And Why You May Not Want to Give Up on Them Quite Yet

I know I’m not the only one who has been watching more movies lately due to the stay-at-home measures brought on the COVID-19 pandemic. As a result, I’ve rediscovered the brilliance of James Bond. From the days of Roger Moore in Moonraker to Daniel Craig in Sky Fall, from skiing through the Alps to dangling from a jet, I can binge watch Bond for hours on end. The suave hero always manages to save the day, with perfect hair and a crisply pressed suit. (Neither of which, perfect hair or crisp suit, have I had in quite some time…)

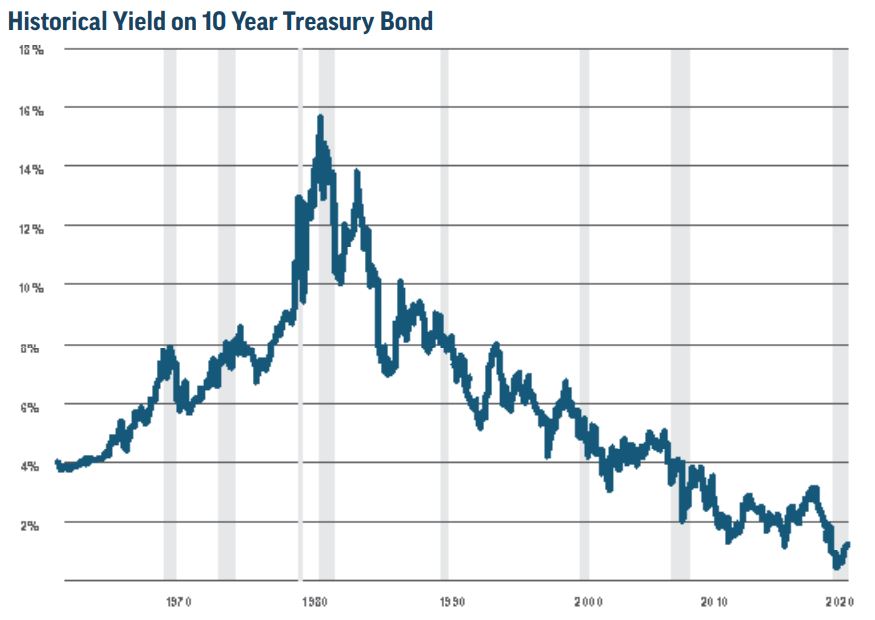

Unlike the adventures of our dynamic and charming James Bond, bonds as a financial instrument have become very boring lately. During the pandemic in 2020, the 10-year Treasury bond, which is used as a gauge for the overall bond market, dropped to an annual yield of 0.38%, the record low for Treasury bonds.1

Historically, the 10-year Treasury bond has yielded around 4.38%.2 Rates have risen lately but are still only about 1.5%.3 Needless to say, this is not the type of return most investors are seeking to help them reach their financial goals. Factoring in even a modest amount of inflation results in negative real rates of return.

Historical Yield on 10 Year Treasury Bond

Although the 10-year U.S. Treasury is typically used as a benchmark for the overall bond market, there are many different types of bonds that have varying yields. As our CEO, Peter Mallouk, likes to say, “Bond is just a fancy term for loan.” You can loan money to federal or state governments, a municipality, or a corporation and receive interest payments and principal at maturity. With a bond, you are loaning money, as opposed to a stock where you are purchasing a fractional ownership piece of a company.

There are two ways to receive higher bond payments:

- Extend the maturity – You can expect to get paid more when you loan money for a longer period of time. For example, currently a one-year Treasury note pays 0.08%, a 10-year Treasury bond pays 1.53%, and a 30-year Treasury bond pays 2.24%.4 This is called the yield curve, and in healthy markets the slope is positive, meaning longer term rates provide a higher interest rate.

- Credit risk – You can also expect to get paid more if you take more risk. Credit risk is the likelihood that your principal will be paid back. The U.S. government pays the least amount of interest because loans are considered risk-free. In contrast, a loan to a small company will pay much higher interest because the risk of default is greater. While junk bonds are high-yielding corporate bonds, they tend to have greater risk of default. If the economy weakens and the equity markets decline, they are likely to tumble alongside stock prices.

Given today’s low interest rates, you may be wondering why I would consider including bonds in a portfolio. The key reasons for consideration:

- Expected return/income greater than cash – While bond yields might still be considered low from a historical perspective, they still outpace the expected return investors will likely earn on cash.

- Stability – Peter Mallouk likens choosing between stocks and bonds to choosing different roller coasters. You’re going to have fluctuations either way, you just have to choose your level of volatility. When my boys were young and I’d take them to Six Flags, they were thrilled with the kiddie coaster at Bugs Bunny Land. Now that they’re older, they want the scarier experience of Mr. Freeze and the Titan. The bond market is the kiddie coaster, while the stock market is the Titan. Most investors don’t need the wild up and downs of a rollercoaster, but prefer a mix of stocks and bonds, which has historically helped to moderate the portfolio fluctuations/volatility.

- Liquidity – Bonds provide an important source of liquidity to meet distributions needs or to buy stock on market dips. In most cases, quality bonds continue to have positive returns during market corrections and bear markets.5 As you can see in the chart below bonds had positive returns in each of the last three major bear markets, the technology bubble/911, the financial crisis, and the COVID-19 pandemic.

During these market downturns, bonds provided investors with capital for opportunistic rebalancing. At Creative Planning, we use down markets as an opportunity to buy additional stocks at a discount, using bonds to provide the capital/liquidity.

In situations like these we believe that opportunistic rebalancing can help client portfolios recover prior to the market’s full recovery.

Bonds also provide liquidity for living expenses. For example, for those living in retirement and withdrawing funds during one of these bear markets, it would have been detrimental to sell stocks while the market was down in order to cover monthly living expenses. Investors who had access to bonds, however, were not at the mercy of stock market performance to provide for their living expenses.

At Creative Planning, we recommend our retired clients have approximately five to seven years’ worth of living expenses in bonds in case we enter a prolonged market downturn. However, with interest rates at historic lows, we don’t recommend holding more bonds than necessary.

The old rule of thumb defined a balanced portfolio as one with 60% stocks and 40% bonds. In this historic low-interest-rate environment, we have thrown this “rule” out the window. Instead, we look at the dollar amount a client needs, rather than focusing on a percentage allocation. For example, if a retiree needs $8,000 per month for living expenses, or $96,000 per year, then we recommend he or she has $480,000 ($96,000 x 5) in bonds. For a $2 million portfolio, this represents a 24% overall allocation.6

To sum it up, while there are important reasons to own bonds as part of a diversified portfolio, bonds are not going to provide dynamic growth. We recommend younger investors and investors who have many years until retirement reevaluate their investment risk tolerance and allocation to bonds. In the current environment, we believe these investors are often better off overweighting stocks. We recommend retirees ensure they have a sufficient bond allocation to cover the next 5-7 years of living expenses, but not more than necessary.

At Creative Planning, we work with clients to develop diversified investment portfolios that help them achieve these long-term goals. We believe investments play a vital role in the financial planning process, yet they are only one piece of a much larger puzzle. If you would like to speak with one of our qualified advisors about how we can help guide you toward your long-term goals, please contact us.

Footnotes

- Marketwatch.com

- Ycharts.com

- Marketwatch.com

- Treasury.gov

- Barclays US Aggregate Bond Index – Creative Planning Periodic Table of Style Rotation

- This example is for illustrative purposes only and should not be considered or used as investment advice.