The current economic cycle, and all the variables that have gone into making it one of the most nausea-inducing cycles of the modern era, will most certainly be studied in economics classes for many years to come.

Let’s begin with how we got here. To do that, we’ll need to ride our “way back machine” to when the COVID lockdowns began in March 2020. With everyone at home, and much of the global economy shut down, the economy came to a near-screeching halt.

History tells us that when an economy is frozen, there are several ways policy makers can help speed up a recovery. These responses can be broken down into two main categories: fiscal policy and monetary policy.

Fiscal policy refers to the government’s use of tax policy and spending to influence an economy. For example, if Congress decides that people giving money to charities is good for the country, it may pass a law giving tax breaks that encourage that behavior.

During recessions, Congress and past presidents have tended to be fairly aggressive with fiscal policy.1 In 2008, Congress passed massive bailouts to keep the banking system going and further breaks to encourage spending. But this time — well, this time was on an entirely different level. Combined, Congress and Presidents Trump and Biden gave away a record-shattering $5 trillion, with more than $1.8 trillion going to individuals, $1.7 trillion going to businesses, $745 billion going to states, $482 billion going to healthcare initiatives and another $288 billion more spread around for good measure. For perspective, with that amount of money, the government could have paid off 100% of the debt of the bottom 50% of Americans (as measured by wealth) or purchased the 15 million homes and condos sold in the United States over the two-year period. The system was awash in money.2

But wait, there’s more.

Not to be outdone, the Federal Reserve moved into full superhero mode. The Federal Reserve exists to help ensure two things: that unemployment stays low and that inflation stays modest (ideally, near 2%). With everyone in lockdown and no one spending, the Federal Reserve went to their textbooks, which say the way you encourage people to spend is by making money “cheaper”. One way the Fed can do that is by lowering interest rates. If interest rates are 2%, you can make a larger monthly mortgage payment than if they were 7%. So if the Fed lowers interest rates, it pulls more people into the homebuying market, and they’re willing to spend more, driving home prices up. This same concept applies — as we are all now very aware — to cars, washing machines, boats and so on.

Now, this concept of lowering rates to entice people to spend really does work. We saw it work after the tech bubble, 9/11 and the 2008 crisis. But this time the fact set was different, and the textbook answer was incorrect. In past bear markets and recessions, people were generally shocked by an event that created a massive economic impact, such as the cocooning that followed 9/11 or the apprehension to purchase a home after 2008. But going into COVID, the economy was strong. People had money, and there was substantial consumer confidence. People were ready to spend money. No one needed to be coaxed to become a consumer again. People were simply fearful of getting sick or dying. In effect, it was as if there was a severe blizzard that prevented everyone from spending. Once the blizzard passed, people would simply get back to it, no incentives needed. But the Federal Reserve didn’t see it that way and dropped borrowing rates to near zero.

So now we have two pieces to the inflation puzzle: first, the government gave away $5 trillion, and second, the Federal Reserve made the cost of borrowing very low.

Quick Economics 101 Break:

Rule #1 of economics: The amount of a commodity, service or product, and the desire of consumers to buy it along with consumers’ ability to buy it, will regulate its price.

In other words, if everyone has a specific amount of money, and there are a specific amount of goods and services available that people want, the market will adjust prices to match the supply and demand.

So, we had $5 trillion more in the hands of consumers, but all those new dollars were chasing the same amount of goods and services. This, as a first-day economics student knows, means prices will go up.

But wait, there’s more.3

It turns out we don’t just have more money with lower borrowing costs chasing the same amount of goods and services. There are now actually also fewer goods and services to chase. With the arrival of the vaccines, it was expected that the supply chain would return to normal. But that hasn’t been the case. Even today, there are constant lockdowns in China, many of which create serious disruption to the supply of various goods that rely on a key part from China. And overall supply chain issues go much further than that, given the start of the war in Ukraine, energy supply disruption and the issues surrounding escalating global tensions.

So, let’s take our supply and demand formula and examine what happened: the government added a record-breaking amount of money to the demand side of the equation, and the Federal Reserve added super low interest rates to the demand side of the equation. At the same time, the supply side of the equation declined due to lockdowns, war, energy prices and so on.

