Considerations When Deciding Which Charitable Giving Vehicle Makes Sense for Your Family

For many Creative Planning clients, charitable planning is a very important part of their current and future legacy planning considerations. If your financial goals include supporting charitable causes that are important to your family, you may wonder about the best way to help ensure a lasting impact. Two popular charitable giving vehicles include private family foundations and donor-advised funds. But how do you know which option is best for your family? The following considerations can help you decide.

Private family foundation

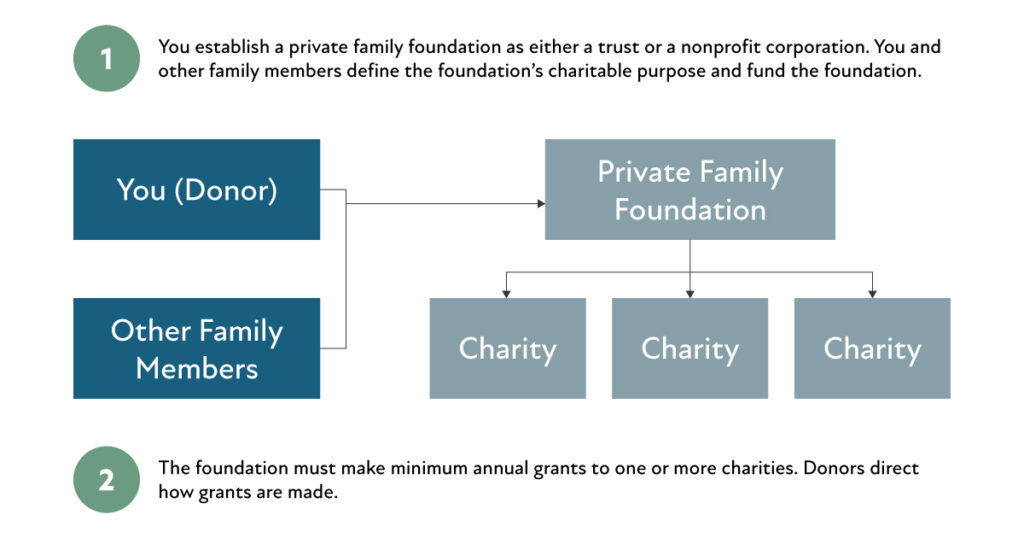

A private family foundation is a charitable organization that’s established and funded by a family in order to fulfill its philanthropic objectives. Most commonly, family foundations are established under IRC section 501(c)(3) as tax-exempt nonprofit organizations. This structure allows the family to make tax-deductible donations and invest those donations with an objective of generating additional income to support the foundation’s designated charities.

Advantages of family foundations

There are several main benefits to donating to a private family foundation, such as:

- Passing down your values to future generations – One of the main benefits to establishing a family foundation is that it gives you the ability to control your charitable impact while allowing family members to have a say in the organizations you support. Once the foundation is established, future generations of family members can continue operating it long after your passing. A family foundation allows you to create a lasting legacy, a shared purpose and a family bond, all while supporting charitable causes that are important to you.

- Control – Another benefit of a family foundation is that it gives you complete control over your donations. You can contribute to public and private charities as well as to individuals facing certain hardships that qualify under IRS regulations. A foundation also allows you to choose your board members and allocate your investments.

- Funding flexibility – A private family foundation can be established using a variety of assets, including cash, real estate, publicly traded stock, private stock, etc. and allows families with less-liquid assets to establish a charitable giving strategy.

- Tax benefits – While one of the main benefits of a family foundation is the ability to support charitable causes that are important to you, an added benefit is that donations offer tax benefits. You can deduct up to 30% of your adjusted gross income (AGI) for donations made with cash, and up to 20% of AGI for non-cash donations.

- Third-party contributions – Foundations are eligible to accept tax-deductible contributions from outside the family, which can enhance the foundation’s impact.

Disadvantages of family foundations

Like with so many financial decisions, there are also downsides to establishing a private family foundation, including:

- Cost – Maintaining a family foundation requires a significant upfront investment to establish the entity and engage with lawyers, accountants and other advisors. Typical family foundations pay between 2% to 5% of total assets per year to cover expenses such as filing fees and legal, accounting and other administrative costs.

- Time commitment – Managing a family foundation requires a significant time commitment. Ongoing, family members must make time to conduct diligence on potential charitable beneficiaries, review grant proposals, oversee investments, manage the efforts of outside professionals and ensure the foundation remains in compliance with all reporting and regulatory requirements.

- Minimum payout requirements – Family foundations are required to distribute a minimum of 5% of assets each year as grants or charitable expenses. Failure to adhere to this payout requirement may result in penalties. This requirement can be a challenge during periods of market volatility if the foundation’s assets have decreased.

- Regulatory requirements – Establishing and maintaining a family foundation requires that you adhere to a wide range of complex rules and regulations. For example, you must establish a legal structure, appoint a board of directors to oversee operations, comply with complex reporting requirements, establish a grantmaking process and ensure adequate oversight of investment decisions.

