Key Financial Principles to Prepare Children for the Future

It’s no secret many adults struggle with their finances. In a recent survey:

- 34% of Americans said they were either struggling with their finances or in full financial crisis.

- 54% reported they’re afraid they won’t have enough money to cover their monthly expenses.

- 32% said they didn’t fully understand the consequences of taking out student loans before they signed up for them.

- 51% said they regretted taking out student loan debt to pay for their education.

- 25% reported maxing out a credit card in the last 90 days.

Perhaps most telling is that 53% of those surveyed said they were never taught how to handle money as they were growing up.1

Sadly, many of the financial problems Americans struggle with could have been avoided if basic financial literacy had been taught in school. Today, more schools are looking for opportunities to integrate financial literacy into their curriculum, but children and young adults still face a huge financial knowledge gap.

That’s why we believe all schools should teach the following money lessons.

#1 – How your income impacts your lifestyle

One of the first steps in building a solid financial foundation is to establish a source of income. For children and young adults, this may be an allowance or income earned from a part-time job. As you get older, it’s important to understand how your income impacts your potential lifestyle.

For example, if you have a goal to live in a certain city, purchase a home or travel the world, you need to figure out a way to earn enough income to support it. This simple financial concept can inform a wide range of decisions along the way, from your college major and your spending decisions to how you save and invest for the future.

#2 – The importance of saving for emergencies

It’s important to understand that, if not properly planned for, an unexpected expense can quickly derail your financial progress. Saving in an emergency fund is one of the first steps toward achieving financial security.

As soon as possible, start working to save three to six months’ worth of living expenses in a liquid emergency account. Doing so could help give you the peace of mind of knowing you can cover unexpected expenses without disrupting other aspects of your financial life.

#3 – How to budget

A budget is an important tool to help guide your financial decision making and keep you on track toward achieving your goals. A budget provides insight into exactly where your money is going each month and can help you identify spending issues early in life, before they get in the way of your long-term goals.

#4 – How to manage debt

Owing money in the form of debt means your financial priorities are to someone else, rather than to yourself. It’s virtually impossible to get ahead if a large chunk of your income is being used to pay off debt.

Student loans are a major source of debt for many Americans. This debt obligation can be a huge burden for decades into the future, which is why it’s important to thoroughly understand what you’re signing up for before you take it on. Save as much as you can for college in advance, apply for scholarships and make sure the major you select offers the potential for future earnings that are adequate to meet your debt needs.

It’s also important to understand the risks of taking on credit card debt, as many young adults quickly get in over their heads with high-interest payments and late fees. This type of financial burden can haunt you for years into the future, making it difficult to achieve your financial goals.

#5 – The power of compound interest

A great way to achieve financial security later in life is by investing at a young age. Many adults are unaware of the power of compound interest, but the sooner you start investing, the better chance your savings has to grow exponentially over time.

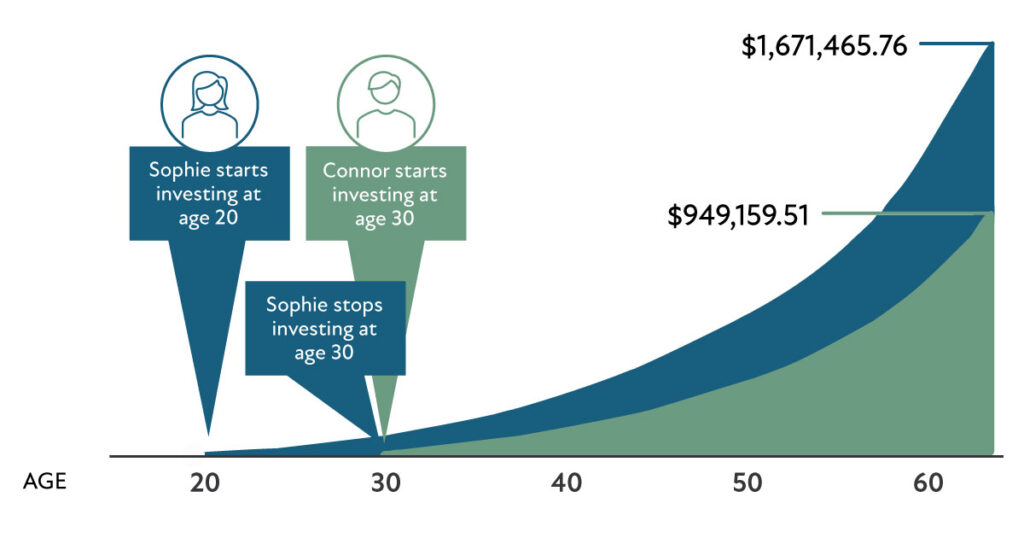

Consider the following chart, which illustrates the impact of compound interest. Notice that both Sophie and Connor invest $250 per month. However, Sophie begins investing at age 20 and completely stops making adding to her investments at age 30. Connor, on the other hand, waits until age 30 to begin investing but continues adding $250 to his investment account each month until he reaches age 65.

Assuming an 10% annual return, look at the difference between Sophie and Connor’s investment savings at age 65!

The $30,000 Sophie contributed over 10 years while she was in her 20s has grown to more than $1.6 million, while the $105,000 Connor contributed over 35 years starting in his 30s has only grown to just over $949,000.

This is a compelling reason to ensure every student has a firm grasp on the benefits of investing at a young age.

Could you use help educating your children on key financial literacy concepts? Creative Planning is here for you. We believe in the importance of educating clients and their loved ones on a wide range of financial planning topics. We want both you and your family members to be well informed and positioned for financial success. To learn more, schedule a call with a member of our team.