Key Takeaways

- Succession planning for family businesses is about more than picking an heir — it’s about protecting your wealth, your relationships and the company’s long-term continuity.

- Clear family governance and role definitions help reduce conflict by separating “family issues” from business decisions.

- Legal and financial planning — including your estate plan and buy-sell arrangements — help keep taxes, liquidity and fairness in balance.

- Developing next-generation leaders early and using simple frameworks can make leadership transitions smoother and less stressful.

- Open communication and structured conflict resolution are essential to keeping both the business and family relationships healthy during a transition.

Introduction to Family Business Succession Planning

If you own a family business, you probably see it as much more than a paycheck — it’s your life’s work, your family’s identity and a key part of your legacy. That’s exactly why it can be hard to think about stepping back or handing the reins to someone else, even when you know it’s necessary.

Business succession planning is the process of deciding who will own, manage and lead your company in the future and how that transition will take place over time. For family‑owned enterprises, this process sits at the intersection of business considerations (e.g., cash flow, growth, talent) and family considerations (e.g., fairness, communication, emotions), which makes it both more complex and more important.

Without a plan, your family may be forced to make high‑stakes decisions under time pressure, whether due to a health event, unexpected offer or sudden shift in the market. With a thoughtful plan in place, you can increase the odds of a smooth transition, help preserve family harmony and keep the business strong for future generations.

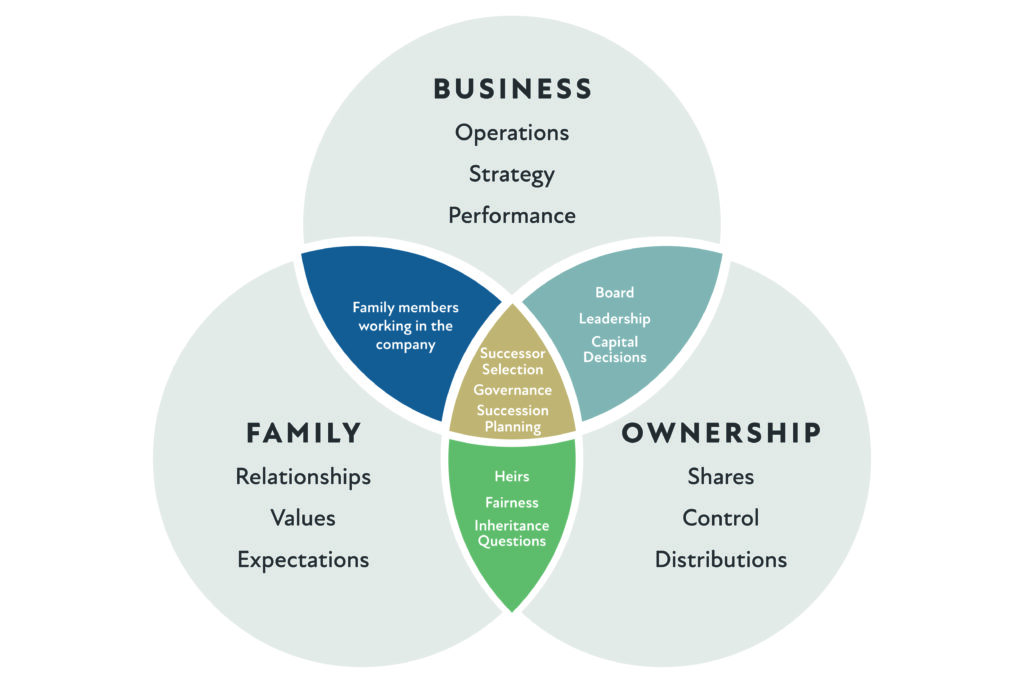

Understanding Family Business Governance and Dynamics

Governance can play a critical role in preserving both family relationships and business continuity across generations. As family businesses grow more complex, establishing clear decision-making structures and communication processes can help reduce conflict, align expectations and support long-term success.

Why governance matters in family businesses

Family business governance is the structure that explains who makes which decisions, how those decisions are made and how family members participate in (or stay out of) the day‑to‑day business. Without a clear framework, long‑standing family dynamics can create confusion or conflict once ownership or leadership begins to shift.

The overlapping roles of family, ownership and business can create both strengths and tensions — governance helps clarify how these circles interact.

Effective governance often includes:

- A family constitution or charter that lays out shared values, a shared vision and expectations around ownership and employment

- A board of directors or advisory board, ideally with at least one independent (non-family) member

- Regular family meetings to discuss high‑level business topics separate from holiday gatherings

These structures make it easier to separate family conversations from business decisions so that you’re not trying to solve both in the same heated moment. For more ideas, see Creative Planning’s overview of family governance.

How family dynamics affect business operations

Because the same people sit around the dinner table and the conference table, family dynamics almost always spill into business operations. Common pressure points include:

- Perceptions of favoritism when one child is tapped as the successor and another isn’t

- Tension between family members who work in the business and those who are owners but not employees

- Generational disagreements over strategy, growth or risk tolerance

If these issues aren’t addressed directly, they can slow down decision‑making, cause talented people to leave and ultimately hurt performance. A strong governance framework, combined with clear communication, helps keep disagreements constructive instead of undermining the business.

