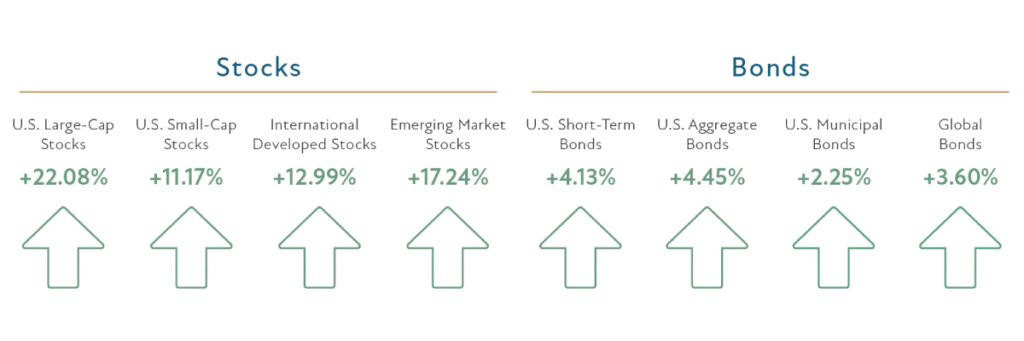

Year-to-Date 2024 Returns (as of 9/30/2024)

As we’ve entered fall and the leaves begin to drop, we can feel fortunate they seem to be the only thing falling as we crest the three-quarters mark of 2024. For stocks, both domestic and international markets have climbed as underlying economic fundamentals remain robust. For boring old bonds, tailwinds from the Federal Reserve lowering interest rates for the first time since 2020 have driven total returns higher. We’re delighted that things have trended so positively, but just like the uncertainty of fall weather, one must be ready for the uncertainty of market conditions that lie ahead. Achy knees may help predict weather changes but are just as useless at predicting market futures as the more sophisticated, yet equally useless, Wall Street prognostications.

Did anyone see this coming? After the easiest analysis of our lives, the answer is 0.0% saw it coming as the future forever remains unwritten. Luckily, (and that’s all it is – just luck or lack of luck) none of the people who were paid to pretend they can predict the future stumbled into success. This presents a convenient opportunity for us to reinforce a key tenet of successful long-term investing. The stock market is now 18% higher than the average Wall Street strategist anticipated for 2024, and it’s nearly 7% higher than the most optimistic forecast of the bunch. The same thing happened with bonds. The “guessers” said interest rates would be reduced seven times in 2024, but so far, it’s only happened once. This provides a stark reminder that if someone tells you what is going to happen in the markets over the next year, it actually tells you nothing about what’s going to happen (because there’s no crystal ball when it comes to the markets), however it tells you absolutely everything you need to know about the person providing the information. Choose to seek guidance from those who can help with your particular needs and circumstances, not those who are good at telling stories about the future. Investing in a Roth 401(k) instead of a traditional IRA — that’s a strategy, not a story. Setting up education accounts for your kids and grandkids while reaping the tax benefits at the same time — that’s a strategy, not a story.

This year has also reinforced the need to be unemotional while making investment decisions. As graphed below, we’ve had two separate downturns in 2024 that, in the moment, felt painful, but will absolutely be forgotten with time. The only catastrophic decision would have been to listen to TV talking heads and sell due to panic. Allowing fear to influence your investment decision-making, rather than following prudent investment fundamentals is a failed strategy nearly all of the time. Long-term investors who remained calm and stayed the course fared just fine. And those who used these momentary bouts of volatility to contribute to their investments (like bi-weekly 401(k)-type contributions), tax-loss harvest (to drive better after-tax returns) or put that extra money on the sidelines to work (cash underperforms stocks 100% of the time over a 20+ year period), were rewarded. Do you know who is not rewarded? Traders. The near 10% recent decline was driven by stock traders getting punished because market winds changed and what they perceived as a free lunch dealing with Japanese currency and interest rates disintegrated. Investors are completely fine. Traders, as nearly always, are punished.