More money + cheap borrowing rates chasing less supply = high inflation.

So, what’s the big deal about inflation anyway? Everyone feels good when their home values and 401(k)s go straight up, right?

Well, there are serious downsides to inflation, and here are just a few:

- It causes a loss of confidence in the dollar. People don’t want to work for a currency that loses its purchasing power quickly.

- Inflation interferes with rational purchasing decisions. Not too long ago, people were buying used cars expecting to sell them for more a few months later.

- Inflation encourages risk-taking that can lead to bubbles. Why not stretch for a super expensive house? You might as well go all in if you expect it to go up in value 10% per year.

- Inflation can create a retirement crisis, as many Americans aren’t invested in a way to protect against high inflation. This would put additional pressure on government programs.

Enter the Federal Reserve again…

Remember that the Federal Reserve’s job is to target an inflation rate of around 2%. Given that inflation has soared past 10%, they were quite a bit off target.4 The Federal Reserve has no control over the supply side of the inflation equation. It can’t control energy prices, supply chain issues and so on. But it sure knows how to influence the demand side.

Just as lowering rates over two years put fuel on the demand fire, raising rates can have the opposite effect. That house you loved with a 2.5% mortgage rate available to you doesn’t look quite so hot with a 6.5% mortgage rate. The Fed has been raising rates aggressively all year and has been clear it will continue to do so until they’ve brought housing and speculation under control. For an example of how far we’ve come, in 2021 a 30-year fixed rate mortgage came in around 2.625%. At that rate, $2,008 per month would secure you a $500,000 loan. Today, a 30-year fixed rate mortgage comes in around 6.625%, and at that rate $2,008 per month would only secure you a $313,600 loan.5

By lowering the supply of cheap money, the Federal Reserve is clearing a path for home prices to come down. And home prices aren’t the only asset impacted by interest rates — so are businesses, farms, stocks, bonds, commercial real estate, and on and on.

So where are we today?

- Housing is softening, luxury home prices are falling off a cliff and bidding wars are a thing of the past.

- Stocks have spent much of the year in bear market territory, and bonds — especially long-term bonds — have been hit hard. Commercial real estate is starting to enter into the bloodletting.

- Speculative assets, such as SPACs, meme stocks, NFTs, cryptocurrencies and small stocks with no earnings have gotten absolutely destroyed (as we predicted here), with many down 70%-100%. Most of these will never recover, resulting in permanent financial destruction for investors who saw these asset classes as the new era of investing.

So, what does this mean for investors?

For the disciplined long-term investor, it’s hard to not see the light at the end of the tunnel.6 A long-term investor who owns bonds as part of her portfolio benefits from higher interest rates. This seems hard to fathom, given that higher rates this year have resulted in investors watching their bond portfolios sink in value. But that’s the short-term impact. The investor is clearly better off in the long run.

For example, you may loan money to a corporation for 4% per year for five years. At the end of the five-year period, you get all your money back, plus you received 4% interest each year along the way. All good. Except, if interest rates go up a lot along the way, you can’t sell your bond before maturity for full value because new investors would rather buy new higher-yielding bonds. This is why a bond appears to have lost value before it matures in a rising interest rate environment. But the long-term investor holds the bond to maturity then happily invests the money they get back into a new higher-yielding bond. Over the long run, the investor collects more income — the investor wins.

If you purchased a two-year certificate of deposit (CD) paying 3% per year at your local bank, and after the first year CD rates increased to 5%, would you be upset? Probably not. Yes, if you wanted to sell your CD before maturity, you would have to sell it at a discount, but instead you may hold it to maturity, get all your money back, then purchase a new higher-yielding CD. The higher rates benefit you as a lender. For long-term investors with bond allocations, higher rates are very good news and increase the probability of a diversified portfolio hitting its target return.7

