Would you like to buy an investment that’s lost money in three of the past five calendar years?

I didn’t think I’d get many takers.

How about a chance to own one of the fastest growing parts of the global economy—at some of the cheapest valuations currently on offer? That probably sounds more enticing.

In both instances, however, we’re talking about the same investment: emerging market stocks. While the S&P 500 notched a handsome 14.7% annual gain over the past five calendar years, MSCI’s Emerging Markets index eked out an average gain of just 1.3% a year, with losses posted in 2013, 2014 and 2015.

Thanks to those wretched returns, today’s buyer can invest at modest valuations. Emerging stock markets are trading at a price-earnings multiple of 14, versus 21.9 for the developed world, according to StarCapital.de. These are so-called cyclically adjusted price-earnings ratios, meaning they compare current stock prices to average inflation-adjusted earnings for the past 10 years.

After five years of lackluster performance, will the future be brighter? Investment theory says “yes.” The riskier an investment is, the higher its expected return—and you don’t get much more volatile than emerging markets. One example: MSCI’s Emerging Markets index plunged 53.3% in 2008, only to soar 78.5% in 2009. For those who could ride out such volatility, the long-run returns have been handsome. Over the past 15 years, emerging markets have clocked an average 9.5% a year, easily outpacing the S&P 500’s 6.7%.

Past performance, of course, is no guarantee of future results. But beyond cheap valuations, emerging stock markets have another huge advantage: They don’t face the demographic headwinds that confront the developed world—and that’s already hampering economic growth in the U.S., Europe and Japan.

There are two key components to economic growth: how fast the working population grows and how much more productive workers become each year. For instance, the U.S. economy has grown at an inflation-adjusted average of almost 3% a year over the past 50 years, with half that growth coming from increases in the working population and half from productivity gains. But instead of 1.5% annual growth in the civilian workforce, we’re now looking at just 0.5%, as new workers barely outpace those who retire. That makes it tough to achieve growth that’s much above 2%—and lately we haven’t even managed that.

This is a problem across the developed world. The International Monetary Fund projects that, over the next five years, the developed world will clock annual economic growth between 1.7% and 1.8%. By contrast, the IMF projects that annual growth in the developing world will range between 4.6% and 5.1%. Moreover, there’s a good chance that emerging economies will continue to grow faster than the developed world for many decades, thanks to their far younger population.

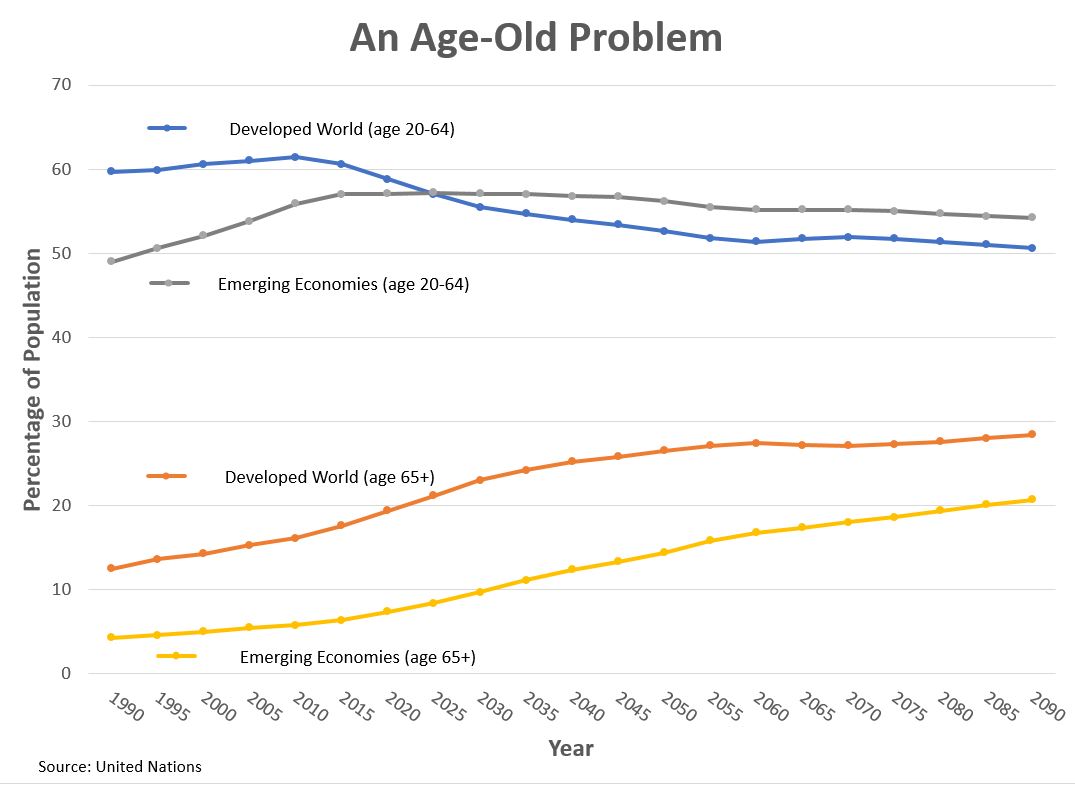

According to United Nations data, as of 2015, 17.6% of the developed world’s population was age 65 or older, up from 12.5% in 1990. Fast forward 50 years, to 2065, and 27.1% of the developed world’s population is expected to be 65 and older.

Compared to the rest of the developed world, the U.S. is in somewhat better shape. As of 2015, 14.8% of the U.S. population was 65 or older, up from 12.5% in 1990. By 2065, we’ll be at 23.9%.

But even in the U.S., our increasingly elderly population, coupled with slow growth in the workforce, is raising a host of tricky questions. Is there any way we can get the economy to grow faster? Can we produce the goods and services that society needs if everybody continues to retire at today’s average retirement age of 62? Can we afford Medicare and Social Security in their current form?

For now, these sorts of thorny questions simply aren’t an issue for the developing world. Yes, emerging nations will eventually have to grapple with the economic implications of a much older population. But their problems are far down the road. Today, just 6.4% of the developing world’s population is age 65 or older. Fifty years from now, that number will be 17.4%—roughly where the developed world is today.

How reliable are these figures? We have a pretty good idea of how many 65-year-olds there will be in 2065, because these folks have already been born and now roam the earth as surly teenagers. Absent a deadly plague or massive population migration, the die is pretty much set—and emerging economies have the advantage. Demographics truly are destiny.

That doesn’t mean developing countries couldn’t squander their demographic advantage. Political upheaval, misguided economic policies and weak property rights could all derail economic growth. And even if growth comes through as expected, there are likely to be plenty of losing years for investors in the decades ahead. Still, for those who can stomach the volatility and hang in for the long haul, this seems like one rollercoaster that’s well worth riding.