Your Guide to Investing From the Sideline

One of the most frequent questions we get from our clients is, “What should I do with my excess cash?”

Sometimes cash has built up due to year-end bonuses or, as we just experienced, from a decrease in lifestyle spending because of a global pandemic. Given the volatility we’ve experienced over the first half of 2022, it’s easy to feel hesitant about putting excess cash to work in stocks. The bond market isn’t too inspiring right now, either, given the threat of rising interest rates as the economy recovers and the Federal Reserve ushers in a hawkish monetary policy regime.

So, how do we answer this question?

Depending on your unique circumstances, consider investing this excess cash in your long-term strategic asset allocation targets. When making decisions about your investment strategy, you want to make sure your risk tolerance is always first and foremost.

Part of knowing your risk tolerance is understanding what creates risk and how this affects both you (emotionally) and your investment portfolio (statistically). One of the most common risk-averse rationales is, “If I’m not in the market, then it won’t affect my portfolio — it’s safer to have to cash in the bank.” This could be a smart option if liquidity is required within the next 3-12 months.

But if your financial situation doesn’t require immediate liquidity, cash in the bank probably isn’t the best strategy to grow your wealth. Let’s break down this stigma and analyze what happens to cash when it’s sitting in the bank as well as the opportunity cost of sheltering cash from market growth.

The COVID-19 pandemic-induced market crash of March 2020 was one of the sharpest drops in market capitalization since 2008. Later in 2020, the very same year, the S&P 500 also hit record all-time highs. Most investors who stuck with their equity allocation (or added to equities) during the recession and rebound of the stock market in 2020 ultimately benefitted.

Let Your Money Work for You!

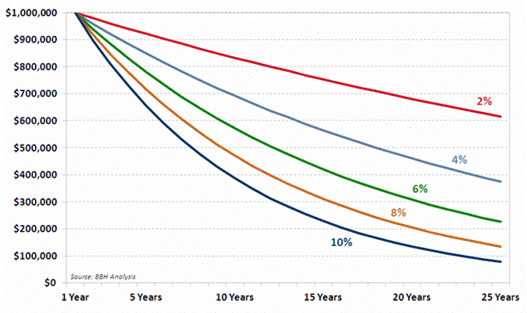

The adage “let your money work for you” became timeless for a reason. Cash over the intermediate and long term carries a massive opportunity cost and puts you at a high risk of losing purchasing power over time, especially with cash yields near zero percent. The #1 reason to invest is to outpace inflation and grow your purchasing power over time. You can see in the following chart how quickly inflation can erode your purchasing power.

Purchasing Power of $1,000,000 (At Various Rates of Inflation)

Source: BBH Analysis. Scott Clemons and Michael Kim, The Eight Principals of Value Investing. https://www.advisorperspectives.com/articles/2013/10/01/the-eight-principles-of-value-investing

Cash rarely outperforms other asset classes because it doesn’t generate any income, especially in a low interest rate environment. Typically, long-term growth is derived from stocks, but bonds have also steadily outpaced inflation historically. Additionally, bonds also offer diversification benefits. Historically, during periods of stock market volatility, investors rush to safety and bond prices appreciate. We haven’t seen that thus far in 2022 but do expect high-quality bonds to provide ballast during future bear market declines where investors flee to safety.

Stocks have outperformed cash consistently over time. Going back to 1928, the odds of beating the S&P 500 while sitting in cash were 30.6% over rolling one-year periods. The longer you sit in cash, the lower your odds of beating the market. An investor in the S&P 500 has beaten cash in every 25-year period, including those who bought at the peak in 1929.

Expect Volatility, Embrace Volatility

“I think I’ll sit in cash until after the volatility blows over, then I’ll get back in.”

There is also a measurable cost to market timing and trying to avoid the big dips — as long-term investors in stocks, it’s smart to first expect volatility and then (at least try to) embrace that volatility.

The kicker in this is that volatility tends to cluster — the best days in the market are often concentrated around the worst days in the market. It’s advantageous to you in the long term to not be out of the market on those best days. The following chart is telling. From 1997 to 2016, a period that includes two large bear markets, if an investor missed the best 30 days, their returns would be wiped out. If an investor held through this volatile period, their returns would be just under 8%, annualized.

During bear markets, we tend to opportunistically rebalance — selling assets that have held up relatively well and buying stocks on sale.

Source: Morningstar. “Principles of Investing.” Stocks = Ibbotson Large Company Stock Index. Past performance is no guarantee of future results. This is for illustrative purposes only and not indicative of any investment. An investment cannot be made directly in an index. 1/1/1997-12/31/2016.

Protection Against Correction = Safety in Numbers

If only investing were about the data or numbers! We’re fully aware feelings and emotions play an important role in decision-making related to our money and investments.

If you’re hesitant to enter the market all at once, strategies such as dollar-cost averaging can help reduce the impact of market volatility by spreading out purchases over time to help ensure you’re buying at multiple market price points. A qualified wealth advisor can help take the emotion out of investing by constructing a long-term portfolio allocation that is in line with your risk tolerance and works in conjunction with your overall financial plan.

Additionally, Creative Planning has a dedicated options strategy team that can use cash-secured put options to generate a yield while implementing a disciplined dollar-cost averaging strategy.

Focus on Time in the Market, Not Timing the Market

We’ve worked with clients for more than 30 years, and we’ve learned one common lesson: successful investors accept risk and stick with their strategies through both good and bad times. The most important time to be self-aware is during market turbulence — when you feel a strong desire to abandon your asset allocation.

So, why don’t we wait for the next 10% pullback and then invest in stocks?

The following chart shows returns for U.S. large cap stocks from 1998 to 2018. This period contains two of the largest declines in stock market history: the dot-com bubble burst (early 2000s recession) and the Great Financial Crisis of 2008. Despite those massive economic shocks, being invested over the entire 20 years would still give you a significant return over sitting in cash.

Source: YCharts, InflationData.com. U.S. Large Cap Index = S&P 500. Data as of 01/01/1998-12/31/2018.

Summary

We believe it’s always the right time to be invested at your long-term strategic allocation targets based on your unique financial plan and goals. Additionally, the decline in stocks over the first half of the year has provided an opportunity for investors to buy stocks on sale. If you don’t plan on using your newfound or built-up cash in the near term, we can work with you to build a dollar-cost averaging program, in conjunction with your current portfolio and overall financial plan, to allow that money to start working for you. This could allow you to benefit from the magic of compounding returns — sometimes called the eighth wonder of the world

For help dollar-cost averaging, or for assistance with any other financial matter, schedule a call with a member of our team.