Clarifying the role of family members in succession

Succession planning involves three related but distinct questions:

- Who will own the business?

- Who will manage the business?

- Who will lead the business strategically?

In some families, these roles all land with the same person; in others, ownership may be widely held while leadership is concentrated within a smaller group.

Helpful questions include:

- Which family members are genuinely interested in leading the business?

- Who has, or could realistically develop, the skills and temperament needed?

- How will you treat family members who aren’t active in the business but will inherit ownership or receive financial benefits?

Documenting the answers and aligning them with your governance and estate planning documents can help everyone understand the “why” behind your decisions, even if they don’t match every family member’s initial expectations.

Legal and Financial Considerations in Succession Planning

A successful succession plan requires more than identifying who will take over the business. Owners also need to evaluate the legal, tax, financial and estate planning considerations that can affect how smoothly ownership and leadership transition from one generation to the next.

Core legal building blocks

Your succession planning should work hand in hand with your legal documents and overall estate plan. Key areas to review with a qualified attorney include:

- Entity structure – Whether your current structure (e.g., LLC, S corporation, C corporation, partnership) still fits your goals and potential exit paths

- Shareholder or buy‑sell agreements – How ownership changes will be handled in the event of retirement, disability, death or disagreement, including valuation and funding

- Governance documents – Bylaws, operating agreements and any family constitutional documents

- Employment and incentive agreements – Noncompete and confidentiality provisions, along with bonus or equity programs for key employees

Estate planning for family businesses is particularly important because many owners have a large portion of their net worth tied up in the company. Tools like trusts, family limited partnerships, and recapitalization into voting and non‑voting shares can help manage estate and gift taxes while still giving you the control you need today.

Financial strategies to help support a smooth transition

On the financial side, the plan should sustain the business, meet your personal financial needs and treat family members fairly. Practical steps may include:

- Getting a business valuation to understand what the company is worth now and what drives its value

- Designing a buyout structure (such as an installment sale, management buyout or ESOP) that provides liquidity without overburdening the business

- Using life insurance strategically to help fund buyouts or provide liquidity for estate taxes

- Building a comprehensive personal financial plan so that you know how much you’ll need from the business to retire comfortably

Creative Planning Advisor Insight

“The most effective family business succession plans don’t treat legal, tax and investment decisions as separate projects. We look at the owner’s business and personal balance sheets to ensure the buyout structure, estate plan and portfolio all support the same long‑term goals.” – Michelle Yates, CFP®, CDFA®, ChFC®, BFA, CPRS®, Private Wealth Manager

Because succession planning touches both your business and personal balance sheets, it’s helpful to work with advisors who can see the full picture, including tax, investment and estate implications. Your advisors can also help you prioritize different business succession planning paths based on your goals and timeline.

Leadership Transition and Next‑Gen Development

Preparing the next generation to lead a family business often requires years of planning, communication and hands-on development. A thoughtful transition process can help successors build credibility, strengthen leadership skills and create continuity for employees, customers and family members alike.

Managing the leadership transition over time

Leadership transitions usually work best when they’re gradual and intentional. A practical transition plan might:

- Set a target range for your own shift from day‑to‑day leadership into a chair, mentor or advisory role

- Outline clear milestones where the successor takes on more responsibility (for example, first a division, then multiple functions, then overall P&L)

- Introduce successors to key stakeholders — such as lenders, major customers and vendors — well before you step back

In some situations, it may make sense to bring in a nonfamily executive for a period of time, especially if your chosen successor needs more seasoning or if family members are still working out their long‑term roles.

Preparing next‑generation leaders

Next‑gen leaders typically benefit from a blend of education, experience and ongoing mentoring. Consider:

- Rotational assignments across operations, finance, sales and HR so that potential successors understand how the business works as a whole

- Requiring outside work experience before joining the family business full time to build credibility and perspective

- Encouraging formal education, such as MBA or executive programs focused on leadership, strategy or family business management

Creative Planning Advisor Insight

“The strongest transitions we see are the ones where future leaders are given time, structure and honest feedback. You’re not just handing over a title — you’re helping the next generation grow into the responsibility of leading both the business and the family.” – Michelle Yates, CFP®, CDFA®, ChFC®, BFA, CPRS®, Private Wealth Manager

You can also benefit from taking a broader view of how you’re planning and growing your business with the end in mind so that daily decisions support your long‑term transition goals.

The role of mentorship

Mentorship can make the difference between a successor who simply inherits a title and one who really grows into leadership. Effective mentors:

- Offer candid feedback in a supportive way

- Help connect day‑to‑day decisions to the company’s long‑term strategy and values

- Encourage successors to respect the business’s history while also innovating for the future

Many families find it helpful for next‑gen leaders to have mentors both inside and outside the business, such as experienced non-family executives, peer groups or external coaches.

