And what the market is really keeping an eye on

While Georgia still has two Senate seat run-offs in January, and the Trump administration has said they will contest parts of the election, the market has spoken, pricing in a division of power with Biden as President-Elect and the Republicans holding the Senate. Historically, we know in the year following a split-power election, the market tends to be up about 75% of the time, in line with normal averages.

I recall personally talking to several clients who wanted to leave the country and move overseas after President Obama won in 2008. While we were able to persuade them not to do that, a couple did wind up going to cash. They paid dearly for that move as the market soared over the next eight years. The same thing happened in 2016. I remember being in Florida talking to two separate clients that were alarmed with the election of President Trump. One went to cash and also paid a heavy price as the market went up substantially over the next four years. The reality is many of us are passionate about our politics, our belief system and our values, but we need to separate this from making market timing decisions with our portfolios.

This does not mean a President has no impact on the economy; there are times when a President can get a lot done, particularly when Congress is held by the same party. Having said that, there is one outcome the markets seem to particularly prefer, and that is the situation where neither party has total power. It appears we may be on a path to a division of power. Both parties are going to have a very difficult time getting anything significant done. And that gives the market one thing it absolutely loves: some certainty. The market no longer has to guess if there will be tax cuts or tax hikes (if either happen, they will be modest), stronger regulations or softer regulations and so on. Anything that gets through requires substantive compromise. The most likely scenario is that for at least two years, very few initiatives of substance – by either party – will gain real traction.

The 2022 mid-term elections are likely to ensure more of the same. In nearly every mid-term election, the President’s party loses seats in both the House and the Senate (though of note is the fact that Republicans control 22 of the 34 seats that will be up for re-election). This is the primary reason the market was up the day after the

And what the market is really keeping an eye on

While Georgia still has two Senate seat run-offs in January, and the Trump administration has said they will contest parts of the election, the market has spoken, pricing in a division of power with Biden as President-Elect and the Republicans holding the Senate. Historically, we know in the year following a split-power election, the market tends to be up about 75% of the time, in line with normal averages.

I recall personally talking to several clients who wanted to leave the country and move overseas after President Obama won in 2008. While we were able to persuade them not to do that, a couple did wind up going to cash. They paid dearly for that move as the market soared over the next eight years. The same thing happened in 2016. I remember being in Florida talking to two separate clients that were alarmed with the election of President Trump. One went to cash and also paid a heavy price as the market went up substantially over the next four years. The reality is many of us are passionate about our politics, our belief system and our values, but we need to separate this from making market timing decisions with our portfolios.

This does not mean a President has no impact on the economy; there are times when a President can get a lot done, particularly when Congress is held by the same party. Having said that, there is one outcome the markets seem to particularly prefer, and that is the situation where neither party has total power. It appears we may be on a path to a division of power. Both parties are going to have a very difficult time getting anything significant done. And that gives the market one thing it absolutely loves: some certainty. The market no longer has to guess if there will be tax cuts or tax hikes (if either happen, they will be modest), stronger regulations or softer regulations and so on. Anything that gets through requires substantive compromise. The most likely scenario is that for at least two years, very few initiatives of substance – by either party – will gain real traction.

The 2022 mid-term elections are likely to ensure more of the same. In nearly every mid-term election, the President’s party loses seats in both the House and the Senate (though of note is the fact that Republicans control 22 of the 34 seats that will be up for re-election). This is the primary reason the market was up the day after the election. It sees power divided and normally when power is split, most changes that get through require compromise that prevents radical change either way. The market loves incremental change, or no change at all, because it provides certainty. The parties do agree on a few issues:

- Both support another round of stimulus, which could come before year end or after the change in power in early 2021.

- Both support infrastructure spending on bridges, roads and so on. But, this has been the case for the last decade and the parties have been unable to agree on what to prioritize.

- Both share a general disgust of Big Tech companies. Democrats see them as monopolies that should be broken up, more heavily regulated and taxed at higher rates. Republicans see them as using their monopolistic platforms to censor and influence politics. Congressional hearings are a near certainty.

