The big blue chip stocks in the Standard & Poor’s 500-index were on a roll, posting gains year after year.

Meanwhile, foreign markets—both developed and emerging—were struggling, U.S. small-company stocks were laggards and bonds got no respect. Some of my Wall Street Journal readers even took to parroting a new mantra: “All you need is the S&P.”

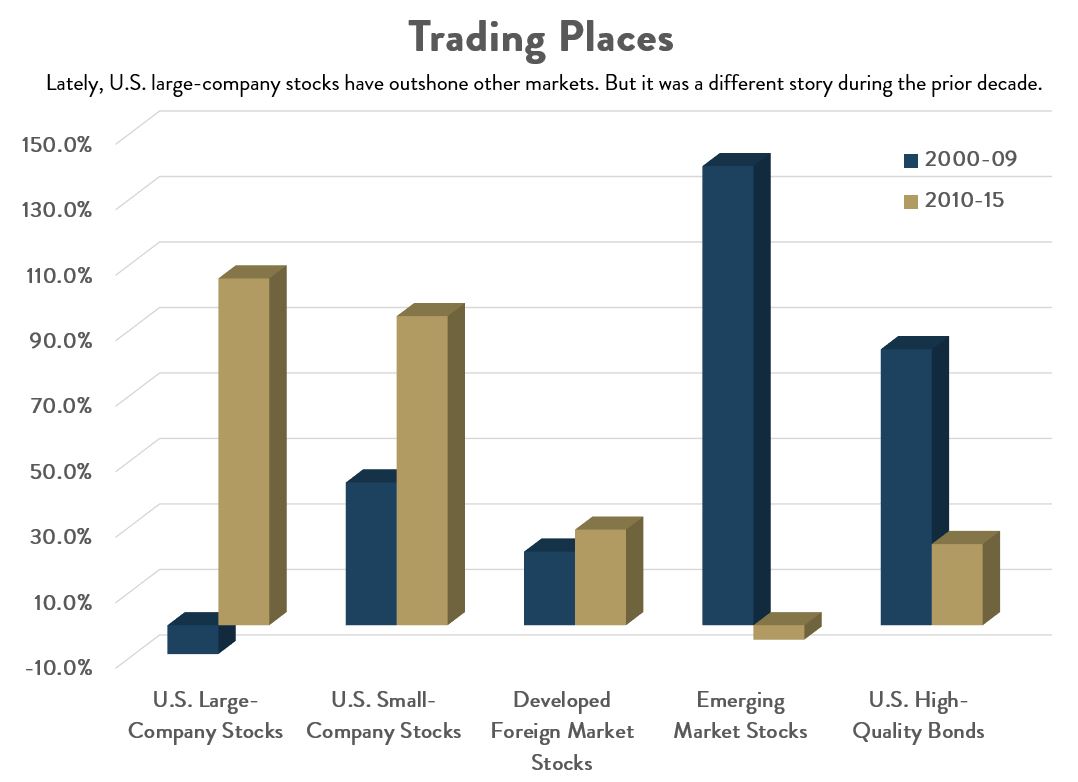

Sound like the past few years? It does—but it’s actually the story of the late 1990s. In the run up to the March 2000 market peak, the S&P 500 posted an unprecedented five consecutive years of 20%-plus gains. Investors poured money into S&P 500-index funds, and some claimed it was the only investment they needed to own. But these investors paid dearly for their lack of diversification: The brutal bear market that began in March 2000 saw the S&P 500 shed a staggering 49%. Indeed, over the decade ending 2009, the S&P 500 stocks trailed every major asset class, as you can see from the accompanying chart.

I’m not predicting another vicious bear market. In fact, when it comes to figuring out what will happen next in the financial markets, Wall Street strategists have a track record that puts them a few notches below weather forecasters and about on par with astrologers.

So what’s the rational strategy in such an uncertain financial world? We should spread our investment dollars widely, thereby bolstering our chances of earning decent gains over time. To be sure, at some point, each component of a globally diversified portfolio will suffer a rough patch. But it’s highly unlikely that every part of the portfolio will suffer at the same time. Result? We should enjoy smoother short-term performance—and healthy long-run returns.

Yet, even if it’s rational to invest as though markets are unpredictable, we instinctively resist this notion. It’s comforting to own investments that have lately performed well, and it’s doubly comforting when it’s the S&P 500, which includes big, well-known companies like Apple, General Electric and Johnson & Johnson. We buy their products. We might know some of their employees. They may have offices near where we live.

Source: Orion Advisory Services. Figures shown are cumulative total returns for the S&P 500 (U.S. large-company stocks), Russell 2000 (U.S. small-company stocks), MSCI Europe, Australasia and Far East (developed foreign markets), MSCI Emerging Markets (emerging stock markets) and Barclays Intermediate U.S. Aggregate (U.S. high-quality bonds).

By contrast, foreign stocks seem so, well, foreign, plus they come loaded with question marks. Will Japan ever escape deflation? Can Europe solve its economic problems? Will emerging markets ever return to their days of heady growth?

To make matters worse, when we ponder our portfolio’s performance, we’ll often use the S&P 500 as our mental yardstick. Lately, it’s been the global markets’ star performer. The S&P 500 has posted gains for seven consecutive calendar years. Other than real estate investment trusts, no other major market sector can make that claim, not even bonds. In short, the S&P 500 today offers everything we want in an investment: a sense of security—and superior returns. The temptation: Ditch all those strange funds that own unfamiliar companies and load up on the good ol’ S&P.

But a year or two from now, will that seem like a wise decision? As they say on Wall Street, “You pay a high price for a cheery consensus.” (Of course, they also spout a lot of nonsense on Wall Street, so you need to be selective in the clichés you quote.) If an investment is popular, there’s a risk that future performance will be mediocre or worse.

Make no mistake: Today, U.S. large-company stocks are exceedingly popular, at least judging by valuations. Among the world’s major developed economies, the U.S. may be enjoying the most robust growth, but it also sports the richest stock market valuations, based on metrics like dividend yield and cyclically-adjusted price-earnings ratios. Europe may be struggling economically, but its stocks are also trading at valuations that are roughly 40% lower than those found in the U.S.

That doesn’t mean U.S. stocks are guaranteed to perform poorly. A 2012 Vanguard Group study found that a market’s current price-earnings multiple only explained 40% of the variation in performance over the next 10 years.

In other words, it’s entirely possible that U.S. large-company stocks will fare just fine over the next decade, which is why you want them in your portfolio. But it’s also entirely possible that performance will disappoint, which is why you want to take the path of humility and build a globally diversified portfolio of stocks and bonds. As I like to tell people, the meek may not inherit the earth. But they are far more likely to retire in comfort.