Tools and Frameworks for Effective Succession Planning

Even in a closely held family business, the right tools and frameworks can make succession planning more organized and less overwhelming. You don’t have to adopt complex software, but you do need a simple system that keeps everyone on the same page.

On the practical side, many families rely on:

- Basic succession planning tools, such as spreadsheets or checklists, to track key roles, potential successors and development plans

- HR or performance‑management systems that document responsibilities and help you spot gaps in your leadership bench

- Simple financial models that show how different transition timelines or buyout structures might affect cash flow and taxes

If your business is larger or more complex, dedicated business succession planning software can help you map critical positions, identify backups and monitor progress over time. Some families also find it useful to apply leadership transition frameworks that break the process into stages — for example, assessing the current state, designing the plan, implementing the plan and reviewing the plan regularly — so that they always know what comes next.

Communication and Conflict Resolution in Family Business Transitions

Open communication can help families navigate succession decisions more thoughtfully and reduce the risk of misunderstandings or long-standing conflict. Establishing clear expectations and consistent communication practices early can make difficult conversations more productive over time.

Why communication is essential

Even the most technically sound plan can fail if family members don’t understand it or feel blindsided by it. That’s why ongoing communication is a central best practice in succession planning. Helpful habits include:

- Scheduling regular family meetings specifically to discuss business topics, succession progress and expectations

- Sharing written summaries of key decisions so that no one is relying on memory alone

- Creating safe spaces for younger family members to ask questions and share concerns without fear of overstepping

For more on this theme, see why communicating with heirs is so important for business owners.

Handling conflict constructively

Disagreements about roles, compensation and strategy are common in any business and can be especially intense when family is involved. To keep conflict constructive:

- Agree in advance on how disputes will be resolved, such as through a family council vote, board decision or third‑party mediation

- Focus on shared goals, such as protecting the business, preserving family harmony and honoring the founder’s legacy

- Bring in neutral advisors, such as family business consultants or facilitators, when conversations become too emotionally charged

A well‑designed governance model, combined with clear communication channels, can prevent many conflicts from escalating and help the family get back to running the business.

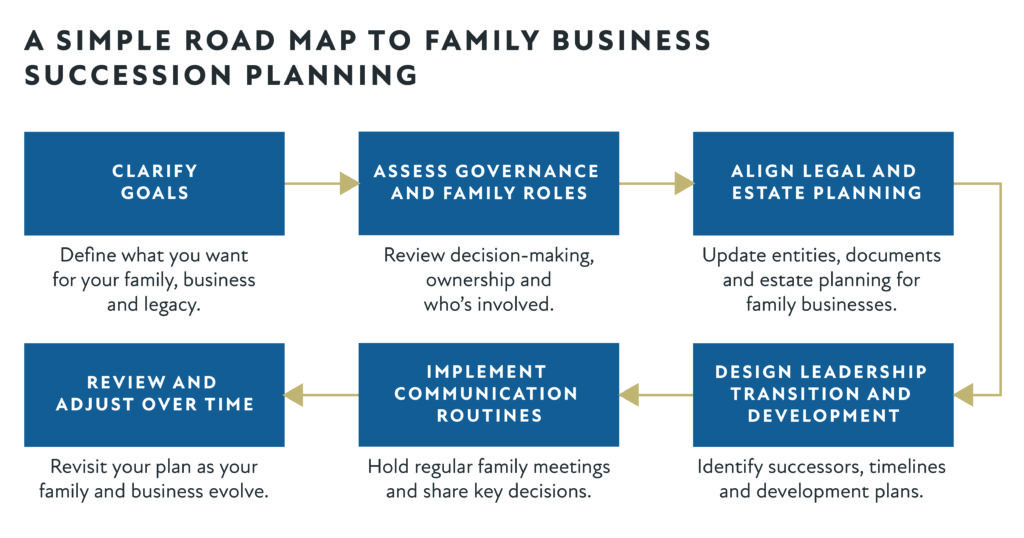

A simple road map to family business succession planning, from clarifying goals to reviewing and adjusting your plan over time.

Putting Your Family Business Succession Plan Into Action

If you feel behind on succession planning, you’re not alone — many owners delay these conversations because they’re complex and emotional. The good news is that you don’t have to do everything at once, and you don’t have to do it alone.

Here are some practical next steps:

- Clarify your personal goals for your retirement, family and business.

- Take stock of your current legal, financial and governance documents to see what’s already in place.

- Identify potential successors and begin honest conversations about interest, readiness and development needs.

- Start formalizing governance structures and communication routines, even if they’re simple at first.

- Work with experienced advisors who understand family businesses, taxes, estate planning and investments so that each piece of your plan fits together.

At Creative Planning, we help family business owners design and implement comprehensive succession strategies that align with their goals, values and long‑term vision. If you’re ready to begin building or refining your own succession plan, our team is here to support you every step of the way.