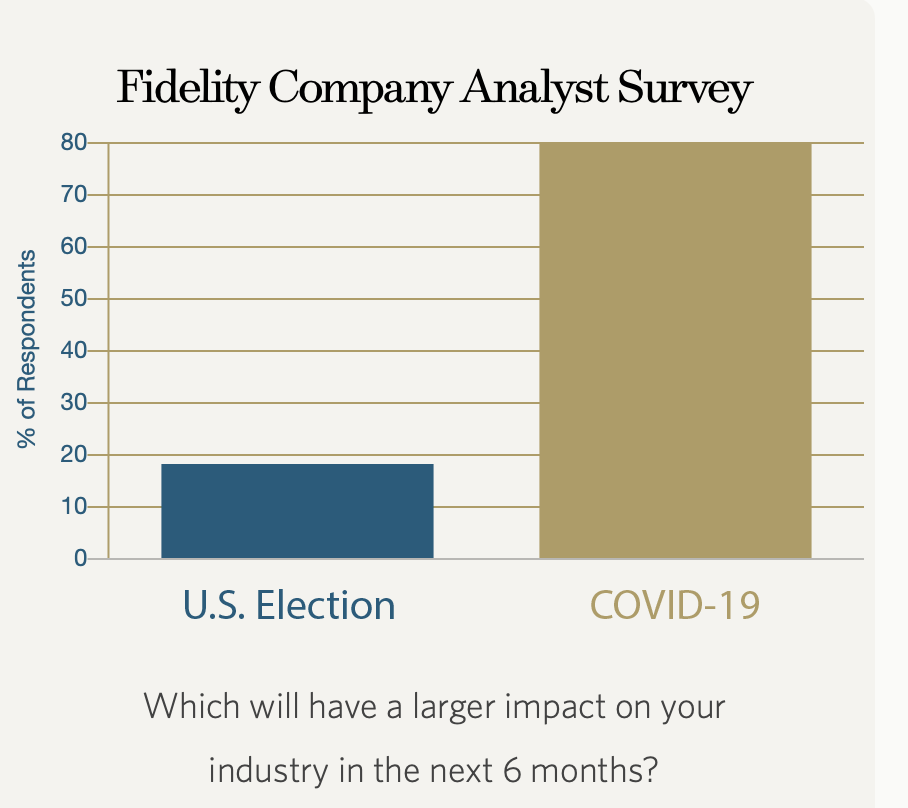

The reality is the most important thing impacting the markets between now and the end of the year has nothing to do with the election and everything to do with COVID-19. The reality is the market only cares about one thing: future earnings. The primary issue that is going to impact future earnings is consumers feeling comfortable enough to operate in the economy and spend money. So far, we are experiencing what many would call a ‘V’ or ‘U’ shaped recovery. We went down sharply when the impact of coronavirus was unknown, and much of the economy recovered quickly when it became clear that the mortality rate was lower than expected, that a vaccine may come into play as early as 2021, that there seem to be better treatments in place, and that high-risk groups can self-identify and take precautions while others may be able to move about more freely. Because of this, the economy started to recover.

However, we are starting to see some countries, particularly in Western Europe, go into a lockdown again. We are seeing positive coronavirus cases hit all-time highs in the United States, and we are watching Western Europe close for business. The markets are concerned the United States might end up following suit. That is why the markets were down over the last two weeks prior to the election. While most businesses are doing just fine, and some even exceptionally well, some businesses are suffering. For example, 12% of restaurants have closed during the coronavirus pandemic. Some would refer to this as a ‘K’ shaped recovery; part of the market has recovered with a sharp upward move. For example, technology (or if you happen to be selling RV’s, personal homes, lake homes, boats, bikes) or anything that moves business online is doing well. Some businesses continue to be in a downward slope (such as hotels, some restaurants, and retail). However, if the coronavirus goes on for another six months and inhibits consumers from spending freely, some of these businesses that are still clinging to survival will not be able to hang on and would go under, driving many people to unemployment lines. We would have less people able to buy things, which would then hurt most businesses, potentially causing a domino effect and driving the economy into a recession. In fact, most business owners – when asked the biggest threat to their business over the coming quarters – reference the coronavirus more than the election.

Elections are emotional, and this one, for many, has been one of the most emotional ever. They also have very real ramifications around what we value, how we live and how we feel. However, when it comes to the economy, the one thing the market likes the most about politics is a division of power, forcing incremental change based on compromise. This letter was written on Saturday, November 7th. With the intent of giving everyone a bit of time to digest the election, we set this to go out today, Monday, November 9th. This morning, Pfizer announced the vaccine is 90% effective. The market is soaring. It is – after all – still all about the coronavirus.