A Charitable Remainder Trust Primer

Spring is here and I find myself hoping that this year, April showers bring both May flowers and a light at the end of the 2020 tunnel. But, even with the sun shining and the tulips popping out above ground, your friendly neighborhood estate planning attorney is here to redirect your gaze six feet below ground.

With potential federal tax changes on the horizon, now may be a great time to reevaluate your estate plan. If you are charitably inclined, it’s particularly important to have a plan in place to help you achieve your philanthropic and tax planning goals; a charitable trust can be an efficient vehicle for achieving your objectives.

For those just getting up to speed with advanced estate planning lingo, the acronyms involved can make you feel like you’re diving into a bowl of alphabet soup, and charitable trusts are among the worst offenders – CRT, CLT, CRAT, CRUT, CLUT, CLAT, NIMCRUT, flip CRUT – who knew there were so many combinations? Here, we take a bird’s eye view and walk through the basics.

Types of CRTs

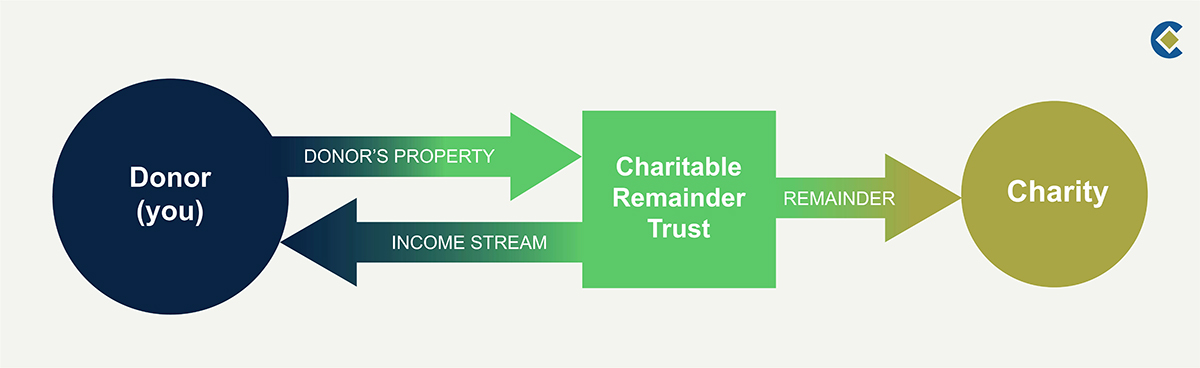

The most common type of charitable trust is a Charitable Remainder Trust (CRT). A CRT is an irrevocable “split interest” trust with charitable and non-charitable components. CRTs are created when a donor gifts property to a trust, names a non-charitable income beneficiary (commonly the donor him/herself either for life or for a set term of years) and names an ultimate charitable remainder beneficiary (or beneficiaries).

Figure 1

CRTs can be structured in different ways:

- Charitable Remainder Annuity Trust (CRAT) – Pays a fixed annual annuity amount to the non-charitable beneficiary. Regardless of whether the property in the trust increases or decreases in value, the annual payment remains the same.

For example, if a CRAT is established with $1 million and the donor retains a 5% annuity interest for life, the donor will receive $50,000 each year until his/her death or until the CRAT runs out of assets.

- Charitable Remainder Unitrust (CRUT) – Pays a fixed annual percentage to the non-charitable beneficiary. In contrast to a CRAT, a CRUT’s annual payment fluctuates based on increases or decreases in the trust’s value.

For example, if a CRUT is established with $1 million and the donor retains a 5% unitrust interest for life, the donor will receive $50,000 in the first year. The unitrust payment for subsequent years is determined by applying 5% to the beginning value of the trust principal for the year in which the payment is being made. Most clients utilize a CRUT structure because they expect the trust assets to appreciate over time, and they want to share in that growth.

CRT Considerations

It’s important to be aware of the following points before establishing a CRT:

Payment limitations – For both CRATs and CRUTs, specific federal tax rules limit annual payment amounts to ensure the charity is projected to receive at least 10% of the initial asset value. This projected remainder is determined using a formula that accounts for an interest rate issued by the IRS and the term of the CRT, whether a fixed number of years or the life expectancy of the beneficiary per IRS age-based tables. Typically, CRAT annuity payments are set between 5-15% of the initial value of the trust property, and CRUT payments are between 5-50% of the yearly value of the trust property.

Additional contributions – A CRAT cannot accept additional contributions, whereas the donor of a CRUT can make further contributions to the trust in later years.

Tax status – CRTs (both CRATs and CRUTs) are tax-exempt entities, which makes them especially useful for donors who have low-basis assets that have appreciated significantly. Consider the following example:

- Taxpayer 1 owns a stock portfolio with a fair market value of $1 million and a cost basis of $100,000. If Taxpayer 1 funds a CRT with the stock and the CRT then sells the stock, no capital gains tax would be due under current tax provisions.

- Following the sale, $1 million is available for investment. The non-charitable beneficiary is typically required to pay income tax on the value of the annual payments he or she receives during the term.

- If Taxpayer 2 has an identical portfolio and sells it, the $900,000 gain would be subject to tax. After paying those taxes, Taxpayer 2 may have $800,000 or less left for investment.

- Tax deductions – Upon funding a CRT, the donor is entitled to an immediate income tax deduction equal to the present value of the charitable remainder interest (indicated by the remainder arrow passing to the charity in Figure 1 above).

If the trust is funded with cash and the remainder beneficiary is a public charity or donor-advised fund, the income tax deduction is limited to 60% of adjusted gross income (AGI) for the year. However, the deduction may be further limited to 30% of AGI if the remainder beneficiary is a private foundation, or 20% of AGI if the CRT is funded with appreciated property. Deduction limitations for certain types of non-marketable assets are even more restrictive.

Regardless, the donor may carry forward any unused charitable deduction amount for up to five additional years following the year of the gift.

Revisiting the previous example, Taxpayer 1 would have received an upfront charitable deduction upon creating the CRT that could be used to offset other income. Assuming that Taxpayer 1 retained the right to receive 5% unitrust payments from the CRT for life and was 45 years of age at the creation of the CRT, the charitable deduction would be more than $300,000 (as determined by IRS tables). Assuming a 40% income tax rate, the value of this deduction to Taxpayer 1 is $120,000.

Taxpayer 1 was able to liquidate the portfolio with no current income tax hit, receive a current charitable deduction and retain the right to receive unitrust payments for life.

Charitable beneficiaries – CRT donors can name multiple organizations as charitable beneficiaries and can also reserve the right to change those beneficiaries in the future.

Funding sources – When determining what assets should be used to fund a CRT, consider cash, highly appreciated publicly traded stock, and possibly closely held business interests (subject to the excess business holdings rule). Avoid funding a CRT with mortgaged property, S-Corp stock, illiquid assets or tangible goods.

If you have appreciated assets to divest, are charitably inclined and hate paying taxes (like most of us!), CRTs are an option that have the potential to leave you singing in the rain this spring and beyond.

If you would like to learn more about whether establishing a CRT makes sense for your personal financial situation, Creative Planning is here to help. Our advisors believe charitable giving strategies are an important part of the financial and estate planning process and have experience helping clients realize their giving objectives. Contact us to learn more.