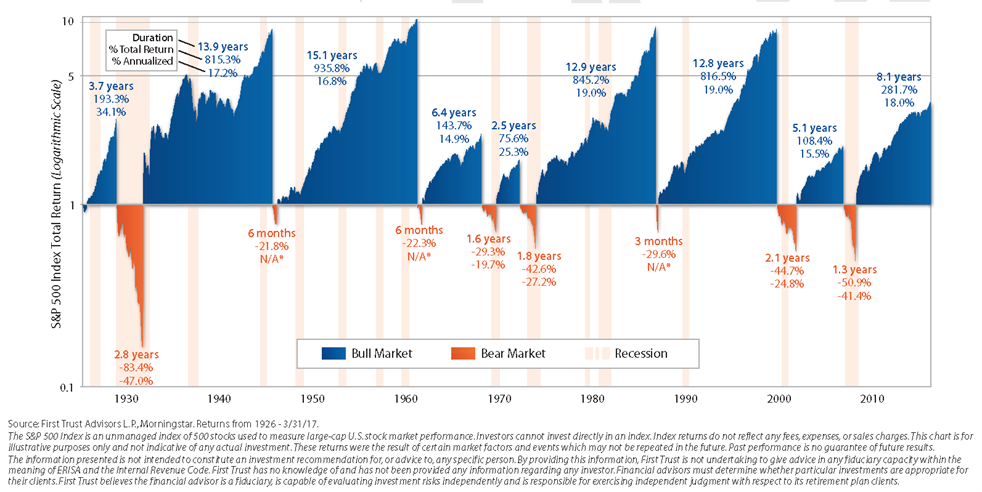

The stock market story is more complex. First, many speculative stocks may never recover. This will likely be similar to the dot-com era. The strong companies will survive and thrive, and the speculative garbage will never recover. But for quality stocks and indexes, a full recovery and march on to new highs is expected. Of course, bear markets and recessions are dynamic, and any new variables can enter the picture at any time. No one knows when the bear market will be over. But we do know the U.S. has faced more than 30 bear markets, and they’ve all ended the same way: with a full recovery and march on to new highs. Every recession has given way to an expansion — the only question is when. While these setbacks tend to last six to 18 months, and we’re already well into this one, it’s simply unpredictable.

We do know a few things though:

- The stock market usually recovers well before a recession is over. In fact, by the time we have the data to even know there was an official recession, the stock market has usually already recovered.

- We know that when the market does turn, it tends to soar very quickly. The market usually won’t work its way out of a bear market at 6% per year. In fact, from these levels, the average cumulative three-year return for stocks is more than 40% and the average cumulative five-year return is more than 70%.

Finally, looming in the background are our friends at the Federal Reserve, and this time they have something they haven’t had in decades: a loaded gun. With all the bear markets over the last few decades, the Fed lowered rates to encourage spending to speed up the recovery. This can be a dangerous game, because when rates are near zero, if something else happens the Fed has little it can do. But this time, the Fed is actually creating the bear market by raising rates. This means if the Fed isn’t able to engineer a “soft landing” and instead sends us into a severe recession, they can simply lower rates to once again stimulate housing and everything else.

And in fact, that’s exactly what the bond market is predicting. By watching bond prices, we can tell what the market expects the Federal Reserve to do going forward. As of today, it expects a rate hike of 0.75% in November, 0.50% in December and 0.25% in February. And after that? Well, the market expects the Federal Reserve will have to lower rates to restimulate the economy. And the game goes on…

Bear markets happen every few years — there will be many, many more along the way. This chart gives us some long-term perspective:

The disciplined, long-term investor is aware of this and therefore must have exposure to assets that protect against long-term inflationary trends (like stocks, real estate and so on). She must also have her short-term income needs met by dividends, bond yields, distributable income and short- to intermediate-term quality bonds.

The disciplined long-term investor never “blows up” because she avoids or controls exposure to speculative assets, takes advantage of market opportunities to purchase depressed asset classes and seizes tax opportunities. And when a portfolio’s exposure to various asset classes matches the needs of the disciplined investor, she is never, ever at the mercy of the market.

Footnotes:

- It’s easy to distribute money when it doesn’t have to be paid back while you’re in office.

- It’s like one of Oprah Winfrey’s giveaway shows: “You get a car, you get a car, everybody gets a car!”

- Watching monetary and fiscal policy unfold has been much like watching a 1990s informercial.

- Slight miss.

- Expect home sales to freeze as people decide to stay where they are rather than lose their low mortgage rate.

- And no, it’s not a train.

- Bonds are so boring. Thanks for sticking with me!