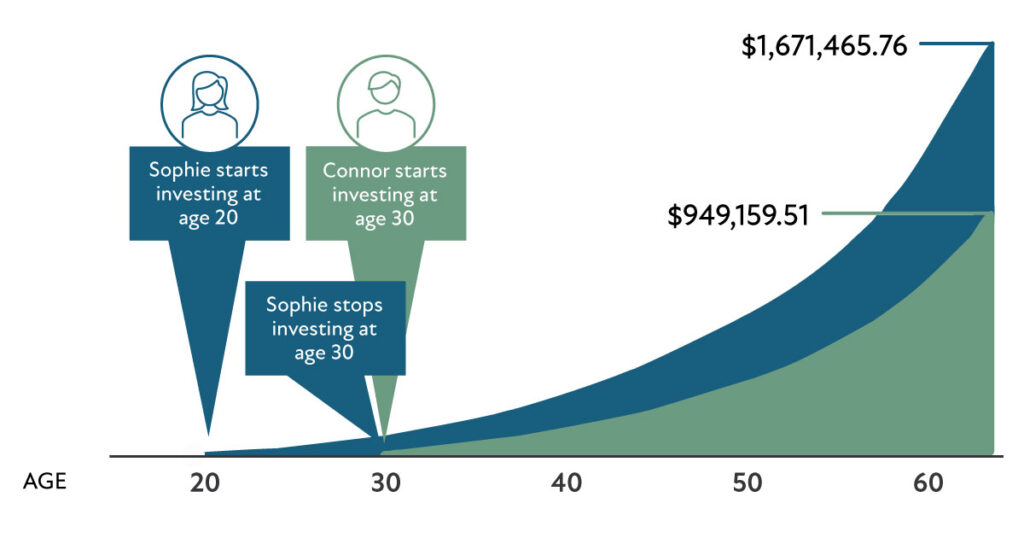

Consider the following chart, which illustrates an example of the impact of compound interest. Notice that both Sophie and Connor contribute $250 per month to their 401ks. However, Sophie begins investing at age 20 and completely stops making contributions at age 30. Connor, on the other hand, waits until age 30 to begin contributing to his 401k but continues saving $250 each month until he reaches age 65.

Assuming a 10% annual return, look at the difference between Sophie and Connor’s account balances at age 65!

The above chart is an example for illustrative purposes only and shows the growth of Sophie’s and Connor’s 401k contributions over time, as described.

The $30,000 Sophie contributed over 10 years while she was in her 20s has grown to more than $1.6 million, while the $105,000 Connor contributed over 35 years starting in his 30s has only grown to $949,000.

If that’s not a compelling reason to start investing as early as possible, I’m not sure what is!

#2 – Aim to maximize your employer match.

If someone offered to give you $3,000 each year with no strings attached, would you take it? Of course you would — you’d be crazy not to! Yet many people pass up retirement savings opportunities each year by not contributing enough to their 401k to receive the full value of their employer’s matching contribution. That’s essentially saying no to “free” money.

For example, let’s say your employer offers a matching contribution of 50% on the first 6% you contribute to your 401k. If you make $100,000 per year and contribute 6% to your plan, your employer will add an additional $3,000 to your account each year.

Think about this as an immediate 50% return on your $6,000 investment. Where else can you find that kind of growth? If you’re not taking full advantage of your matching contribution, you’re likely missing out on a significant opportunity.

#3 – Increase your contributions by 1% to 2% each year.

Once you’re contributing enough to receive your full employer match, consider increasing your retirement plan contributions each year or whenever you receive a raise. Even a 1% to 2% annual increase can have a big impact on your retirement savings over time, and you’re unlikely to even notice the impact on your take-home pay.

#4 – Diversify your contribution types.

Many employer-sponsored retirement plans offer the option of contributing to a traditional (pre-tax) 401k or a Roth (after-tax) 401k.

- Traditional 401k contributions provide the benefit of lowering your taxable income during the year in which they’re made. However, these assets and their earnings are taxed as ordinary income when you withdraw them in retirement.

Once you are retired and reach a certain age, the IRS requires you begin taking required minimum distributions (RMDs) from your pre-tax retirement accounts. These withdrawals are subject to ordinary income tax.

- Roth 401k contributions don’t provide an immediate tax benefit, but assets can be withdrawn without federal income tax as long as you’ve reached age 59 ½ and held the account for at least five years.

In addition, Roth 401k contributions aren’t subject to RMDs, which means your assets can continue growing within the account throughout retirement.

Contributing a portion of your retirement savings to both types of accounts offers a combination of tax benefits, including:

- An opportunity to lower your current taxable income when you’re in a high tax bracket by making pre-tax contributions

- Flexibility and tax planning opportunities in retirement that allow you to draw from accounts with different tax treatments, based on your changing needs, market conditions and tax exposure

Could you use some help optimizing your employer-sponsored retirement plan contributions? Creative Planning is here for you. Our experienced teams take time to get to know you, your current financial situation, your goals for the future and any challenges you may face before offering well-informed, custom solutions to meet your needs. For more information, schedule a call with a member of our team.