Donor-advised funds (DAFs)

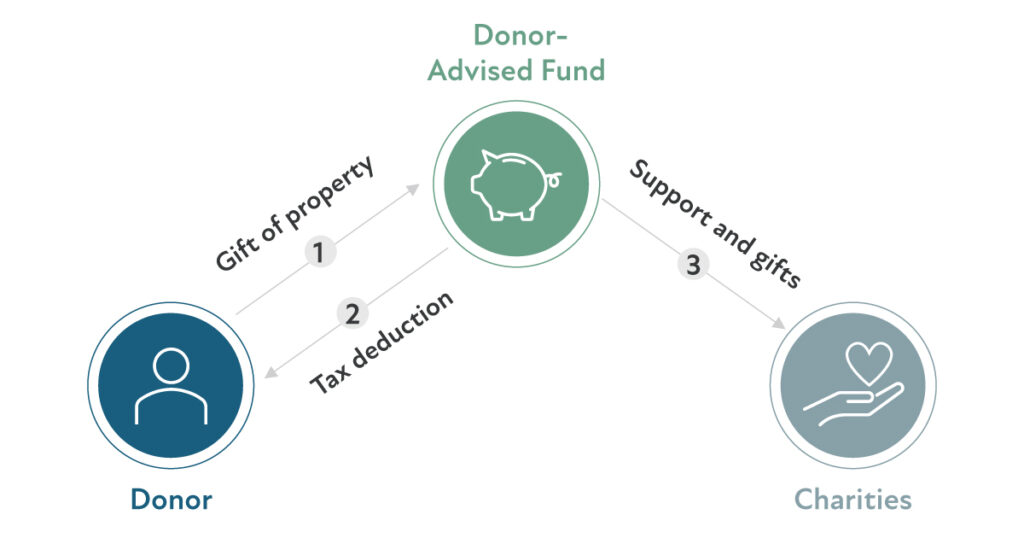

A donor-advised fund (DAF) is a charitable giving vehicle that allows the donor to set aside donations and receive a tax deduction in the current year while having the flexibility to allocate the funds to charities in either the current year or future years.

Advantages of donor-advised funds

There are several reasons why it may make sense for your family to choose a DAF as your charitable giving vehicle:

- Simplicity – The process of establishing a DAF can be much simpler than that of starting a family foundation. The process just includes setting up a new account, similar to opening other types of investment accounts.

- Streamlined recordkeeping – The entity you use for establishing the DAF is responsible for tracking contributions and distributions, as well as for providing simplified tax reporting.

- Tax benefits – Contributing to a DAF allows you to deduct cash donations of up to 60% of your AGI or illiquid donations of up to 30% of your AGI. There are two primary strategies for maximizing your DAF tax benefits based on your filing status (itemized vs. standard).

- Itemized filing – If you file an itemized tax return, you can make large donations during high-income years and receive charitable deduction benefits during the years in which you fall into higher tax brackets. For example, you may decide you’d like to continue donating to charities once you’ve retired. To plan for this, you donate to the DAF during your working years and realize a tax benefit while you are still receiving pay from your job and have a higher income. Once you retire, you can continue donating to charities using the pre-funded DAF assets.

- Standard filing – If you file a standard tax return, it may make sense to stack your charitable donations in order to maximize your tax benefits. For example, say you have a goal of donating $10,000 per year to charities and you file a standard tax return. It may make sense to stack three years’ worth of donations into a single contribution if doing so puts you over the standard deduction threshold. This can allow you to file an itemized deduction during the year in which you make the DAF contribution while still spreading your charitable donations out over three years. The benefit in stacking these donations is that the charity receives the same amount but you have the potential to realize a greater tax benefit.

- Investment control and growth potential – When you contribute funds to a DAF, you’re able to choose how those funds are invested, and any investment growth within the account is exempt from taxes. The ability to determine an asset allocation and access tax-exempt growth offers you an opportunity to significantly increase your charitable giving potential over time.

Disadvantages of donor-advised funds

In addition to the advantages of DAFs, there are also several disadvantages to using a DAF as your primary charitable giving vehicle, including:

- Cost – There are typically administrative fees associated with DAFs, as well as investment management fees that apply to assets held within the account. If the DAF experiences poor investment returns, these fees can gradually erode the value of the account.

- Loss of control – When you donate assets to a DAF, you give up legal control of those assets. While you, as the donor, may advise on the use of those assets, the sponsoring organization may have limitations on how the assets can be distributed. These limitations can be frustrating for donors who prefer to take a more hands-on approach to charitable giving.

- No giving requirements – In contrast to private family foundations, DAFs don’t have distribution requirements. While some donors view this as a pro, it’s not ideal for charitable organizations, as they may struggle to receive donations in a timely manner.

- Inactive accounts – Because assets held in a DAF can remain there indefinitely, these accounts can remain inactive for an extended period of time, making it difficult for charities that have an immediate need for donations.

- Limited giving options – The IRS requires that DAFs donate only to approved charities, which can limit the donor’s donation options.

Family foundation versus DAF: A side-by-side comparison

The following table breaks down the similarities and differences between private family foundations and DAFs.