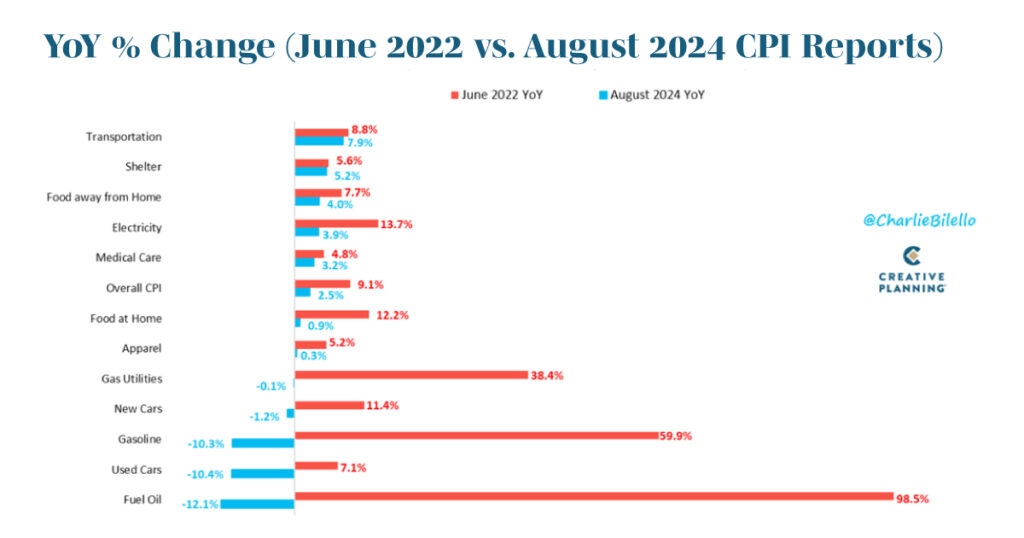

For bonds, returns have also been positive. The Federal Reserve, like most central banks across the globe, has begun lowering interest rates. Japan is the only country amongst the largest economies around the globe that is continuing to raise interest rates; however, they are dealing with uniquely localized issues (the demographics are so unbalanced in Japan they sell more adult diapers than children’s diapers!) As shown in this graph, inflation has been declining across the board (or rising less rapidly), allowing the Federal Reserve to begin lowering interest rates.

This is unequivocally a good thing for most businesses (lower interest payments on loans so cash can be more effectively deployed elsewhere) and all households carrying revolving lines of credit (i.e., credit card debt.) For individuals this is a great time to make sure you’re optimizing your unique financial situation. Review any interest rates you’re paying to make sure you’re taking advantage of lower trending rates.

Okay, if you’ve read this far, thank you. But now, and only now, will we comment on the impending every-four-year popularity contest. Why save it for the end? Because other elements like tax-loss harvesting, investing in the right type of accounts and prudent financial planning are so much more important and so much more within your control compared to election outcomes. Yet it always feels different.

Every four years it feels like the stakes are exceptionally high, or even higher than the previous contest, but the data just doesn’t support that. An astounding and shocking 15% of Presidents has been shot1; not a rounding error percentage. You only have to go back to 1968 to remember the last time a sitting president (Lyndon B. Johnson) refused their party’s nomination; and the markets went up 15% from there through the end of the year. For better or worse, when someone says “this time is different” they are so very rarely accurate.

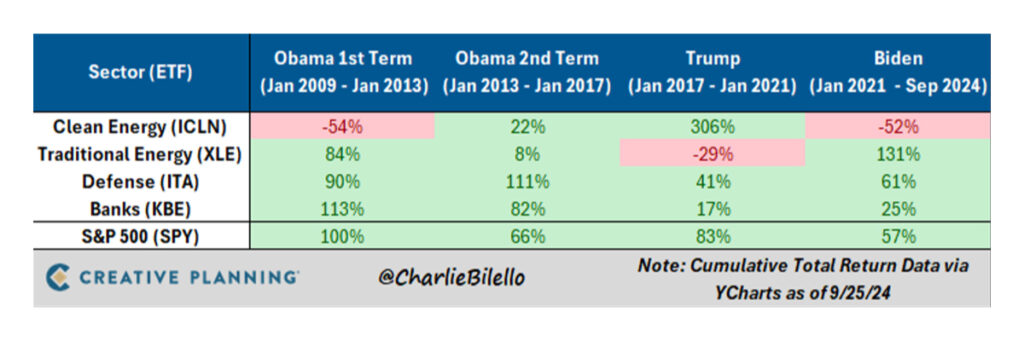

You can turn on any news channel or look at any financial website and see our point reinforced. Over the long-run, markets are not red or blue; they’re green. Continuing to invest, regardless of which political party is in control, is a well-trodden path. But you’ll see many of these news stations or websites will still have articles or commentaries such as “this sector will benefit from a renewed Trump administration” or “that sector will benefit from a Harris administration” and all will be empirically wrong. As shown in this table, we broke down the two four-year periods of Obama’s administration, the four years of Trump’s administration and Biden’s administration so far showing how different sectors of the market performed. If you polled one hundred people, do you think any of them would say clean energy performed dramatically better under Trump while traditional energy performed the same under Obama and Biden?

The point is this — the political rhetoric just doesn’t sync up with the data. The markets and economy are far larger than any one political party or candidate can influence. We’ve always said fear and greed are the well-known twin pillars of poor decision-making when it comes to the markets, but during this election season you can add a pillar for politics to make it a terrible trifecta.

The world is a complicated place; it always has been and probably always will be. The remarkable thing is that we always find a way forward. The exact same tenets hold true for the economy and markets. Over the long run, a well-diversified investment strategy and prudent financial planning almost always win. We’re happy to report the markets are currently cooperating, but that can change just as quickly as the fall colors. Understanding and appropriately participating in the markets, while knowing this is how the seasons ebb and flow, allows for a much more enjoyable and vibrant experience.